Buybacks, valuation, and the UK equity market

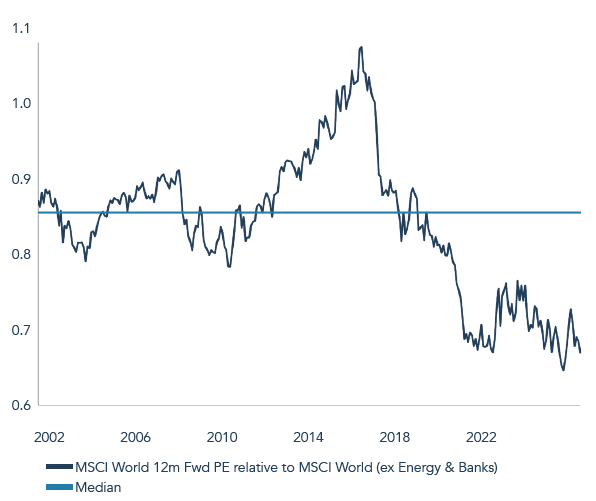

Over the past decade, there has been a persistent drumbeat of commentary noting the low valuations of UK equities relative to global peers. While the UK market has long held a discount to global benchmarks, the gap widened significantly in the wake of Brexit and has stubbornly remained. We are often asked what might trigger a re-rating or ‘re-appreciation’ of UK equities.

FIGURE 1 – MSCI UK 12M FORWARD P/E RELATIVE TO MSCI WORLD (EX ENERGY & BANKS)

Source: FactSet, 30 September 2025. Past performance is not a guide to future performance and income generated (if any) may fall as well as rise. All references to benchmarks are for comparative purposes only. P/E is price to earnings. LTM is last twelve months.

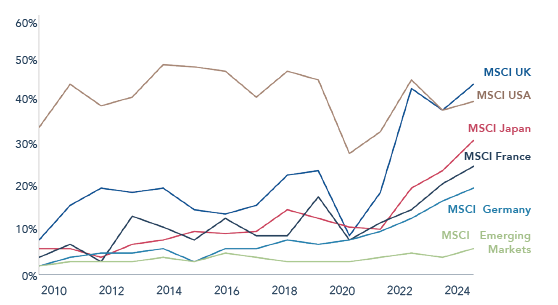

While many investors still seem hesitant on UK stocks, from a point of low valuations, and low expectations, not much needs to happen in our view to generate attractive returns. Pleasingly, companies themselves have demonstrated strong conviction in their value, with UK large cap share buybacks reaching record levels over the past few years (see figure 2). Some credit for this must be given to the COVID-19 pandemic, when many UK companies lowered their dividend payouts. This provided some relief from the shrinking UK market dividend cover that had been a feature of the preceding years and freed up more capital for buybacks. The UK now has the highest proportion of large cap repurchasers globally as shown below.

This enthusiasm for buybacks extends to your Fund, with c.70% of holdings by weight buying or having bought back shares in the past 12 months. We think more could follow in the future.

FIGURE 2 – PROPORTION OF LARGE CAP COMPANIES REDUCING THEIR NUMBER OF SHARES IN ISSUE BY AT LEAST 1%

Source: Schroders and MSCI, 30 September 2025. Past performance is not a guide to future performance.

Our thoughts on buybacks

“Price is what you pay, value is what you get” – Warren Buffett

We are generally supportive of this growing trend but are clear that any conversation on buybacks must be inextricably linked to that of valuation. We regularly discuss share repurchases with the management teams/boards of companies. Remarkably, we still find widely varying views and approaches towards their use.

Share buybacks are another capital allocation option alongside dividends, capital expenditures, M&A, or paying down debt/accruing cash. In an ideal world, any capital allocation decision is weighed against alternatives to deliver a rate of return that is attractive in both relative and absolute terms. However, the realities of such decisions can rarely be so clear cut. For example, dividends (the other form of shareholder returns alongside buybacks) tend to be treated as a sacrosanct commitment that are kept consistent over time. Boards are reluctant to cut them and markets tend to heavily punish the shares of companies that do, inferring the business to be in bad shape. Dividends are seldom started or stopped based on an ongoing relative judgment of their value versus other capital allocation choices.

Buybacks are often viewed as more discretionary, giving boards leeway to act opportunistically. This is good news as buybacks differ from dividends in a critical way – their value creation potential is price-sensitive. If shares are undervalued, the remaining shareholders (those who do not sell) benefit from a company buying back its own stock. If shares are overvalued, departing shareholders benefit at the expense of those remaining. Warren Buffett offers typically sage and succinct wisdom on this dynamic: “My suggestion: Before even discussing repurchases, a CEO and his or her Board should stand, join hands and in unison declare, ‘What is smart at one price is stupid at another’.”

