Prioritising sustainable dividend growth over high yield

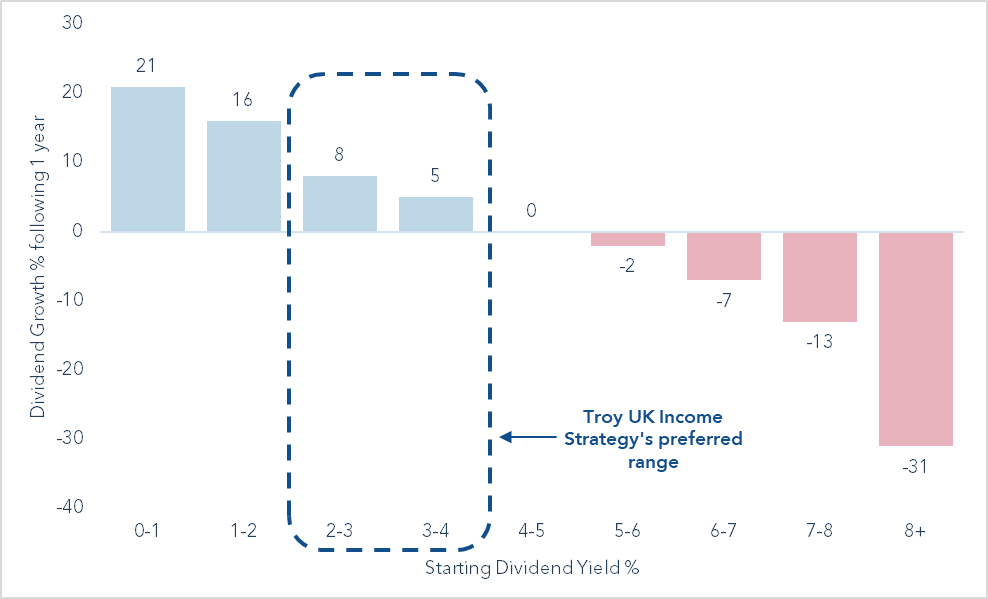

A key pillar to the quality approach to equity income we follow at Troy is an emphasis on sustainable dividend growth, rather than high yield. The case for such an approach is powerfully illustrated by the chart below. It demonstrates that the higher the yield, the lower the subsequent dividend growth and vice versa. Notably, the chart also implies that on average, dividend yields between 4-5% do not grow, and, worse still, that companies with dividend yields above 5% tend to cut their dividends the following year.

Figure 1 – Dividend Yield vs Growth the following year (FTSE All-Share constituents)

Past performance is not a guide to future performance and income generated (if any) may fall as well as rise.

Source: Factset, 31 December 2009 to 31 December 2022. Based on the historical constituents of the FTSE All Share Index ex Investment Trusts, groups aggregated using the mean. Outliers removed (+/-2 standard deviations) Income generated (if any) may fall as well as rise. All references to benchmarks are for comparative purposes only.

UK investors have suffered several high-profile dividend cuts in recent times where optically high dividend yields have ultimately proven unsustainable; banking stocks in the Global Financial Crisis, oil majors heading into the pandemic and most recently housebuilding stocks in a higher interest rate environment. A dividend cut is not only painful for the income account, it is almost always accompanied by weak share price performance. I have always believed that dividend growth, as a reflection of underlying free cash flow growth, is the ultimate long-term driver of equity returns, and am therefore very wary of reaching for high yield.

Income investors should also be wary of the far-left hand side of this chart at times when low dividend yields are reflective of high valuations. Dividend growth of 20% is appealing, but stocks with such low yields can come with material valuation risk and high share price volatility.

We seek sustainable dividend growth from quality, resilient companies trading at reasonable valuations. We like companies that pay out a sensible proportion of their profits as dividends, retaining a healthy portion to reinvest in further growth. Generally, we have found the right balance tends to be in and around the 2-4% dividend yield bands. If companies in this range are paying out roughly half of their earnings as dividends, it means that on average their shares will trade on 4-8% earnings yields1 . These are valuations that I deem attractive for resilient, growing companies. The portfolio today has a forward dividend2 yield of c.3.2% and an earnings yield of c.6.0%. If the chart is anything to go by, investors can reasonably expect mid-single digit dividend growth from the Fund over time, equating to a doubling of income every 10 to 15 years or so. This also concurs with our bottom-up forecasts for individual stocks. Importantly, we also aim to provide a stable income stream that does not suffer the same volatility across economic cycles as that seen historically in the wider market.

