I hope that readers had a good festive break. We return refreshed and ready for 2023. In this short newsletter, I will review 2022 and touch on the Fund’s dividend outlook. I also include a reminder to investors of the most significant exposures within the portfolio.

2022 review

2022 was a challenging year for equity investors, with ‘macro’ factors dominating the headlines. High levels of inflation, rapidly rising interest rates, and geopolitical unrest conspired to profoundly impact global asset prices. Both the S&P 500 and the MSCI World Index declined by -18.2% total return (TR) in US dollars (USD). By comparison, the UK’s FTSE All-Share (TR) fared comparatively well, rising +0.3% in sterling (GBP), reflecting the strong performance of certain larger-cap companies such as miners, oils, tobacco, and some banks, which benefited from higher interest rates and inflation. In contrast, many Consumer Discretionary stocks, perceived ‘COVID winners’ and growth-oriented companies suffered from a material derating in their valuations or the direct impacts of inflation. Smaller companies also had a difficult year, with the FTSE 250 falling by -17.4% (TR) (GBP).

This was an unfavourable environment for our investment strategy, which focuses on high-quality dividend growth stocks and avoiding capital-intensive and cyclical banks and commodities. Over the year, the Trojan Income Fund returned -12.5%, which was a disappointing outcome. Reassuringly, despite some weak share price returns, the vast majority of portfolio companies continued to deliver strong operating performance and dividend growth in 2022.

In fact, in many cases we found that those companies delivering the most robust free cash flow1 and dividend growth suffered the most. Take industrial and healthcare distributor Diploma, a c.2.5% holding in the Fund and a stock we purchased in January 2021. Diploma managed to significantly upgrade their profit guidance over their financial year which resulted in them growing earnings and dividends per share +26% in 2022. In spite of this faultless execution, the shares ended 2022 down -17%. Even more staggeringly, at one point in the year they were down over a third. We observed a similar but opposite effect with many of 2022’s winning shares too, with instances of share prices rising well in excess of earnings growth. We suspect that after a year so dominated by the macro, and with interest rates and equity valuations having rebalanced significantly, share prices might be more closely correlated with fundamental earnings and dividend growth in 2023. Given the emphasis we place on resilient earnings and dividend growth, I would expect this to be to the benefit of the strategy.

Drilling into individual stock price performance, it was pleasing to see some large, core holdings prove defensive in the face of inflation. AstraZeneca, Unilever, Compass Group, British American Tobacco and Visa were the leading contributors to performance in 2022. The five stocks which detracted most were Croda, Fever-Tree, Experian, Domino’s Pizza and IntegraFin. These stocks underperformed for different reasons. Experian and Croda have generally continued to trade well. They each had very strong share price performance in 2021, benefitting from an upward rerating in their valuations, only to see this reverse in 2022 in the face of rising interest rates. Over three years, Experian and Croda have both delivered robust positive returns for the Fund. Domino’s, Fever-Tree and IntegraFin on the other hand have suffered to varying degrees from company-specific cost pressures. Encouragingly, all three continue to grow nicely and take market share, and so any softening of the inflationary environment ought to be their benefit. We continue to hold all five of these companies, confident about long-term dividend growth and outperformance from each of them.

Last year we became investors in the value-added distributor Bunzl and LSE Group, the world-leading financial markets and data company which owns the London Stock Exchange. We like their positions as global leaders in their fields, their resilient, growing cash flow and reasonable valuations (c.5% free cash flow yields2). Sharp-eyed readers will notice we are no longer investors in the industrial software provider AVEVA; we sold our holding following majority shareholder Schneider Electric’s bid to acquire the company.

We have learned much over 2022, but our core investing principles remain unchanged. We will continue investing in resilient, high-quality, cash-generative businesses capable of sustainable dividend growth funded by cash flow. Although commodity and banking stocks had a good run in 2022, we would caution against extrapolation and remain convinced that such capital-intensive and cyclical stocks will deliver poor risk-adjusted returns3 for investors over time, whereas those companies capable of consistent dividend growth across the whole market cycle will win out.

