A down year

“Sell when you can; you are not for all markets.”

As You Like It, William Shakespeare

Markets are never constant; they change and evolve like the weather. Trends can sustain for months and years, perhaps even a decade, but not forever. 2022 was a reminder of this. It was a poor year for financial assets, and investors will be glad to see the back of it. Inflation rose to forty-year highs in the UK and the United States. Combined with a record pace of interest rate hikes, this was something only the most battle-hardened investors had experienced previously. The ‘Bubble in Everything’ started deflating at the beginning of last year, but this accelerated following the outbreak of war in Ukraine.

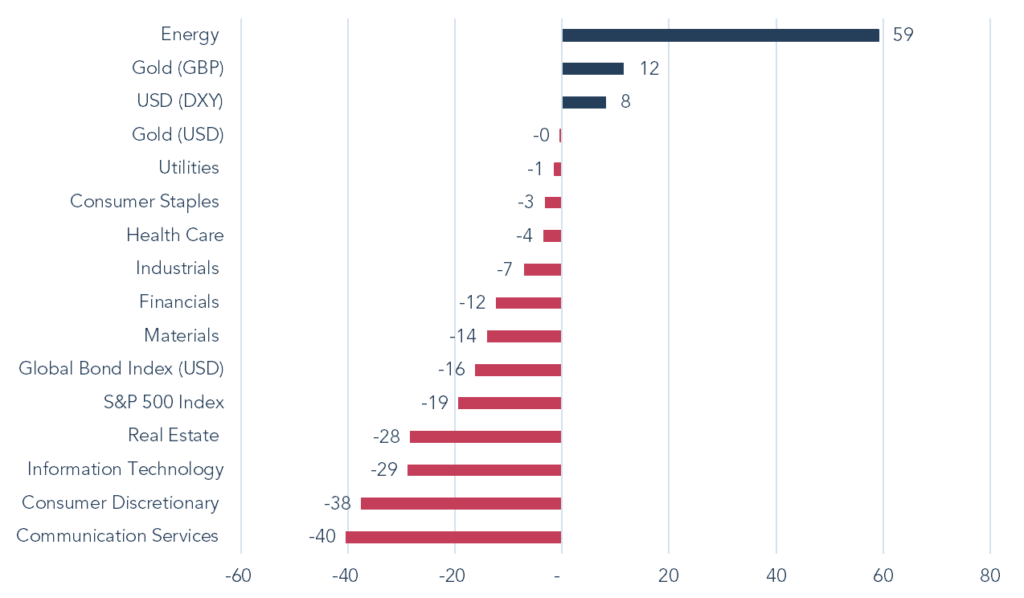

All major asset classes fell. 2022 was the worst year for stocks since the Global Financial Crisis in 2008, and the worst year ever for global bonds, which fell -16%. This would have meant that a traditionally stalwart ‘balanced fund’ of 60% equities and 40% bonds suffered its worst return in decades. Real assets, including real estate and ‘alternatives’, offered no cover, unable to resist the gravitational pull of a rising cost of capital. The gold price was flat in US dollars and rose a welcome +12% in sterling terms, doing a valuable job for our portfolio. Figure 1 demonstrates that diversification was hard to come by in 2022.

Figure 1 – Asset Class and S&P 500 Sector Returns in 2022 (%)

Source: Bloomberg, Factset, Robert Shiller, Yale University, http://www.econ.yale.edu/~shiller/data.htm. Local currency returns from 31 December 2021 to 31 December 2022.

Amid this turbulence, the Trojan Fund fell by -3.8%. While this is disappointing for us, as managers, it is a modest loss that we would hope to recoup quickly. The preservation of capital remains our priority.

The disappointment

Looking at our performance contribution, the main lessons to be learnt are not necessarily from how much we held in equities last year but rather how much of what. We entered the year with a modest exposure to risk assets, which proved to be correct. 2022 was a painful reminder, however, that from time to time the last will be first and the first last. The likes of Microsoft, a long-time winner and the greatest single contributor to returns in recent years, detracted from the Fund’s performance. In a falling market, recent underperformers such as Unilever came to our defence. We had reduced our equity exposure in 2021, at the height of the bubble, but with hindsight we should have reduced our winners more than we did.

