No Such Thing as a Free Trade

In the world of financial markets, where a tendency towards complexity and intellectual cartwheels often obfuscates simple truths, it can be clarifying to speak to someone one step removed. Such was the case when a family member asked me, ‘’Will the tariffs, enacted by the US, be paid for by US businesses?” The answer is a simple yes. And yet, according to a poll by Ipsos, this was understood by only 45% of American adults at the end of 2024. Amazon toyed with the idea of making the cost of tariffs explicit to consumers, by breaking out ‘import charges’ next to the listed price on each of its products, so that customers knew the source of price increases being passed onto them. The company ultimately backtracked from what would have been an economically transparent but politically inflammatory move.

This tug-of-war between economic reality on the one hand, and politics on the other, hits at the core of what is happening in the United States. Trump won electoral support by tapping into a feeling and, for a substantial portion of the population, a reality that free trade had left many behind. At the heart of his promises to disaffected voters has been a pledge to revive the country’s industrial heartland, recreating manufacturing jobs that have been lost to lower-cost exporting nations. As is so often the case with populist politics, the story is compelling, but the economics are more nuanced. Although not without trade-offs, free trade has in aggregate been a boon to the US economy. According to the Peterson Institute for International Economics, by 2022 the liberalisation of trade since WWII had increased US GDP by about 10% — approximately $2.6 trillion. The benefits show up in higher real incomes per capita, lower consumer prices and enhanced competitiveness, forcing US companies to be more innovative and productive than they otherwise would.

As the law of comparative advantage has reigned, manufacturing has moved away from the US. In turn, the US’s services and technology sectors have ballooned and been exported with great success to the rest of the world. This latter fact is glossed over by the current administration. Meanwhile, the costs of tariffs are poorly understood. Somewhat contrary to popular perception, tariffs are likely to hit the poorest hardest, since a higher proportion of their income is spent on imported goods. As for bringing jobs back to the US, the fact that it takes over four years for a new auto plant to reach production points at the difficulty in turning the switch back on overnight.

Liberated at Last

The 2nd of April, or ‘Liberation Day’ as it was heralded by its architects, saw the proposal of average tariffs on US imports of >30%, the highest since the 1930s. The prospect was met with intense market dislocation with the S&P 500 falling -12% and the FTSE All-Share -10% over the following four working days. Consumer and business confidence plummeted, to four and 12-year lows respectively. With the economic consequences of tariffs yet to be seen, share prices in this past quarter have generally been dictated by news flow. With the incremental headline becoming less negative since the start of April, markets have recovered to make new all-time highs.

There is lots to be cautious about. Uncertainty paralyses decision-making – and survey data suggest that many businesses are postponing hiring and capital expenditure decisions. Whilst the average tariff will likely settle below the initial proposals, the ultimate rate will still act as a tax on US business and, where costs are passed on, the US consumer. We see little value in attempting to precisely forecast most things, and we are certainly clear that we have no edge in predicting what Trump will do next. We maintain our focus on valuations, seeking to understand the outlook they are pricing in and what, positively or negatively, could cause this to be wrong. It is this assessment of individual stocks that drives the equity allocation. Investors should think of this process as incremental most of the time, with the ability to mobilise quickly when markets fall.