Reasons for optimism

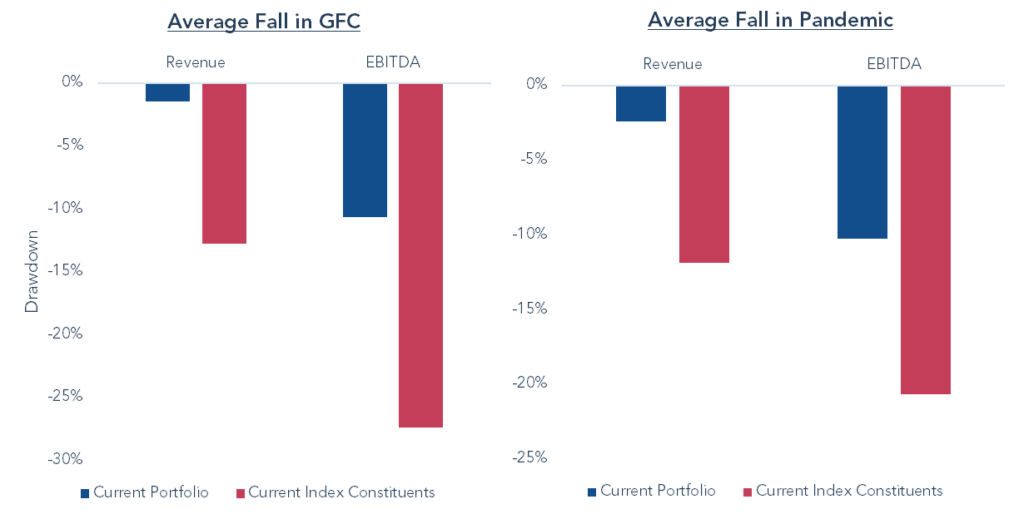

Despite a brutal past year, we are optimistic about the outlook for high-quality UK equities. The two big unknowns for markets in 2023 are likely to be i) the path of interest rates and therefore valuations and ii) the ability of companies to navigate a difficult earnings environment. In our view, the most severe adverse impact on equity valuations from higher interest rates following central bank rate hikes may be behind us. Valuation multiples for the UK market are depressed compared with the long-term trend, which bodes well for longer term prospective returns. I also strongly feel that after the debacle of September’s mini budget, the UK is on a much firmer footing with regards to government stability and fiscal prudence. When it comes to earnings, it seems inevitable that corporate profits will be under pressure. However, your Fund is overwhelmingly exposed to sectors and businesses whose earnings and dividends should prove more resilient than the market. While no two downturns are the same, we have seen this in prior episodes – the chart below compares the declines in revenue and profit (EBITDA4) for the current portfolio holdings versus the wider index during the Global Financial Crisis and the COVID-19 pandemic. We also think solid and well-established companies that pay growing dividends to investors will benefit in 2023’s more austere climate as the era of cheap money ends, and it is harder for new businesses to borrow heavily or run at a loss to disrupt the market.

Source: Bloomberg, Troy Asset Management Limited, 31 December 2022. Index is the FTSE 100. We have excluded REITs from this analysis because the accounting standards that they generally use are not comparable with the EBITDA metrics of other companies in the portfolio/wider index. Other EBITDA exclusions on the basis of data availability. All references to benchmarks are for comparative purposes only.

The importance of dividend growth to combat inflation

The importance of reliable dividend income growth cannot be overemphasised against this backdrop of inflation and market volatility when capital returns can be uncertain and depressed. We can report a positive outlook for dividend income. 2022 was a solid year for dividend growth and this should be reflected in the Fund’s final distribution, which will be declared at the end of this month. Most companies in your Fund have grown their dividends over the past year. Four held their payouts flat, and there was one notable and well-flagged cut – GSK. We fully support the latter, which reflects a sensible adjustment to capital allocation that frees up more cash for reinvestment.

While it is no secret that 2023 will bring challenges, we expect the Fund to continue growing the dividend. History shows that our companies can sustain their payouts through harsh conditions – datapoints from the Global Financial Crisis and COVID-19 pandemic support this.

In emphasising resilient dividend growth rather than chasing potentially riskier high yields, we aim for the yield on original investment for investors in the Fund to grow consistently. Assuming our companies continue to grow their cash flows and dividends at a reasonable rate, the dividend income that underpins the current 3.3% prospective dividend yield on an investment made today should increase long into the future and enable investors to protect and grow their wealth.

On behalf of the UK Income team here at Troy, may I wish readers a Happy New Year and all the best for 2023 and beyond.

