Higher for Longer

In September, the yield on the 10-year US Treasury bond reached 4.8%, its highest level since 2007. This coincided with, or rather precipitated, weakness across asset classes. We have witnessed a shift in expectations since the start of this year. In January the outlook, as priced by bond markets, was for rates to peak below 5% in June 2023, with cuts beginning in July. This contrasts with today, with rates now expected to stay above 5% until September 2024.

There appears to be an emerging acceptance that the Goldilocks world which we have inhabited for so long, where growth was neither too hot nor too cold and monetary policy was ‘just right’, has already given way to a more bearish reality. There are several plausible drivers for the rise in bond yields over recent weeks but arguably the most important has been the Federal Reserve’s commitment to keeping rates high to tame inflation. This has coincided with a growing consensus that the US economy is headed for a soft landing. Without a recession, it will be much harder for the Federal Reserve to reverse tack and ease monetary policy.

We remain sceptical that such an immaculate disinflation can be achieved without higher rates having a derailing impact on growth. That said, regardless of the ultimate economic outcome, we view the recent response in equity valuations to be more rational than the ebullience of the first half of this year. We think it is likely that rates will remain structurally higher in future, notwithstanding inevitable fluctuations if we enter an economic downturn. And this has implications for asset prices. In September, equity valuations fell to reflect a higher cost of capital, the sectors most impacted being those generally viewed as ‘bond proxies’. These include the likes of consumer staples, real estate and utilities, where the regularity of cash flows and of dividend payments makes them more akin to fixed-income securities in their profile of returns. (It is worth noting, particularly in the case of consumer staples, that the best companies are quite unlike bonds in their ability to grow and to pass on inflation to their customers).

We have seen such bond-yield-led selloffs before – notably in 2013, when the first ‘taper tantrum’ occurred in anticipation of the end of quantitative easing. In the seven years that followed, the Federal Reserve added a further $4tn in bond purchases to its balance sheet. Another troublesome year for investors was 2018 when higher-than-expected wage growth at the start led to fears over how high interest rates might need to rise in response. In December of 2018, the US 10-year yield climbed to over 3.2%, its highest level in over seven years. This was swiftly followed by the ‘Powell Pivot’ in January of 2019 when the Chairman of the Federal Reserve committed to a pause in the tightening cycle on the premise that inflation was not a threat. These periods of bond and equity weakness were notable for their scarcity in the 2010s – a decade when, for the most part, good news was good news and bad news was regarded as good news too. Equity investors had two ways to win as bond yields made lower lows and equity valuations higher highs. If anything, the muscle memory built up from those temporary setbacks encouraged investors to buy the dips, because monetary policy always came to the rescue.

The current setback for equities is different in nature. Unlike the bond-led selloffs of the past decade, recent equity market weakness has not arisen in anticipation of rate hikes. It is materialising in their aftermath. There may be more to come, but rate rises of generational proportions have already occurred. And it is clear from the rhetoric of the Federal Reserve that rates will remain at higher levels until they are ‘confident that inflation is moving down sustainably toward our objective’. In an ostensibly resilient economy, markets have begun to contemplate a structurally higher cost of capital. This seems prudent to us. As we have written about previously, we expect inflation over the next few years to remain higher and less stable than most market participants are used to. This is likely to be attended by higher nominal rates, uprooting the valuation yardstick of the past fourteen years.

Scot-free?

‘Happiness is the gap between expectations and reality, so the irony is that nothing is more pessimistic than someone full of optimism. They are bound to be disappointed.’

Morgan Housel, Investor and Writer

As investors continue to digest higher rates, another threat to equity markets lurks unseen. That is the risk to earnings from slower economic growth. The consensus earnings growth for the majority of listed companies does not currently make any allowance for a recession. In fact, for the S&P 500, aggregate earnings are forecast to grow +17% over the next two years. Let the good times roll! We are not in the business of making precise economic forecasts, but we do take care to consider expectations versus the potential for disappointment. It is unsurprising that the more time elapses, the less likely investors are to worry about the risk of a recession; it is human nature to believe that the longer you get away with something, the less likely you are to get caught. And this false sense of security can spur people on to bigger and bolder bets, hence why market collapses are usually preceded by hubris. 2021 epitomised this, with the COVID experience (a sharp fall in markets followed by a swift recovery) validating a narrative whereby the downside was capped.