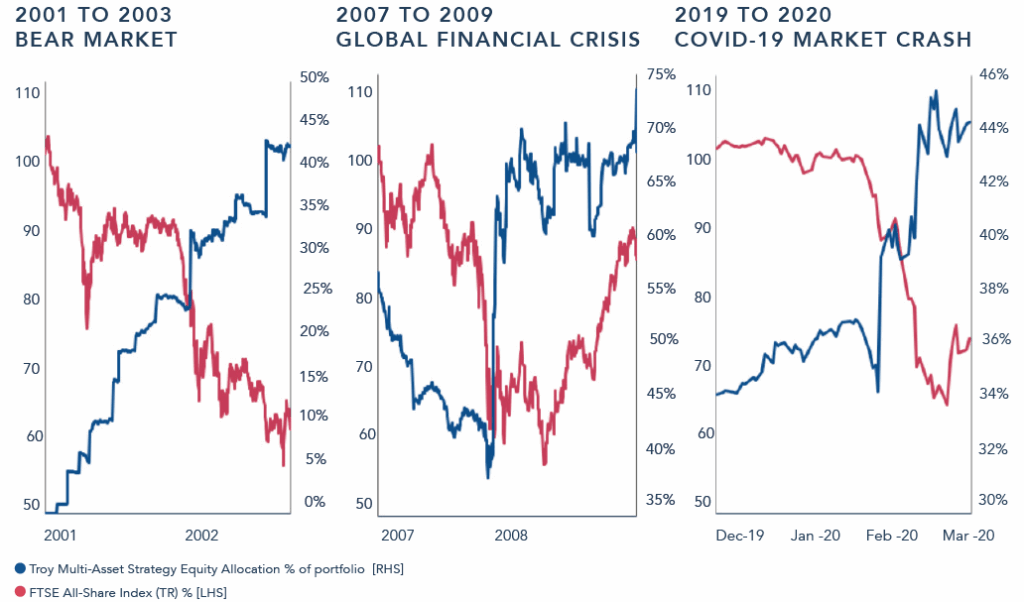

Walter Deemer, head of Putnam Investments’ Market Analysis Department in the 1970s, published a book in 2019 called ‘When the Time Comes to Buy, You Won’t Want To’. There are several things which help guide us during moments of dislocation, but perhaps most important is awareness of Deemer’s point that the best investment opportunities often arise when it is emotionally most difficult to act. We are fortunate that our mandate allows and encourages us to go against the grain. Our muscle memory has been built from acting during previous crises (see Figure 1). In hindsight, we were too cautious, but we had been leaning back from equity market risk since 2021. Having said that, entering 2025 with less than 30% in stocks put us on the front foot, with plenty of dry powder, when markets lurched down in April. We added five percentage points to new and existing holdings the week commencing Monday 7th April. Whilst the S&P 500 had fallen -18% from its peak, the strategy had only drawn down -2%. We took the view that valuations on a number of our equities had fallen to attractive levels and, had the market fallen further, we had scope to add more.

Figure 1: Dynamic asset allocation in market drawdowns

Source: Troy Asset Management Limited, 30 June 2025 . Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Asset Allocation and holdings subject to change. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

As it was, the market bottomed a couple of days later. We added a further 2% in April and May, to companies which had not immediately recovered, with the result that the strategy’s equity weighting now sits at 40%. This is slightly below the mandate’s long-term average, reflective of our continued concern that the range of outcomes remains wide, and that valuations generally are now factoring in something more optimistic.

Quiet Power

We sit alongside a team of talented colleagues who are focused on identifying the best businesses in the world. We work with them to find companies whose durability and consistency can play a central role in preserving and growing our investors’ capital. Our equity selection framework can be viewed through two lenses – the financial characteristics we look for (the outputs), and the qualitative characteristics that underpin them (the inputs). Neither can exist without the other – great returns with no strategy or runway for growth are unsustainable, whilst a great strategy or management team with unproven returns is a leap of faith too far for our mandate (we are not in the business of Venture Capital).

One company we have identified with both a strong track record and a clear path to future value creation is Hubbell. Hubbell manufactures equipment for the transmission and distribution of electricity across the US grid. The company has grown its revenues at 5-6% compound over the last 5, 10 and 20 years and has a tangible return on invested capital of just under 50%. We can see both characteristics sustaining into the future. Hubbell’s market share (estimated at 20% and twice the size of the nearest competitor) is stable and steadily growing, reflecting its position as the leading supplier of essential parts. From cable connectors to lightning arrestors and insulators, these essential pieces of equipment cost on average $50, but damages can easily run into the tens of millions if they fail. Founded in 1888, Hubbell’s reputation for reliability, coupled with unrivalled breadth of product offering and the long life of its products, make customer relationships incredibly sticky. Strong pricing power comes from the strength of the brand, the mission critical nature of the products and the fact that they tend to constitute only ~5% of above-ground power line costs.

