Data in the age of AI

One area where concern about Artificial Intelligence (AI) has been particularly acute is ‘information services’ companies: businesses that collect, organise, and sell data and analytics to professional customers. The fear is straightforward. If AI can synthesise and present vast quantities of information cheaply and at scale, what happens to the businesses that have historically charged for access to it? It is a reasonable question. We believe the selling pressure on the incumbent providers’ shares has been amplified by the rise of thematic investing. Investment banks now routinely publish ‘AI winner’ and ‘AI loser’ baskets, and the flow of capital into and out of these baskets can, in the short term, be largely valuation-agnostic, driven by narrative rather than analysis of individual businesses. These dynamics have driven a sell-off over the past year in several of the Fund’s holdings, including RELX, Experian, and the London Stock Exchange Group (LSEG). In this newsletter we set out why we remain confident in these holdings at current valuations.

A familiar anxiety

Over 18 years of UK equity investing, I have watched technology reshape, and in some cases destroy, entire industries. Regional newspapers, classified advertising, and high street retail for instance have all been devastated by the internet age. Whilst many businesses have ceased to exist, it is instructive to look at examples of those that have not only survived but thrived. Next plc for example, has managed to reinvent itself around e-commerce, whilst their peers fared less well. Autotrader moved from print to digital and strengthened its dominance. The lesson here is not that incumbents always win, but that those who combine a durable core asset with the management quality, and a willingness to adapt and invest behind new technology, often emerge stronger. That is the pattern that we have identified and look for, and it is what we believe we own in RELX, Experian, and LSEG.

The data that cannot be replicated

AI, and large language models (LLMs) in particular, pose a genuine challenge to businesses whose value rests on aggregating and presenting publicly available information. If the underlying data is accessible to all, the barriers to entry are meaningfully lower than they once were. This concern has real force for some information services businesses, and it cannot be dismissed entirely, even for our holdings.

But there are two fundamental reasons why we think RELX, Experian, and LSEG are considerably more resilient than the market has recently implied. The first is the nature of their data. The core assets of all three are proprietary, contributory, and in many cases real-time, built through privileged access to information not publicly available and, in our view, difficult to replicate. Experian’s credit bureau aggregates data from over 12,000 contributing financial institutions, and benefits from decades of lessons in how to extract useful signals from the information. Management have described it as effectively impossible to recreate. RELX’s largest business processes 400 million fraud and identity transactions per day, underpinned by a variety of unique contributory databases, such as receiving privileged information from every major US auto insurer. LSEG delivers live market data from nearly 600 exchanges and venues, combined with 30 years of proprietary price history across 100 million financial instruments. This data is valuable because it links the present to a past record that only LSEG holds.

The second reason is the nature of their customers. Lawyers, lenders, investors and scientists operate in highly regulated environments. A lawyer citing a case hallucinated by an LLM risks losing their licence to operate. A bank using an unverified credit score faces regulatory and financial liability. A quant fund relying on inaccurate market data loses money. This raises the bar for any new entrant considerably above what technological capability alone can clear and suggests that trust and proprietary data, built over decades, will not be easily disrupted. Moreover, as these customers look to embed AI into their own workflows, they are looking for these same incumbents to provide it, making the relationships more integrated, not less. LLMs’ utility rests on high quality information. LSEG’s chief executive recently noted that the world’s most sophisticated financial institutions, after up to two years of rigorous analysis, are “voting with their wallets” by contractually committing to LSEG’s data and workflow tools for up to seven years. The growing emphasis on accuracy, auditability, and regulatory compliance in an AI world may well reinforce the moats of these businesses, rather than erode them.

Performing as well as they ever have

Having met with management at all three companies in recent weeks, and with results recently reported across the board, our conviction has been reinforced rather than tested. There are no signs of disruption, quite the opposite. RELX delivered accelerating growth including 9% organic growth in its Legal segment and 9% underlying operating profit growth across the group as a whole. Experian upgraded its full-year guidance to the top of its 6-8% organic range, with earnings per share (EPS) on track to grow around 13%. LSEG delivered 7% organic growth in 2025, with EBITDA[1] margins exceeding 50% for the first time and EPS growth of over 15%. The technology appears so far to be accelerating their growth rather than threatening it.