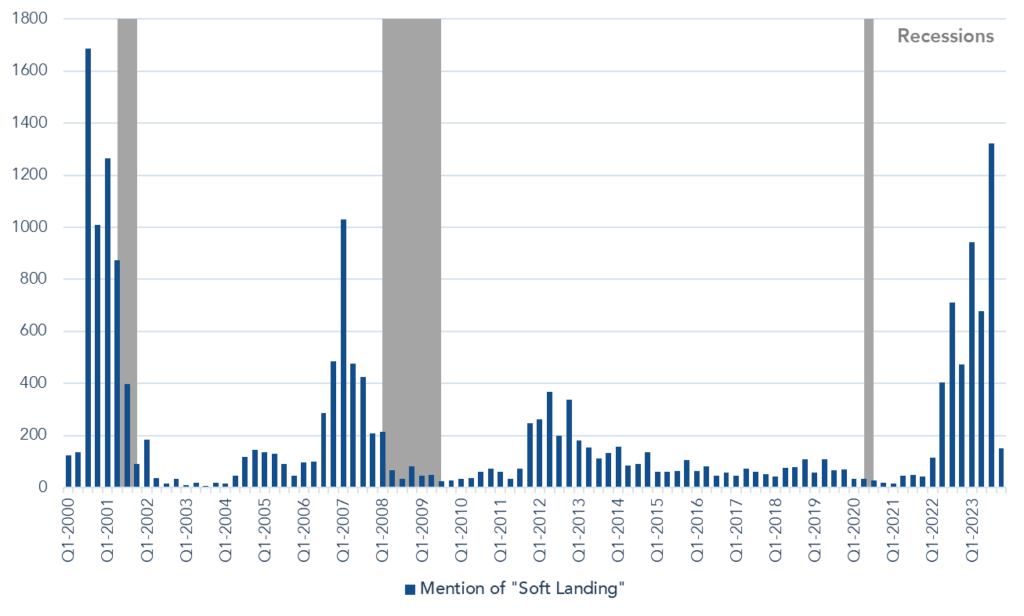

Whilst confidence around the economy is starting to have a less categorically positive impact on markets, any threat to a soft landing is likely to be negative. Even in a mild recession earnings tend to fall c. -20%. Last month Bloomberg published an insightful article exploring the backward-looking measures which govern monetary policy, notably levels of unemployment, which we referenced in last quarter’s report. The article also showed a chart (Figure 1) illustrating the frequency with which ‘soft landing’ is mentioned in company earnings calls. History shows that, ex-COVID, recessions this century have been preceded by calls for a soft landing. This repeatedly ignored the reality that the vast majority of interest rate hiking cycles are followed by recessions – with a lag. We have written at length about ‘long and variable lags’, but some facts are worth reiterating. Ex-COVID, the past two US recessions (2008-9 and 2001) occurred 18 months and 10 months respectively after the final rate hike. If we simplistically apply this precedent to today, assuming no more rate rises, a recession might not occur until the end of 2024.

Figure 1 – Mentions of “Soft Landing” in Company Reports and Transcripts

Past performance is not a guide to future performance

Source: Bloomberg, 1 October 2023.

Where the wind is blowing

An understanding of human behaviour and a knowledge of historical patterns can help a cautious investor in holding their nerve during periods of growing complacency. But the fact that most people were wrong last time does not in and of itself disprove the bullish thesis today. For this, we must look to the data to ascertain whether or not borrowing costs still matter. The answer is they do, the degree to which depending on the country and sector of the economy. Some are going to feel it more than others, and at different times. The UK has faced similar rate rises to the US over the past 18 months, but its consumer is more exposed. Household debt as a portion of GDP is higher in the UK (88% versus 65% in the US) and, critically, more of that debt is impacted by higher rates in the near term. Of the nearly 9 million mortgages in the UK, around half are estimated to have already seen a rise in servicing costs since the end of 2021, when mortgage rates started to increase, and a further 4mn households are due to be impacted by the end of 2026 as they come up for refinancing.

Unlike the UK’s short-duration (2-5 years) mortgages, the US’s tend to have 30-year terms, extending the lag with which higher rates are felt. For the 30% of household debt that is not mortgage-related (personal loans, auto loans etc.), we are starting to see a pick-up in delinquency rates. These shifts may be at the margin, and currently mitigated by strength in employment and a declining buffer of excess savings. Nonetheless, they are instructive in their direction. It is important to recall that recessions do not require for activity to fall off a cliff; rather it is the rate of change that counts. GDP can still be a vast number but if it is smaller than a year earlier for two quarters in a row, that constitutes a recession.