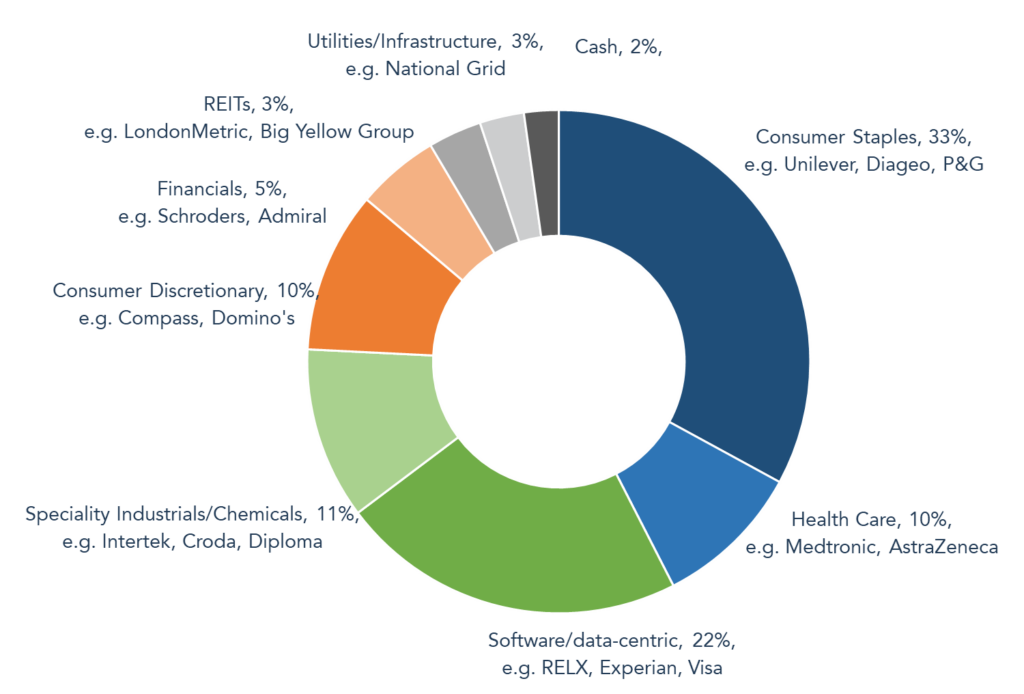

Your Fund’s major exposures as we see it

Source: Troy Asset Management Limited, 31 December 2022. Asset allocation and holdings subject to change.

We have written a summary below for readers to see how the portfolio is constructed.

Consumer Staples, 33%

This has long been the dominant sector in the Fund. We hold several of the world’s leading branded consumer staples companies, including Diageo, P&G, and Unilever. These highly resilient and cash-generative companies provide exposure to a broad range of exciting categories, including premium spirits, food, consumer healthcare and beauty products. We have been impressed by the global staples giants who have demonstrated their brand and pricing power well so far in the face of extraordinary inflation.

Health Care, 10%

We hold three global healthcare companies: the world-leading pharmaceuticals AstraZeneca, GSK and the US medical technology business, Medtronic. We like healthcare for its a-cyclicality, cash-generative economics, and secular growth drivers.

Software, platforms or data-centric business models, 22%

Software can be a fast-paced and disruptive space, but we focus on firmly established, dividend-paying stocks with sticky customer relationships reinforced by incumbency or proprietary data. To provide some examples of core holdings: Experian is one of the world’s largest credit bureaus, with origins dating back almost two centuries, and a linchpin of the credit system. RELX develops software tools for numerous industries, boasting nearly 80% of the Fortune 500 as customers. CME Group is the world’s largest derivatives exchange, owning the five most liquid futures contracts globally, including those for trading the US 10-Year Treasury Note and S&P 500. This gives CME a considerable incumbent advantage. All these companies are capital-light, highly cash-generative, and have been excellent sources of resilient dividends.

Speciality Industrial, Chemical and Distribution companies, 11%

Whilst the UK economy is no longer as exposed to heavy industrial manufacturing as in the past, the UK stock market is still home to some fantastic specialist industrial businesses. For instance, Croda provides speciality chemicals to consumers, beauty, and healthcare companies. We also invest in niche distribution businesses such as Diploma and Bunzl. Both have enviable track records of high-quality returns over multiple decades in the unglamorous sphere of B2B (business to business) distribution. Bunzl supplies numerous non-consumable necessities that businesses use daily, such as cleaning or packaging products. Bunzl’s robust free cash flow growth has enabled 30 years and counting of uninterrupted dividend growth.

Consumer Discretionary, 10%

We hold four companies here. InterContinental Hotels Group and Domino’s Pizza (UK) are leading brand owners benefiting from asset-light franchise business models and therefore strong dividend-payers. We wrote in detail in our October newsletter about longstanding holding Compass Group, the world’s largest contract caterer. We also own Next plc, which stands to gain substantial market share in a challenging retail market as it continues to evolve into a platform for third-party brands while generating high levels of cash and dividends.

Financials, 5%

We avoid many parts of this sector, including banks and life insurance companies, where we see sustainable growth and returns more challenged. Instead, we hold financials such as the wealth management company St James’s Place and UK auto insurer Admiral. For good reason, they are household names in the UK – both dominate niche markets and enjoy superior performance and scale over peers. Neither has been immune to the pressures in 2022, but both have fared better than competitors and have exceptional growth track records. We are excited about their prospective returns from here, with both companies trading with more than a 4.5% dividend yield.

