Rollercoaster: A year in a quarter

In the first quarter of 2026, investors could be forgiven for being driven to distraction. Stock markets are always noisy, buffeted by a cocktail of macroeconomics, geopolitics and company-specific news. Yet it is hard to recall a period of prices being impacted to such a large extent by such differing factors.

The war with Iran has provided the fourth material supply shock for the global economy this decade, following the pandemic in 2020, the invasion of Ukraine in 2022 and Tariffs in 2025. Central banks struggling to reach their inflation targets are today facing the spectre of stagflation once again. This is confirmation, if it were needed, that the 2020s are proving a considerably more inflationary decade than the 2010s. An energy crisis risks a reversal in fragile economic growth and increases the potential for a recession.

The year started robustly at the index level, but with material divergences in stock-specific performance. There was a strong preference for the physical (real assets including gold, commodities and related companies including miners) over asset-light, quality growth businesses, such as software and data service companies. Included within this shift was a desire for substance and scarcity and a move from growth to value. In March, as hostilities broke out in the Gulf, there were few places to hide. Staples and other typically resilient stocks were weak, while bonds proved to be a poor hedge due to fears of rising inflation. The latter continued an ongoing theme of closer correlations for asset prices, especially fixed income and equities. We expect this to continue in a world where inflation remains structurally higher, and we reflect this via low duration in the portfolio’s fixed income and index-linked bonds.

Gold, although up for the quarter overall, failed to offset equity declines during March. We expect that profit taking and demands for liquidity have since removed some of the more speculative activity that was in evidence in the gold market towards the end of January. We reduced the holding in our Multi-Asset portfolios at ~$5,100 from 14% to 10%. As we wrote in February, “This does not change our long-term view on the yellow metal. However, after such a strong run, there is plenty of room for a setback. Investment banks have recently become highly enthusiastic towards precious metals, which was certainly not the case a couple of years ago. They suggest tantalising year-end 2026 price targets of over $6,000/oz. This cheerleading makes us nervous, and we recognise in the short term there is scope for disappointment. We would not wish to make the cardinal sin of getting ever more bullish into rising prices.”

Almost forgotten, amid such an eventful quarter, was the appointment of the world’s most important central banker. After flirting with various unconventional and inappropriate candidates, President Trump opted to appoint Kevin Warsh as the new Chairman of the Federal Reserve, to replace Jerome Powell in May. This is important because there was considerable concern about the Administration’s threat to the Fed’s independence. The appointment of a supposed ‘hard money’ intellectual, who has served as a Fed Governor before (2006-2011) may lower this risk. Straight from ‘central casting’, Warsh is known for his criticism of the Ben Bernanke-led Fed, its balance sheet expansion and zero interest rates following the Global Financial Crisis. Warsh is seen as a less unorthodox, safe pair of hands. Does this mean Warsh’s tenure will lead to ‘sound money’ and US dollar strength? We sincerely doubt it. For the time being, Warsh is an advocate of interest rate cuts, despite inflation being stubbornly above target.

‘SaaSmageddon’

In addition to the Gulf war, Artificial Intelligence (AI) continues to dominate the stock market narrative, with some very sharp share price moves in recent months, especially to the downside, where investors are grappling with the technology’s effects on business models. In the same way that during the internet boom and bust 26 years ago investors sought to target the web’s winners and losers, there is a rising doubt about the terminal values (the longevity of earnings sustainability and growth) for some business models and sectors. Focus has been on SaaS (Software as a Service) companies, like Salesforce and SAP, and data companies, like Wolters Kluwer and Thomson Reuters.

Other less obvious sectors affected have included caterers, like Compass, for fear of fewer employees to feed, real estate service companies, such as CBRE, wealth managers like St James’s Place and insurance brokers including Marsh. At times in the past three months, company management in these sectors must have felt their share prices were victims of a drive-by shooting, perplexed when announcing solid financial results that are yet to be affected (or not) by the oncoming disruption. The noise coming from the AI cognoscenti highlights the broad effects the technology could have on the wider economy. For example, Anthropic’s co-founder and CEO Dario Amodei has stated AI could displace half of all entry-level white-collar jobs in the next 1-5 years. The April 7th announcement of Anthropic’s latest model, Claude Mythos, has added to these insecurities, with early reports suggesting it is startlingly impressive.