Whilst the consumer picture is mixed, the outlook for businesses in the US is more negative. We listened to a call recently with the Chief Economist at the National Association for Credit in America. He identified businesses rather than consumers as being first in line for trouble from higher rates. This is evident from a number of sources. A research paper published by Federal Reserve economists in June concluded that 37% of nonfinancial companies in America were in financial distress, with financial distress defined as ‘close to default’. The analysis echoes the fact that the number of companies having registered for default so far this year is at its highest level since 2009. This is hardly surprising when one considers that, according to the NFIB US small business survey, borrowing costs for small businesses have risen from 4% during the pandemic to 10% today.

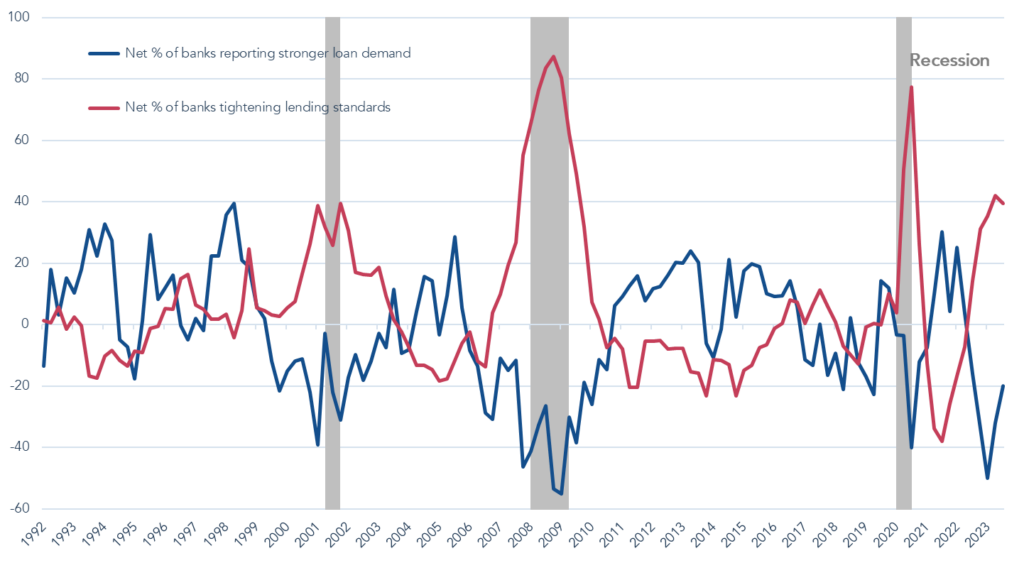

We often hear the response that businesses today are well capitalised, with most of their debt not due for imminent refinancing. This is true of many publicly listed companies but it ignores the swathe of small businesses, with less than 250 employees, which account for 74% of jobs in the US. And it is these businesses which rely on bank loans since they are unable to access public markets to borrow. This is rendered more problematic by the fact that many regional US lenders are struggling with their own funding models, as the cost of deposits has risen. The demise of Silicon Valley Bank in March exposed the extent of this vulnerability. The result is that not only has demand for loans fallen to levels consistent with a downturn, but banks have also tightened lending standards a similar amount (Figure 2). In this context, the findings of financial distress by the Federal Reserve’s economists are hardly surprising.

Figure 2 – Net % of US banks reporting stronger loan demand and tightening lending standards

Past performance is not a guide to future performance

Source: Federal Reserve – Senior Loan Officer Opinion Survey on Bank Lending Practices, Jefferies. Data as at July 2023.

We also hear that many small companies have hoarded labour, having struggled to find staff in the aftermath of COVID. In most circumstances, labour is the hardest cost for companies to cut; not only are layoffs expensive but, when a recovery does come, re-hiring is usually more time-consuming and riskier than retaining the staff you had. It is little wonder then, especially in today’s post-COVID environment, that cuts to labour are not the first indicator that something is amiss.

Looking forward

In the context of a more challenging environment for fixed income, it is worth highlighting how the index-linked bonds (linkers) in our portfolio have fared this year. Of the portfolio’s holdings, all bar the two longest-dated securities have generated a positive absolute return in the year to-date, and the asset class overall has been around flat in terms of contribution to returns. This is in the context of modestly positive returns from the portfolio year-to-date. This is a little disappointing, but it is not surprising in the context of rising interest rate expectations (bad for all bonds including linkers). Also unhelpful to index-linked securities, has been the fact that market expectations for future inflation have not risen. The combination of these two things has meant an increase in real yields, i.e. index-linked bond valuations have fallen.