REITs, Utilities/Infrastructure, 6%

These are more asset-intensive businesses that own property or infrastructure and pay attractive dividend yields. Our REIT (Real Estate Investment Trusts) holdings, including LondonMetric and self-storage company Big Yellow, have detracted amidst rising interest rates this year. However, we remain confident in the quality of their assets and like their stable dividend streams.

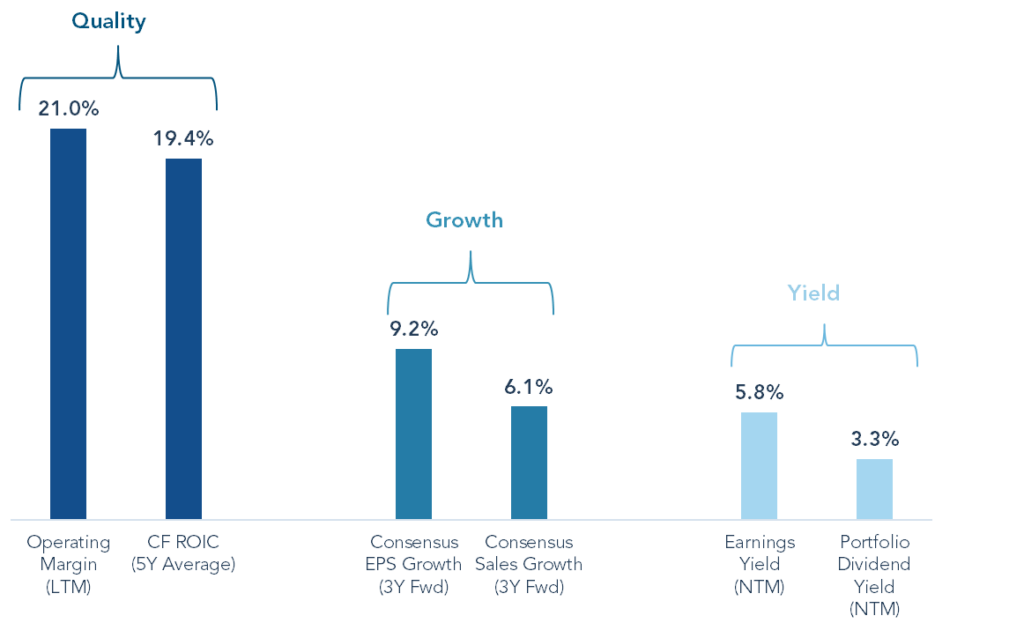

Overall, the Fund represents a diverse portfolio of companies with a clear emphasis on high-quality, cash-generative businesses capable of resilient dividend growth. The chart below illustrates the portfolio’s quality, growth, and valuation profile. Operating profit margins and returns on invested capital for the aggregate portfolio are both very attractive at c.20% – comfortably more than the FTSE All-Share (TR) Index. We expect healthy sales and earnings growth for the portfolio in the mid to high single-digit range over the next three years. And finally, this is coupled with a forward portfolio dividend yield of over 3%, supported by an earnings yield of nearly 6%. In my view, this combination of an attractive starting yield and consistent growth should underpin a strong range for returns for current and prospective investors.

Source: Factset and FTSE, 31 December 2022. Please refer to Troy’s glossary of terms. Last twelve months/next twelve months (LTM/NTM). Cash Flow Return on Invested Capital (CF ROIC) is a measure of financial performance that calculates how efficiently a company’s management is utilising all forms of capital available. Earning per share (EPS).

1Free cash flow is the cash a company generates after taking into consideration cash outflows that support its operations.

2A financial valuation ratio that divides the free cash flow a company earns against its market value.

3is a calculation of the profit or potential profit from an investment that takes into account the degree of risk that must be accepted in order to achieve it.

4Earnings before interest, taxes, depreciation, and amortization

Important Information

Please refer to Troy’s Glossary of Investment terms here. Fund performance data provided is calculated net of fees unless stated otherwise. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. Investments in mid and smaller cap companies are higher risk than investments in larger companies. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the fund’s price, as at the date shown. The yield is not guaranteed and will fluctuate. It does not include any preliminary charge and investors may be subject to tax on their distributions.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Derivatives (whose value is linked to that of another investment, e.g company shares, currencies) may be used to manage the risk profile of the fund.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. The fund(s) is/are registered for distribution to the public in the UK only. The fund(s) is/are available to professional investors only in Ireland.

The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents or, as the case may be, the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

The offer or invitation to subscribe for or purchase shares in Singapore is an exempt offer made only: (i) to “institutional investors” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “SFA”); (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

All reference to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2023. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence. Morningstar logo (© 2023 Morningstar, Inc. All rights reserved.) contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. The fund described in this document is neither available nor offered in the USA or to U.S. Persons.

Copyright Troy Asset Management Ltd 2023.