Share prices may follow earnings in the very long term, but unprecedented uncertainty around business models and this breakneck pace of AI development have left disproportionate room for shifts in sentiment. There is an argument for avoiding both the ‘winners’ and ‘losers’ as deemed by the market. Perhaps the most prominent ‘winner’, technology hardware, is inherently cyclical and will suffer a downturn once the capital expenditure cycle matures. Perceived losers, like SaaS and data companies, are vulnerable to changes in how their services are delivered and monetised. Perhaps the valuations of these companies were anchored on past success and are merely catching up with reality. Software and data companies have long benefited from premium valuations, exhibiting strong and sustainable operating margins, high returns on capital, consistent growth and sticky customer relationships. Many of these qualities are now in doubt in an AI world. There are other parts of the stock market, like consumer staples or railroads, which will not be affected by AI disruption, where investors may choose to hide from the crossfire. We will see how the dust settles. Such severe rotation is rare but not unprecedented and may be explained by continued regime change from the era of zero rates and QE to a higher cost of capital.

The second mouse gets the cheese

First quarter reporting has begun. The most notable aspect of results season continues to be the increase in AI-related investments by the hyperscalers. The extent of the capital investment is breathtaking, with Alphabet proposing to double its investment from $91bn in 2025 to $180-190bn in 2026. This arms race has reached fever pitch. The spending is justified by huge backlogs in revenue. Alphabet has highlighted a $460bn revenue backlog for its Google Cloud business alone. Whether this spending has an adequate return on capital is still to be determined and, as these companies move from spending their cash to spending debt, investors are likely to question the returns. There is also the growing involvement of private credit in the sector (as highlighted in Troy’s Special Paper No.13). According to the Bank of International Settlements, there are already more than $200bn of private credit loans in AI-related investment which is expected to grow to $300bn-$600bn by 2030. Free cash flow for the hyperscaler companies is plummeting. Microsoft on a multiple c.20x, only offers a free cash flow yield of c.2.5% – a decade low. When we acquired the holding in 2010, the free cash flow yield was just below 10%.

Alphabet’s performance has helped our Multi-Asset portfolios over the past twelve months. The share price bottomed at $145 in April and doubled from the lows by the year end. The valuation has risen from ~15x to a high-twenties multiple of earnings. Google’s parent was initially seen as an AI loser, with its core Search franchise perceived to be under threat. This concern was compounded by an ongoing antitrust case relating to Apple’s use of Google as the default search provider, which represented a further overhang until it was resolved in Alphabet’s favour in September. Following the successful launch of its Gemini 3 AI model, Google was seen to have overtaken OpenAI (ChatGPT), alleviating (or indeed reversing) fears of disruption to its Search business. There is an increasing concern that OpenAI is losing its first mover advantage, which, alongside broader concerns around software franchises, is likely responsible for some of Microsoft’s recent share price weakness. [Microsoft owns 27% of OpenAI]. With a private company valuation of $850bn, OpenAI feels like the epicentre of the AI bubble. Google has been taking share from ChatGPT; Gemini’s share of web traffic in the generative AI market has increased from 5.3% to 22% in the past 12 months, while ChatGPT’s has fallen from c.87% to c.65%, according to Jefferies.

Scaling up

It is our belief that both Alphabet and Microsoft can remain resilient over the long run in the face of AI because, unlike the model or hardware companies, they have multiple ways to win. Arguably the single greatest unknown, in terms of what will determine the future success of the semiconductor companies like Nvidia and model companies like OpenAI and Anthropic, is whether scaling laws continue to hold – i.e. whether more investment continues to lead to improvement in the models. We do not know the answer to this but are pleased to see that in the case of Microsoft, their capital expenditure is directed towards compute power for inference (i.e. AI usage) far more than towards training (improving their own or other people’s models). In the case of both companies, they boast strong cloud businesses for which demand should continue to grow apace as enterprises get ready for AI. Additionally, in the case of Search and Google’s other eight platforms with over 1bn users, and in the case of the c. 450m people who use Microsoft Office, each company enjoys sizeable distribution advantages.