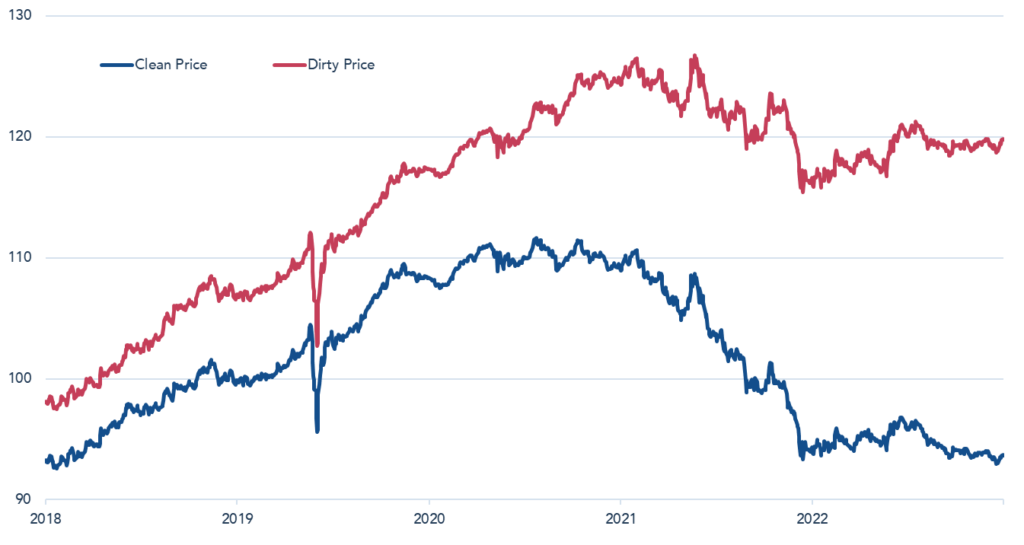

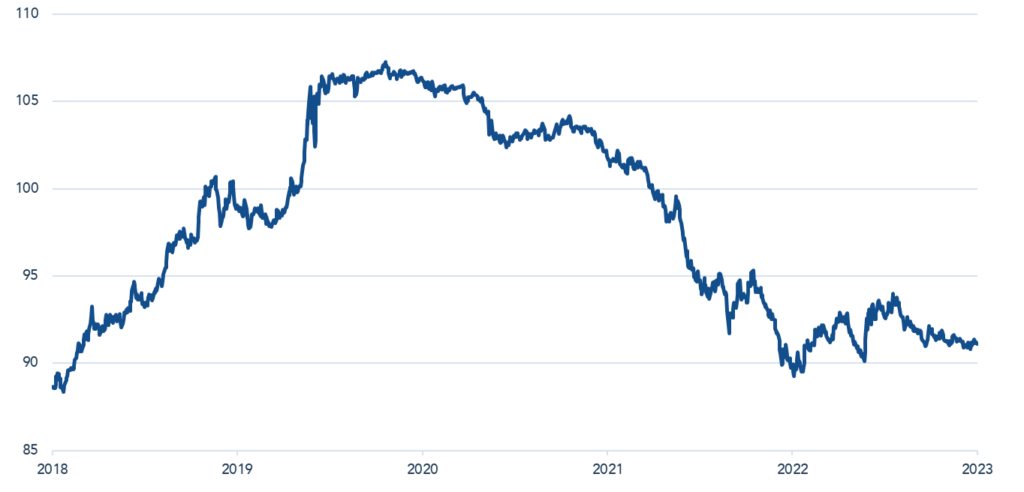

What has helped to offset this headwind is the fact that most of the index-linked bonds we own are shorter-dated. The value of these securities is more strongly linked to current rates of inflation, as opposed to expectations of what the market expects inflation to be in the future. As inflation this year has remained strong, the principal value of the bonds has risen; this is known as the inflation accrual. Figure 3 shows just how much this has mattered since the start of 2022. The ‘dirty price’ is the price of the bond including the inflation accrual and the next coupon to be paid; the ‘clean price’ is the price before indexation to inflation is taken into account. For comparative purposes, it is interesting to observe the price movement of a comparable, conventional bond with no indexation to inflation. Those securities have not held up well (Figure 4).