Of course, boards and management teams do not operate with perfect information. Assessing the true value of a company (and thus a buyback) is no small feat – art plays a major role alongside science in any valuation exercise. And having foresight on the outcome of every capital allocation choice is impossible. There is always going to be a significant element of judgment. However, intuitively, companies should emphasise buybacks when they believe shares are significantly undervalued and vice versa. Looking at broad market patterns over time, almost the opposite happens – in times of market ebullience, buybacks are high, and in significant drawdowns, activity slows as illustrated below:

FIGURE 3 – S&P 500 BUYBACKS, $BILLIONS

Source: S&P Global, 30 September 2025. Past performance is not a guide to future performance.

FIGURE 4 – FTSE 100 SHARE BUYBACKS, £BILLIONS

Source: AJ Bell, 30 September 2025. Past performance is not a guide to future performance.

We do acknowledge that it is perhaps easy for investors in our ivory towers to criticise management teams operating real companies for this pattern. Times of widespread market or economic uncertainty naturally make companies more cautious with their capital. This is often by necessity if their profits are impacted with knock-on effects to leverage ratios. Highly cyclical or indebted companies may even need to issue new shares in order to survive. Nevertheless, we admire management teams who can demonstrate clear value creation with proactive, counter-cyclical thinking,1 buying shares opportunistically when they see value. Below we discuss some relevant examples from your Fund.

Some portfolio examples

Perhaps the best-known practitioner of buyback discipline in the UK market is portfolio holding Next plc. The company repurchases shares when it believes this will enhance earnings more effectively than alternative uses of capital. The simple rule of thumb is to divide expected profit before tax by the company’s market capitalisation (in effect a ‘profit yield’). If the number is c.8% or higher, buying shares is deemed to generate a relatively attractive return. Why 8%? This is roughly the long-term expected return on equity of the wider market – as evidence, the FTSE All-Share has delivered a compound annual total return between 7-8% over 10, 20, and 30 year periods.2 Therefore, 8% is a good ‘opportunity cost’ for the company and shareholders to consider. Through 2025, we have seen Next start and stop share purchases as the valuation and forecast return have fluctuated either side of the 8% level. If shares are consistently below this watermark, and Next keeps accruing excess cash, the company may opt for special dividends instead of repurchases. In effect, Next’s management are saying you may be better off deploying this cash for higher rates of return elsewhere, with c.8% possible from investing in the market as whole.

There is no perfect formula or target return but Next’s approach leads to a sensible, tactical policy where buybacks are naturally favoured at lower valuations. This logical and simple framework is surprisingly rare among the universe of listed companies!

However, even Next’s management team have to operate with imperfect information. They followed many other companies in suspending buyback activity in 2008 amidst uniquely tough economic conditions. In 2017, they repeated the action – at the time, Next’s share price and valuation were low but the company was suffering cannibalisation of its physical retail stores by ecommerce, creating pressures on profit and raising existential questions. Despite the low valuation, management opted for special dividends over buybacks. Justification was given as follows:

“In hindsight, we were wrong to not buy back shares in 2008 and we hope that hindsight will prove us wrong, on this particular decision, once again! But at this time of significant uncertainty, we feel that the decision to buy back shares is best left to shareholders themselves. And of course, shareholders can always use their special dividends to buy shares for themselves. Perhaps we have been overly cautious but companies rarely fail for being prudent with their shareholders’ money and in uncertain times such prudence is all the more important.” 3

In hindsight, 2017 too would have been an opportune time to repurchase shares, demonstrating the difficulty even skilled managers can have in getting capital allocation right. Nevertheless, the big picture has been Next reducing their share count by almost 70% over the past 25 years with good discipline, helping to compound shareholder returns at robust double-digit rates over this time period.

FIGURE 5 – NEXT PLC, SHARES OUTSTANDING

Source: Bloomberg, 30 September 2025. Past performance is not a guide to future performance.

To avoid the risk of being overly clever, other companies opt for a more ‘hands off’ approach. Portfolio holding RELX has been a consistent ‘share cannibal’ over the past decade but opts for an ‘irrevocable, non-discretionary’ share buyback mandate where the execution is outsourced to a third-party (an investment bank). This party agrees to buy a fixed cash amount over a defined period at their own discretion. While this limits RELX’s ability to capitalise on periods of lower valuation, it also reduces the risk of overpaying and mitigates potential issues under the UK’s Market Abuse Regulation.

RELX has continued its buyback programme over recent years as its valuation multiple has increased. This expansion reflects the accelerating organic growth of the business but brings with it the higher volatility possible at higher valuations and potentially lower prospective returns. Perhaps discretionary slowing of the buyback at high multiples in favour of other capital allocation could be more beneficial to shareholders? We think there is logic in considering it. However, we can see how RELX may have come to its current strategy; as a historically highly profitable, asset-light business, it has generated far more cash that it can feasibly reinvest organically. The company does acquire other businesses but assets in this sector tend to be highly priced and not regularly for sale. With RELX already paying a regular dividend, the buybacks become their default route to return excess cash. Relatedly, we have commonly found that shareholders tend to pressure companies to return ‘spare’ cash on the balance sheet, which often precludes management teams from simply letting it build-up. We would be in favour of more companies feeling they could have some latitude on this, providing some flexibility on the use of buybacks or other capital decisions.