We expect that the risk-averse Chief Technology Officer looking to deploy AI will prefer to do so via its existing Microsoft software than by experimenting with a new model which lacks the same reputation for security and governance, and which may not be the best one to use in six months’ time. Microsoft is, strategically, model-agnostic despite its OpenAI investment and integrates all the major models into its software. It is worth remembering that with new entrants like Zoom and Slack in the past, Microsoft’s me-too product Teams won out in the end. Another example of the second mouse getting the cheese.

Weighed against these advantages is the reality of increased capital intensity and the fact that we expect more volatility in the short to medium term. We are cautious on the increased capital expenditure and retain a healthy degree of scepticism as to whether, as Microsoft’s management declare, they can earn the same returns on this investment as were achieved during the cloud build out. It is worth acknowledging that today’s spend is on a different scale; at the time of the cloud build-out in 2015, capex[1] was less than $6bn or around 6% of sales, versus $65bn and 23% respectively in 2025. We note that there is pent-up demand for the computing power being built, and that there are few companies with pockets as deep. Both Alphabet’s and Microsoft’s balance sheets remain healthy, whilst they build unrivalled hard assets. Alphabet in particular boasts advantages both in the form of its own chips (TPUs) and a leading-edge model in the form of Gemini. The degree of nuance and ongoing, fast-paced change combined with the elevated multiples of free cash flow on which each stock currently trades, are behind our recent profit taking. The Multi-Asset Strategy’s equity weighting is now a mid-thirties percentage of the portfolio.

Record breakers

The investment zeitgeist of the past decade has been for private companies to delay their arrival on the stock market via Initial Public Offerings (‘IPOs’), with greater value accruing to the entrepreneurs and venture capitalists. This has been taken to an extreme in 2026 with three companies – OpenAI, Anthropic and Space X – looking to list in the coming months. The valuations for these businesses currently stand at $850bn, $800bn and $1.3tn respectively. Anthropic’s value more than doubled last month, from $380bn. These are staggering valuations and will rank as the largest IPOs on record, with SpaceX targeting a $2tn valuation. If these numbers hold, the 10 largest stocks in the S&P 500 Index will account for c.50% of its market capitalisation, up from c.40% today. We have always been sceptical of IPOs as the seller chooses the time to sell and the price. Nevertheless, it may explain volatility in the technology sector as it prepares to welcome the listings of three such substantially valued companies.