US dollar strength and gold helped to partially offset the Fund’s falling equities but index-linked bonds disappointed. In a year of rampant inflation, these securities were anything but ‘inflation-linked’. Faced with historically low real yields1 at the end of 2021, we reduced our duration. The subsequent rise in nominal yields did not surprise us but, in the face of the greatest inflationary shock since the 1970s, the stability of long-term inflation expectations was remarkable. US breakevens2 remained firmly around the 2-2.5% level. This is reflective of a market anchored to the recent past. It also suggests a continued faith in the powers of central bankers to control inflation.

Déjà vu

History does not repeat but it does rhyme. Looking back over the past two years, there are plenty of similarities between the current period and the deflating of the ‘TMT’ boom of twenty years ago. Growth stocks, as represented by the NASDAQ, fell -30% last year following the 2021 tech-led euphoria.

The contrast with the 2000-2003 bear market is that there have been fewer places to hide. ‘Value’ stocks are not as cheap as they were then. These offered little protection in 2022. On the contrary, sectors like housebuilders, airlines and retailers performed poorly. As recession sets in, both growth and value stocks will become vulnerable to weaker earnings and further pressure on valuations. Earnings and share prices do not normally rise in recessions. We will need to be even more discerning about what we hold and at what price.

A similarity between 2000-2003 and the experience in 2022 was the summer’s bear market rally. Between mid-June and late August, the S&P 500 index regained exactly half its losses. These echoes of past bubbles can be far greater than anticipated, providing traps as the fear of loss is replaced with the fear of missing out. This is where secular bear markets (2000-2003 and 2007-2009) differ from the more typical -20% corrections we experienced in 2018 and 2020. Notably, in the latter instances, the Federal Reserve rode to the rescue of markets. Today the Fed is prioritising the fight against inflation in order to retain a semblance of credibility in its 2% target. The rallies of secular bear markets can be substantial, so it is critical to stay on track, unswayed by price movements and with eyes firmly on valuations.

A final similarity with the bear market of 2000-2003 is the rising importance of income and income growth to generate returns – in leaner times the contribution from dividend growth becomes dominant, as can be seen in James Harries’s latest report Income Matters No.4. In a recession, profits fall and there is risk of further valuation compression. In such conditions, dividend income can have a stabilising effect on the share prices of companies which continue to pay.

Inflation – temporary, transitory or lasting and volatile?

key in determining whether higher-than-usual inflation is sustained. For decades, the low paid have remained that way. This was due to several factors including globalisation, the opening up of China, the shift to offshoring and widescale immigration into and around Europe.

Today the low paid have improved bargaining power. They have suffered most from the cost-of-living crisis. Employers know this and are necessarily responding given labour shortages and the higher propensity of this cohort to move jobs. Despite the current economic headwinds, the UK and the US have almost record low unemployment. Employers do not want to risk rising staff turnover, which increases costs and adds to management complexity.

Lower immigration has meant fewer new entrants to the workforce at a time when many over-50s have retired early after COVID-19. Finally, there is the impact of industrial action. Between June and November 2022, 1.6 million days were lost to strike action in the UK, the greatest number since 1990. Although we are not yet at 1970s Winter of Discontent levels, when 10 million days were lost to industrial action, there seems little public support for the levels of unemployment that may be required to cool inflation.

This recent increase in bargaining power was confirmed to us at a recent meeting with a FTSE 100 chief executive who said that, whilst the highest salaried workers were not receiving pay rises (with competition for talent having abated), the lowest paid are receiving inflation-level increases. This is likely to prove more inflationary given the higher propensity of the latter to spend.

We expect 2023 to be less dramatic when it comes to interest rates and inflation, as post-pandemic distortions die down. Initial shortages of supply were followed by excesses in demand, as a result of fiscally strengthened consumer balance sheets and economies re-opening. This year, both factors should move in the opposite direction. Will this return us to where we were previously? We suspect not. Labour shortages reveal a different economy from the one we had before the pandemic.