Competitive advantage counts for little if your end-market is shrinking. Fortunately for Hubbell, the runway for grid investment is long. Just accounting for the ongoing maintenance required to keep the grid running, we expect the company should grow its sales at a mid-single digit rate. Going forward, there will be greater demands on top of this, ranging from data centre usage to electric vehicles and the need to harden the grid against climate change. The International Energy Agency estimates that the global grid needs to expand 2-3x to support growth in demand, with electricity moving from 20% of global energy consumption today to 50% by 2050. The company does not give guidance beyond the current financial year, but we suspect that the rate and durability of its returns are underappreciated. We bought a holding for the mandate at 20x earnings in May.

The existence of companies like Hubbell, at a market capitalisation of $20bn, speaks to the depth of opportunity in US capital markets. There is a lot of talk of the end of US exceptionalism – and the fact that the US stock market, which peaked as a share of global markets at 70% towards the end of 2024, may be more challenged going forward. Whether it will return to 70% is not of great relevance to us since we do not track the index. What remains clear however is that the US is still home to an array of exceptional businesses, and we do not believe that the aggregate conditions for their future success are dramatically altered. These conditions comprise, among others, a culture of risk-taking and entrepreneurialism, access to capital, and a large single market within which to scale.

Trust issues

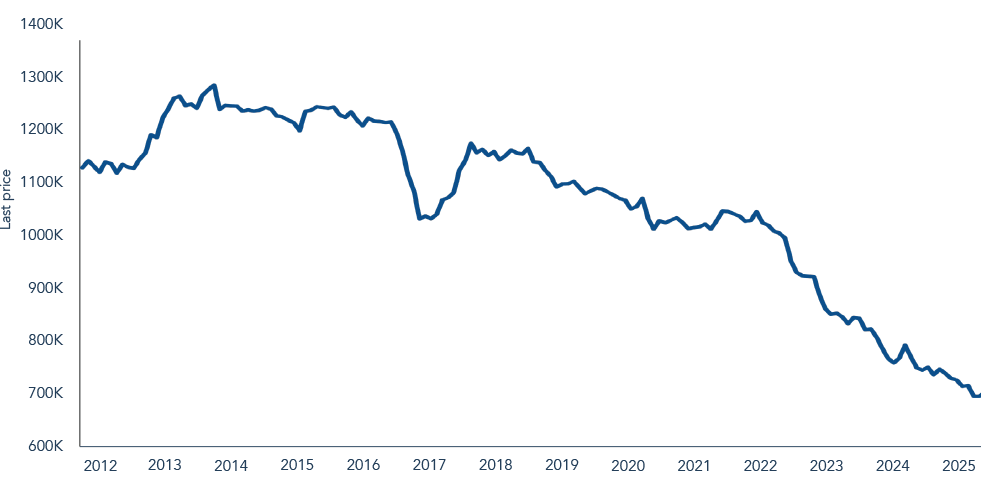

What has likely changed more fundamentally is trust at a sovereign level. China’s holdings of US Treasuries peaked in 2013 (see Figure 2). In the same year, deputy governor of the People’s Bank of China, Yi Gang, was quoted in China Daily saying, ‘It’s no longer in China’s favour to accumulate foreign-exchange reserves.’ Whilst this can be linked to the liberalisation of the Chinese currency, it also coincided with comments from the Chinese authorities about the US’s Quantitative Easing programme. It would be reasonable to conclude that trust in the US dollar was already waning back then in the aftermath of unprecedented monetary easing.

Figure 2: China’s holding of US Treasury Securities

Source: Bloomberg, 30 June 2025.

More recently, in February 2022, the US and its allies implemented sanctions, freezing c. $300bn of Russia’s FX reserves. This effective weaponisation of the dollar set off alarm bells for central banks around the world. The corollary of this has been a bid for gold. We expect that ‘de-dollarisation’ continues, with the events of April providing another blow to the US’s world reserve currency status. A survey of Central Banks by the World Gold Council showed that, of the 72 central banks surveyed, 76% expect to hold higher reserves in gold five years from now. Meanwhile, 73% expect to hold fewer dollars. Somewhat perversely, if the US administration succeeds in its goal of reducing deficits with the rest of the world, there will also be fewer dollar-denominated revenues to be reinvested back into US Treasuries in the future.