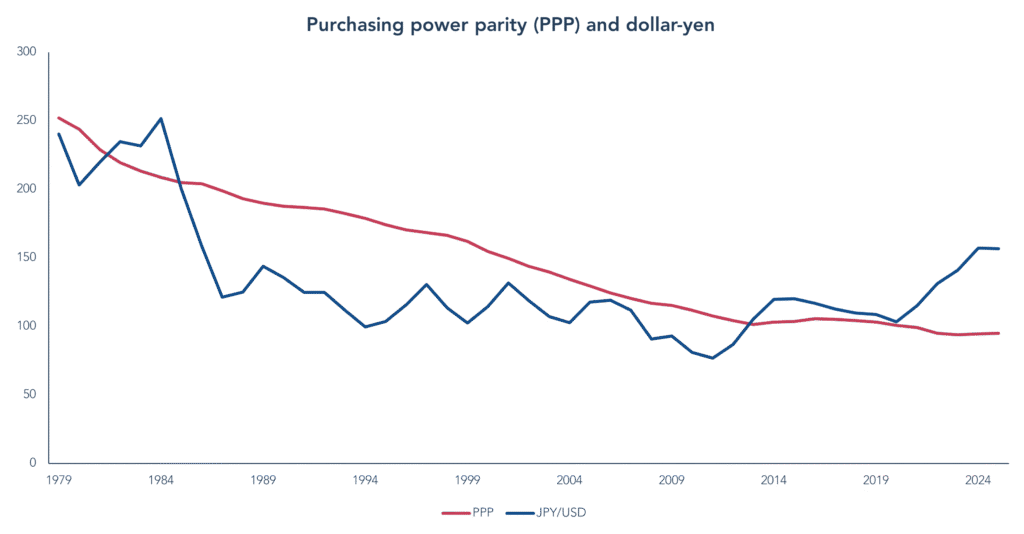

The yen is cheap

In 2025, in the expectation of sustained US dollar weakness, we decided to begin a holding (~10%) in yen through the purchase of short-dated Japanese Government Bonds (JGBs). A first for our mandate. Thus far, the yen has modestly depreciated, but this does not unduly concern us because we expect it to strengthen when other assets, such as equites, are weak. The Japanese currency is the cheapest it has been in my career, over 35 years. The dollar has risen by 55% against the yen since 2020, moving well away from purchasing power parity (PPP), see Figure 1. We believe the holding will provide us with good diversification and an offset, should stock markets become more risk averse. The volume of yen-denominated borrowings allocated to global risk assets continues to be substantial. BCA Research estimates that total yen claims in overseas financial centres amount to approximately $650 billion. This has meant historically that investors will tend to repatriate their borrowings back into yen during crises, leading the currency to strengthen.

There is however plenty of investor concern regarding rising bond yields in Japan as interest rates normalise. We see this as no bad thing, with narrowing interest rate differentials making the yen more attractive. There are common misconceptions about Japan’s debt, which on a gross basis sits at 230% of GDP. However, the net figure is far lower, at ~120%, thanks to enormous assets accumulated from being a creditor nation. Japan borrows at ultra-low (although rising) rates and invests in higher yielding global assets, creating a robust balance sheet rather than a distressed one. Average government debt maturity is nine years, shielding the budget from rate shocks. Only 12% of JGBs are owned by foreigners so there is less of a bond vigilante issue. We have kept our duration very short, expecting yields to rise further over time.

Japan is no longer the economic exception or outlier. The recent dramatic election win for the LDP, and its new leader Sanae Takaichi, gives the party a strong mandate for change, greater confidence and rising animal spirits. The victory has been viewed as a positive for the stock market and for the yen. The cost-of-living crisis is a key issue for the new leader. Her proposed fiscal stimulus is the key risk to yen holdings. It would, therefore, be a good time for the Bank of Japan to demonstrate its independence by tightening monetary policy in the coming months.

Figure 1: The yen is cheap

Source Bloomberg. Past Performance is not a guide to future performance.

Pro-active not reactive

Returning to the Gulf, scarcity of raw materials like oil, fertilizer and helium will take time to work their way through global supply chains. Even if the fighting stops, after-shocks can be expected and a return to normality, that markets already discount, cannot be guaranteed. In the meantime, our index-linked bonds provide some protection from the immediate effects of rising prices expected in the coming months.

We sense a high level of investor complacency, with stretched valuations and heightened inflation risk. The conflict with Iran has greatly increased uncertainty but is yet to be seen as a threat to global growth. We expect markets to remain febrile, as short-term returns are highly sensitive to heightened military action or a diplomatic solution. These may provide us with opportunities to add to holdings, but we must be vigilant in stock selection. As ever, we are looking for asymmetric return profiles, underpinned by supportive valuations, whilst retaining our preference for sustainable and consistently profitable growth. It is always best to be pro-active rather than reactive in circumstances like these.

The cost of living

As of 1st May 2026, Personal Assets Trust’s comparator is being changed from RPI to CPI. RPI lost its National Statistic designation in 2013 and UK government bodies, including the Office for National Statistics, have stated the metric as statistically flawed, discouraging its use in favour of CPI. It will be effectively phased out by the government in 2030. Many public and financial institutions have already transitioned away from RPI, and we have received feedback from shareholders requesting inflation reporting against CPI. CPI is now widely recognised as the UK’s standard measure of consumer price inflation and is considered more suitable for assessing the long-term performance objective of the Company.

[1] Capex refers to capital expendituremany of today’s fragilities. OpenAI’s fortunes are tied to a handful of the largest listed companies; a broader questioning of its business model would have widespread ramifications for asset prices.

The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-asset Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund.

Performance data provided is either calculated as net or gross of fees as specified in the relevant slide. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. This presentation may also contain forward-looking statements that are based on current expectations, estimates, forecasts, and projections. These statements are not guarantees of future performance and involve certain risks and uncertainties which are difficult to predict. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2024. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“”SEC””) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2026.