Above zero

As we look forward, our US index-linked holdings are still pricing in higher real yields than they have done for over a decade. Nominal yields have risen but market expectations for inflation are little changed. We think this represents a contradiction that is unlikely to persist. The Federal Reserve, and central banks around the world, have hiked up the cost of capital with one goal in mind: taming inflation. Interest rate rises have not coincided with falling debt levels or structurally stronger economies. To the contrary, government and corporate indebtedness are higher now than they were five or 10 years ago, while growth is creaking. Rates are higher in spite of the economy’s waning ability to endure them. It follows therefore that they can only stay elevated if inflation does. If inflation is under control, then the rate rises can no longer be justified.

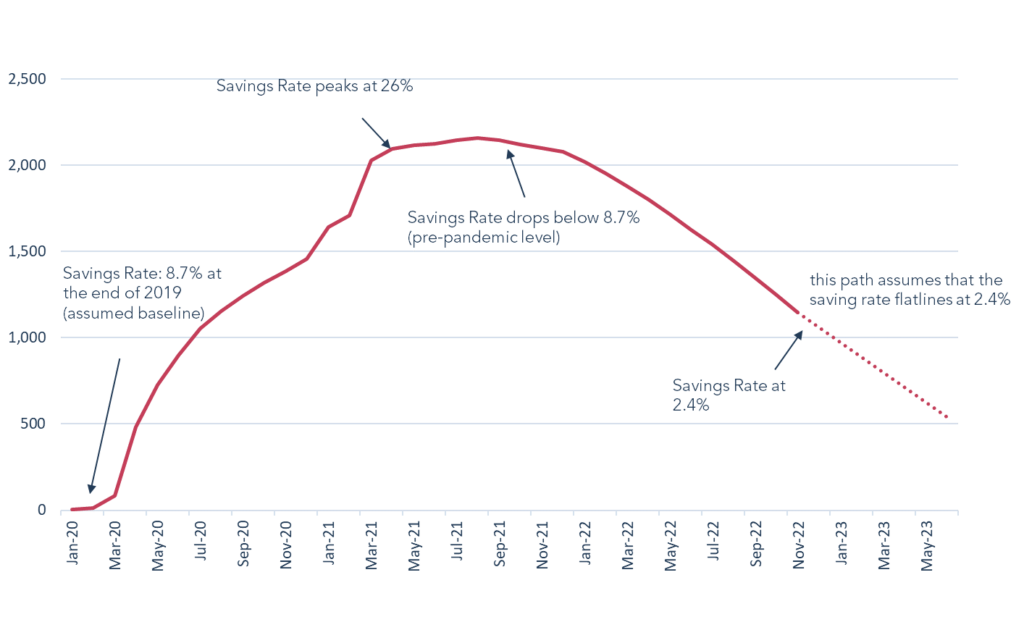

Figure 2 – US Household Excess Savings (USD bn)

Source: Haver, JEF Economics. Forecasts are not a reliable indicator of future performance.

Falling inflation is currently driving nominal yields lower. Breakevens were already pricing in such a scenario, so they have hardly moved. This has seen real yields fall, and the prices of US index-linked bonds rise. We expect the dynamic of slowing growth and slowing inflation to continue, at least in the short term, as we lap the commodity price peaks of early 2022 and as consumer savings (built up during the pandemic) are depleted (see above). As this occurs, many will declare the inflation battle won and welcome a return to the old regime.

But that may be premature. Nothing happens in a straight line and the Fed for one is not declaring victory yet. Longer-term, as described above, we think the inflation backdrop has changed. For breakevens to reflect this, we think the market will require more evidence that we are not on a return trip to the inflation stability of the past forty years. The experience of the 1970s, when inflation saw two major peaks, is something unfamiliar to most market participants, but it is likely at the forefront of policymakers’ minds. They will be wary of declaring victory too soon. The bond and equity markets on the other hand, so conditioned to a central bank that flinches at the first hint of pain, are already exhibiting a Pavlovian response. The direction of travel for rates from here will, in large part, depend upon the state of the economy and on the rate of unemployment. We are unlikely to know the full effects of a generational shift in the cost of capital for some time yet.

The 1970s may provide a helpful precedent, not so much in terms of the absolute levels of inflation reached (we think they will be lower this time), but in so far as those years presided over false dawns and changes in direction. Interest rates will move around, but we would expect them to remain higher than they have been in recent years, in response to a higher steady state of inflation. We would also expect breakeven rates of inflation to rise as investors are prepared to pay a premium for protection against higher and more volatile consumer prices. And we expect this to lead real yields lower, benefitting index-linked bonds.