In the case of RELX, we greatly admire what their management team have achieved and so are willing to give them the benefit of the doubt on their choices. However, we think it is crucial that companies deploying a persistent buyback must consider their ability and willingness to keep doing so through the tough times as well as the good (we discuss a relevant example below). As a highly defensive business, we believe RELX should be able to continue its buyback through the ups and downs of economic cycles, averaging out to a good return on investment for investors.

While we view RELX’s strategy as reasonable, in our view it is the skilled, tactical allocators like Next that tend to generate the most compelling returns from buybacks. It is no coincidence that the hugely successful CEOs profiled in William Thorndike’s superb 2012 book ‘The Outsiders’ made use of buybacks at scale and opportunistically when they felt share prices were clearly disconnected from true value. We think all management teams should know these case studies and try to reflect these playbooks. Sadly, some companies still fail to get the understanding or execution (or both) of share repurchases right. This can take multiple forms, for example:

- Procyclical behaviour

Outside of widespread macroeconomic events dampening market-wide buybacks (such as in 2008 and 2020), we have had some disappointing allocations and suspensions of buybacks in recent years. Diageo was continually buying back shares for several years, including as valuation multiples rose, but then suspended the process as falling profits reduced their capital flexibility. With today’s lower share price and valuation, alongside no repurchases, the execution can rightly be criticised in our view.

- Focusing on earnings per share (EPS)

In the press, and in our interactions with management teams, discussions of buybacks often focus on the obvious first-order impact – that as shares outstanding reduce, earnings per share are boosted – without noting the potential value destruction of buying at high valuations. We think this first-order thinking often features heavily in decision-making. In particular, EPS growth is perhaps the most common metric included in incentive-based remuneration for executives. This can strongly encourage the use of buybacks to hit EPS targets, regardless of valuation.

- Excessive use of leverage

Buybacks are often funded by fresh debt, effectively swapping equity for leverage. In the low-interest rate era that persisted in the 2010s, buybacks were particularly accretive to earnings per share as any incremental interest costs on debt were extremely low. With much higher borrowing costs today, repurchases done with debt at high multiples risk damaging shareholder value with minimal/no benefit to EPS.

- Offsetting dilution

Buybacks are sometimes viewed simply as a mechanical tool to offset dilution from employee share-based compensation. This is especially a feature of the US market but not exclusively. While it may seem ‘job done’ to keep share count flat, this confuses optics with economics, failing to recognise buybacks as a capital allocation choice with variable rates of return.

We think that in most instances of poor execution, management teams do not necessarily consider buybacks equivalent to other forms of capital investment. Changing this mindset should, in our view, go a long way to ensuring their actions are best aligned with shareholder value creation.

What about those doing no buybacks?

Some companies in your Fund have little or no history of buybacks. Our newsletter last year discussed those companies, such as Diploma, capable of regularly acquiring small businesses at highly attractive valuations/rates of return, making repurchases of their own shares relatively less attractive. This is in contrast to many M&A transactions where we think the risks from overpaying and combining separate entities can make buybacks a much more attractive prospect. Indeed, there seems obvious logic in management teams prioritising the shares of the asset they know best – the company they already run.

Meanwhile, other companies have formed a preference for dividends. Car and home insurer Admiral Group has historically earned exceptional returns on equity, leading to lots of excess cash flow. They pay a stable ordinary dividend which is supplemented by variable special dividends, often after times of exceptional profit generation when shares can be riding high (and so, like Next, perhaps sensibly offering cash to shareholders at times of high valuation/lower prospective return).

Concluding thoughts

Through a broad UK and portfolio lens, we are very supportive of the current material rise in buybacks alongside attractive valuations. Buybacks are neither inherently virtuous nor destructive, but another tool that can create value when correctly used. The hallmark of good buyback discipline is valuation-driven, countercyclical repurchasing4, funded by excess cash, and considered against all other capital allocation uses. Whether it is buybacks or M&A, decisions must be made with attractive rates of return in mind.

The simple message above all is that share prices matter. Management teams, like any thoughtful investor, should seek to buy low.

We recognise that boards and managers do not operate with perfect foresight and even the most skilled capital allocators will make mistakes. However, we look for clear, simple frameworks on how capital is used. We value skilled managers who can plainly articulate sound thinking on value creation and, crucially, who practice what they preach.

- Thinking and acting opposite to prevailing market or economic trends. ↩︎

- Bloomberg ↩︎

- Next plc 2017 annual report. ↩︎

- Buying back shares when the market is down. ↩︎

Disclaimer

Please refer to Troy’s Glossary of Investment terms here. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s UK Income Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund. Performance data provided is either calculated as net or gross of fees as specified in the relevant slide. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2025. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2025.