No longer paying up for quality

The valuation journey of these three companies over the past 18 months tells an instructive story. At the start of 2025, they were widely regarded as AI beneficiaries, businesses that could potentially grow faster and harvest productivity gains, and their valuations reflected that optimism. We were reducing our positions at those levels. What followed was a sharp reversal. As sentiment shifted, the same businesses were reclassified as AI victims, and the selling accelerated sharply in January and February of this year, when at their lows their valuations reached around 14 times forward earnings. This was a period of indiscriminate selling, with digital stocks falling heavily regardless of the quality of their underlying assets.

Since then, encouragingly, some discernment has returned. RELX, Experian, and LSEG have each recovered around 20% from their lows, while many software businesses and other digital companies with more legitimate AI risks remain under pressure. The market is beginning to distinguish between businesses with genuine, hard-to-replicate data assets and those more vulnerable to the threat.

RELX, LSEG and Experian are the largest of a broader group of digital and data-driven holdings in your Fund that together represent around a fifth of your portfolio. The first chart below tells the valuation story clearly. The current digital holdings in the strategy collectively and historically traded at a valuation premium to the Fund’s holdings that rely more on ‘physical’ assets. In our view, the premium was justified by their superior growth, cash conversion and returns on capital. That premium has now all but disappeared.

Figure 1: Current Portfolio Digital vs Current Portfolio Physical Stocks Historic 12M Forward P/E

Source: Troy Asset Management Limited and FactSet, 28 February 2026. Past performance is not a guide to future performance. Price-to-Earnings (P/E) ratio is a valuation metric that compares a firm’s stock price to its earnings per share. “Digital stocks” refer to companies within the portfolio whose primary revenues are generated from digital products, software, or online platforms, while “physical stocks” refer to companies within the portfolio primarily producing or selling physical goods or asset-intensive services.

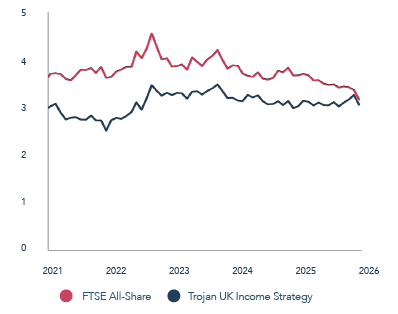

The second chart below makes the point directly for income investors. Unlike most UK Income Funds, we do not target the market’s dividend yield in constructing the portfolio, rather we aim for sustainable dividend growth from higher-than-average quality companies. The Strategy’s dividend yield has recently converged almost exactly with that of the FTSE All-Share. Put simply: investors are receiving market-level income from a portfolio of considerably higher quality businesses.

Figure 2: Troy UK Income Strategy vs FTSE All-share Forward Dividend Yield

Source: Troy Asset Management Limited and FactSet, 28 February 2026. Past performance is not a guide to future performance and income generated (if any) may fall as well as rise.

Retaining conviction

As discussed in our previous newsletter, valuation-aware, countercyclical share buybacks are one of the clearest signals of management confidence in intrinsic value. LSEG announced a £3 billion buyback at its full-year results, explicitly framing it as a response to what it sees as market dislocation. RELX upsized its buyback to £2.25 billion, almost 5% of its market capitalisation, and Experian launched a $1 billion repurchase programme in January 2026. We are very supportive of these actions at prevailing low valuations.

These companies have all navigated technological change before, and their core assets are among the hardest to replicate in their sectors. Their customers cannot afford to be wrong when experimenting with new technology, and management teams are investing assertively and dynamically to maintain and grow their relevance, leaning into these new changes rather than hoping it passes them by. Troy’s investment approach seeks to balance high-quality businesses and attractive valuations. At current prices, we believe we have both.

[1] Earnings Before Interest, Taxes, Depreciation, and Amortization

The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s UK Income Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund.

Performance data provided is either calculated as net or gross of fees as specified in the relevant slide. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. This presentation may also contain forward-looking statements that are based on current expectations, estimates, forecasts, and projections. These statements are not guarantees of future performance and involve certain risks and uncertainties which are difficult to predict.All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

Although Troy’s information providers, including without limitation, MSCI Solutions LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness of any data herein. None of the ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2026. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2026.