US Treasury Inflation Protected Security 0.125% July 2026

Past performance is not a guide to future performance

Source: Bloomberg. Data as at 17 October 2023.The clean price is the price of a coupon bond not including any accrued interest. That is, it doesn’t include the accrued interest between coupon payments. The clean price is typically the quoted price on financial news sites. Dirty price is the price of a bond that includes accrued interest between coupon payments.

Figure 4 – United States Treasury Bond 1.5% August 15th, 2026

Past performance is not a guide to future performance

Source: Bloomberg. Data as at 17 October 2023.

As real yields have risen, we have added to our index-linked holdings. In August we initiated holdings in US and UK 2026-maturing bonds, at positive real yields of over 2.5% and over 1.5% respectively[1]. This effectively locks in returns at these levels, plus whatever the inflation rate turns out to be over the three-year life of these bonds, if held to maturity. If inflation is, for example, 3.5% in the US, that will give a return of 6% annualised until 2026. We think this is attractively priced, government-backed protection against ongoing inflationary risks.

While we spend much of our time considering what could go wrong, and looking at the world through a macroeconomic lens, we make a priority of building our understanding of exceptional businesses. With invaluable input from the rest of the investment team at Troy, this comes in the form of research into new ideas and updates on existing holdings either owned or in our Investment Universe[2]. Meeting with management teams is an instrumental part of what we do, and we have had several company meetings this quarter.

Even as we enter what we believe will be a sustained period of higher and more volatile inflation[3] – with rates to match – we have confidence that opportunities in several areas are set to persist. It is likely that the world will continue to digitise, requiring spending on cloud computing, digital payments and, increasingly, AI. We are confident that, regardless of current turmoil in the Chinese property market, consumers in the country and across Asia more broadly will be wealthier in ten years’ time, to the benefit of a host of businesses. Our view on higher rates means that the price we pay really matters. We expect that the chance to buy at lower valuations will coincide with a deterioration in earnings. Ultimately though, our conviction in the longer-run durability of a number of business models makes us optimistic about the opportunity to build on the 25% of the portfolio invested in equities today.

[1] For reference, prior to this purchase, we have not owned UK index-linked bonds in the portfolio since 2019.

[2] Our investment Universe comprises c. 170 companies, owned and non-owned across markets, where we have conducted in-depth research to conclude that the business meets our quality criteria, and could therefore be purchased for our mandates at an appropriate valuation.

[3] See Investment Report 75 for a longer discussion of our inflation outlook.

Please refer to Troy’s Glossary of Investment terms here.

Fund performance data provided is calculated net of fees with income reinvested unless stated otherwise. All performance and income data is in relation to the stated share class, performance of other share classes may differ. Past performance is not a guide to future performance. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the fund’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. The UK Retail Prices Index (RPI) is a target benchmark for the fund as the Fund aims to achieve a return (the money made or lost on an investment) that is above the rate of inflation, reference to other benchmarks are for comparative purposes only. Tax legislation and the levels of relief from taxation can change at any time. Any change in the tax status of a Fund or in tax legislation could affect the value of the investments held by the Fund or its ability to provide returns to its investors. The tax treatment of an investment, and any dividends received, will depend on the individual circumstances of the investor and may be subject to change in the future. The yield is not guaranteed and will fluctuate. Any objective will be treated as a target only and should not be considered as an assurance or guarantee of performance of the Fund or any part of it. The Fund may use currency forward derivatives for the purpose of efficient portfolio management. The UK RPI figures shown are a combination of the actual rate of RPI, as calculated by the Office of National Statistics, and estimates for the previous month.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. In line with the Fund’s prospectus, the Fund is authorised to invest in transferable securities and money market instruments issued or guaranteed by an EEA state, one or more local authorities, a third country, or a public international body to which one or more EEA states belong. The Investment Manager would only consider investing more than 35% of the Fund’s assets in UK or US government issued transferable securities or approved money market instruments.

The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The sub-funds are registered for distribution to professional investors only in Ireland.

The distribution of certain share classes of the sub-funds of Trojan Investment Funds (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents or, as the case may be, the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

Certain sub-funds are registered in Singapore and the offer or invitation to subscribe for or purchase Shares in Singapore is an exempt offer made only: (i) to “”institutional investors”” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “”SFA””); (ii) to “”relevant persons”” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2023. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence. Morningstar logo (© 2023 Morningstar, Inc. All rights reserved.) contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2023.