Deflating the everything bubble

Both 2022 and this year-to-date have been punctuated by bouts of optimism, interrupting what we believe to be an ongoing, downwards trend. The tendency remains to travel hopefully, with investors holding out for an interest rate reversal. This is an innately human response. For as long as we can remember, investors have been used to the punchbowl being spiked, not removed.

There is plenty of belief that 2022 was an aberration and that we shall return to the recent normality of low inflation and low interest rates. But if we are right about risks to the contrary, then there are important ramifications for equity investors. 2022 had the effect of taking the froth out of the stock market, but valuations remain at or around the levels of 2019. We are effectively back to where we were when this bull market was 10 years’ old.

Looking back to early 2021, it is clear that the lows in bond yields created extreme distortions. This was the bull market’s final melt-up, characterised by rises in crypto, NFTs, the metaverse and meme3 stocks . Over recent years, investors had been paying ever-higher valuations for the same profits, gradually becoming accustomed to record earnings multiples. But stock markets, like the proverbial frog in boiling water, did not seem to feel the heat. Valuation came to be seen as almost irrelevant to subsequent returns, when we know the law of diminishing returns comes from higher starting valuations. The experience of the past decade, and perhaps even longer, as interest rates and inflation have been falling for forty years, is likely to be more a hindrance than a help to investors today. While that trend has come to a sudden end, market positioning is relatively unchanged.

A microcosm of this overvaluation can be seen in companies like the high-quality UK engineering business Spirax-Sarco. Spirax’s valuation rose from a fair multiple of c. 17x earnings in 2012 to c. 50x a year ago, with no discernible change in its business or underlying profits growth. Subsequently, it has fallen to around 30x, or back to 2019 levels. If these companies return to longer-run averages, we may be looking at a dull period of share price performance, during which growth in earnings is offset by valuation compression.

Bear markets occur unevenly and in different sectors. The technology sector was certainly the worst hit in 2022 but, as with our engineering example, there is room for this bear market to broaden out to other more highly valued areas. Why then doesn’t Troy delve into the murkier depths of the ‘value’ parts of the market? Because this is the area most vulnerable to cyclical downturns and subsequent dilutive equity fund raising. As always, we want our companies to pay us to own them, not the other way around.

Meanwhile, expectations are building for a recession in 2023 (arguably the most anticipated and telegraphed recession for years) but earnings downgrades have thus far been modest. This vulnerability is likely to come into focus as the year progresses. For now, we choose to sail close to the shore with a low equity exposure.

Words of encouragement for 2023

These days it seems almost quaint to send and receive Christmas cards. The tradition now is to send an email but there is something rather soulless about a round-robin corporate email. The number of cards I receive has fallen over the past twenty years, but I still get a few from clients and friends of Troy. One always stands out, from an erstwhile director of our company, with the same message every year, ‘Keep Going!’ We will.

1Real yields represent the difference between nominal bond yields and market expectations of inflation.

2The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.

3Meme stocks describe the shares of companies that have gained a cult-like following on social media, which can influence share prices.

Disclaimer

All information in this document is correct as at 26 January 2023 unless stated otherwise. Please refer to Troy’s Glossary of Investment terms. Past performance is not a guide to future performance. The document has been provided for information purposes only. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. The document does not have regard to the investment objectives, financial situation or particular needs of any particular person. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The views expressed reflect the views of Troy Asset Management Limited at the date of this document; however, the views are not guaranteed, should not be relied upon and may be subject to change without notice. No warranty is given as to the accuracy or completeness of the information included or provided by a third party in this document. Third party data may belong to a third party. Benchmarks are used for comparative purposes only.

Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Asset allocation and holdings within the fund may be subject to change. Investments in emerging markets are higher risk and potentially more volatile than those in developed markets.

The fund(s) of Trojan Investment Funds are registered for distribution to the public in the UK but not in any other jurisdiction.

The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents, or as the case may be the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

In Singapore, the offer or invitation to subscribe for or purchase Shares is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act. This document may not be provided to any other person in Singapore.

All references to indices are for comparative purposes only. All reference to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2023. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. The fund described in this document is neither available nor offered in the USA or to U.S. Persons.

Copyright © Troy Asset Management Ltd 2023