US dollar reserves today comprise c. 58% of central bank assets today, down from 65% a decade ago. This still represents a majority share, subject to reallocation over time. Gold has now overtaken the euro as the second-largest reserve asset globally, pointing to a paucity of credible, liquid alternatives. Whilst it is unlikely that the dollar’s importance diminishes overnight, we think that investors will look back on the events of April as another accelerant in its longer-run decline.

Figure 3: Central Bank FX Reserves

Source: Bloomberg, 30 June 2025.

We have moved the portfolio to reflect this. Having entered April with a net 25% in dollars, we reduced this to 15% in the week that followed the tariffs. It now sits just below 10%. We actively manage currency exposures, defaulting to hedging the exposure back to sterling if we do not think we are being rewarded for the risk. Historically, as the world’s reserve currency, the dollar has performed a useful role over time, providing protection in the portfolio when equity markets fell. The fact that this relationship broke down in April we suspect may be a harbinger of things to come. We have invested just under 10% of the portfolio’s liquidity into short-dated Japanese government bonds. We expect the yen to be another beneficiary of the move away from the dollar over time. Importantly, and a function of both the existence of a large carry trade as well as investors’ perception of the currency, April underlined the yen’s propensity to behave as a safe haven when equities are weak. The yen is also substantially undervalued versus both the dollar and sterling.

Non-zero Sum

According to research firm 13D, there is a joke circulating in Chinese circles that the proposed tariffs are ‘Making China Great Again’. Beijing has spent the past eight years (since Trump 1.0), preparing for a trade war, strengthening relationships with ASEAN, South America, the Middle East and Africa. The US meanwhile remains highly reliant on Chinese supply chains, in particular when it comes to strategic metals and rare earths. China’s most recent export data appear to speak to the country’s resilience. In 2024, the US accounted for just under 15% of China’s exports. In spite of 30% average tariffs from the US today (down from 145% in April), China still managed to grow its customs-reported exports +5.8% in June as growth from Southeast Asia and the EU more than offset the decline in demand from the US.

The contrast between China’s actions and those of the US speaks to a widening gulf between the way the two nations are thinking. Harvard Professor Stefanie Stantcheva wrote in The Economist this month, ‘To understand America today, study the zero-sum mindset… If China benefits from trade with America, America must lose…If immigrants find work, they must be taking jobs from citizens.’ She examines the backgrounds that tend to engender zero-sum thinking, from growing up with slavery to generations that do less well than their parents. It is clear that inequality lies at the heart of the issue. It seems likely therefore that tariffs, due to their impact on the poorest consumers, risk intensifying the zero-sum mindset. Likewise, the Big Beautiful Bill, signed into law on 4th July, is estimated to hurt the poorest most.

The world is competitive, but that fact should spur greater collaboration and innovation, not less. Within our mandate, we are fortunate that stock picking sits at the centre. It is hard to be resolutely pessimistic about the world when observing the non-zero-sum successes of businesses operating in areas of growth and change. The best companies will take tariffs firmly in their stride, spending more time on factors of greater importance to their bottom line and where they have agency over the outcome. It is by embracing these opportunities that we will ultimately succeed in protecting (and growing) our investors’ capital.

Meanwhile, we are keeping a firm eye on the risks that, for now, have receded into most investors’ rear-view mirrors. At the start of this year, we were cautious about how far animal spirits, supported by hopes for AI and a pro-business administration, had run. Despite the turmoil of the past quarter, those spirits are back. It is unlikely that the largest tariff increase in the post-war period will leave the world in a better state than it was beforehand. We therefore expect more volatility and will use this to add to companies on a greater margin of safety than we see today.

The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-asset Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund. Performance data provided is either calculated as net or gross of fees as specified. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Although Troy’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness of any data herein. None of the ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2025. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence. Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2025.