Dividend growth opportunities

As discussed in previous newsletters, we believe the UK market in particular offers compelling value today. There is an increasingly rich opportunity set emerging for UK dividend growth investors. Many high-quality companies in our internal investment universe currently sit within our favoured 2-4% dividend yield band. Below I pick out three held in the Fund today.

| IHG | Smiths | Unilever | |

|---|---|---|---|

| Earnings yield | 5.3% | 6.5% | 6.0% |

| Dividend yield | 2.4% | 2.8% | 4.0% |

| Latest dividend growth | 10% | 5% | 2% |

| Payout Ratio | 45% | 45% | 66% |

Past performance is not a guide to future performance and income generated (if any) may fall as well as rise.

Source: Bloomberg, 30 September 2023. The latest dividend growth refers to the most recent dividend declared by each company. The payout ratio is the proportion of earnings paid out as dividends to shareholders.

At the lower end of this 2-4% range is Intercontinental Hotels Group (IHG), owner of leading hotel brands including Holiday Inn, Crown Plaza and The Intercontinental. Whilst 6,000 physical hotels sit within their system, only six of these properties are owned by IHG, with the majority operating under franchise agreements. The beauty of this franchise approach is that IHG enjoys a largely capital-free growth model. Third-party operators take on the risk and cost of opening hotels, paying IHG a royalty for the use of one of their brands. This has enabled IHG to grow in a highly efficient way and to generate prodigious cash flow as their hotel network expands globally. The industry is currently enjoying good demand from both leisure and corporate customers. Strong profit growth for IHG is translating to good dividend growth for shareholders – IHG’s most recent dividend pay-out grew 10%. The current dividend yield is c.2.4% and the earnings yield is c.5.3% both of which are lower than the portfolio average, but this is reflective of the growth potential on offer. Less than half of IHG’s profits are paid out as dividends, leaving an ample portion to reinvest in this growth opportunity.

An example of a company in the middle of the 2-4% dividend yield range is industrial conglomerate Smiths Group, a new holding for the Fund in 2023. Smiths is a high-quality engineering business with an over 100-year history on the London Stock Exchange. Today it is a multinational, diversified company, with world-leading positions in several

end market niches ranging from oil & gas to construction and aerospace. Given the breadth of the business and the fact that c.70% of profits are earned from relatively predictable service and aftermarket sales, Smiths is less exposed to the economic cycle than many typical industrial companies. Smiths recently reported a healthy 5% dividend growth rate for their 2022/23 financial year and guided to similar growth going forward. Smiths has a c.2.8% dividend yield and c.6.5% earnings yield, which is attractive to us, especially given the high return on capital historically earned by the business, the strong balance sheet and the potential for mid-single digit growth into the medium term.

At the top end of this 2-4% range, where growth is likely to be slower, but dividend yields are higher, investors can find certain consumer staples companies including food and personal care giant Unilever. The company own some of the most recognisable brands in the world including Dove, Hellmann’s and Ben & Jerry’s. Unilever is a truly global business and over time has had the ability to expand even further into emerging markets and into adjacent product categories. With a new CEO and sensible refreshed strategy, we expect dividend growth to re-accelerate from the most recent c.2.0% level towards the mid-single digit range. The current dividend yield is c.4.0% and the earnings yield c.6.0%, both highly reasonable for such a high-quality, resilient business.

IHG, Smiths and Unilever are three examples of large, high-quality, cash generative companies within the portfolio that have a good balance between dividend yield and growth. Pleasingly for us as stock-pickers, we are finding multiple other such opportunities across the UK market today.

Bonds are an alternative once more, but it’s equities for the long run

We believe that an emphasis on dividend growth, rather than high yield, is particularly important at this current point in time. Such was the lack of yield available from government bonds in the years post the global financial crisis, that investors were consistently sold the ‘TINA’ adage – “there is no alternative” to equities. But higher inflation has meant that investors can once again get a risk-free yield from government bonds of c.5%. Some investors are understandably rebalancing their asset allocations between bonds and equities as a result.

Crucially however, what equities can offer over fixed income is a perpetually growing yield on original investment. Bonds on the other hand provide a fixed yield for the term of the bond, and potential reinvestment risk at maturity. Growth of earnings and dividends will always be the big advantage of equities over bonds and is the investor’s primary defence against the corrosive effects of inflation. As the chart above shows us, key to enjoying the benefits of dividend growth is finding the right balance between yield and growth. This means in most cases avoiding the highest yielding areas of the market. With inflation still high, and with yield available from fixed income, it is our belief that investors should prioritise dividend growth, not high yield, from their UK equity allocations.

1Earnings yield is the inverse of the Price to Earnings ratio, therefore is defined as Earnings per share/Share price. Please see Troy’s Glossary of Terms.

2Forward dividend yield refers to the projection of a company’s yearly dividend.

Please refer to Troy’s Glossary of Investment terms here. Fund performance data provided is calculated net of fees with income reinvested unless stated otherwise. All performance and income data is in relation to the stated share class, performance of other share classes may differ. Past performance is not a guide to future performance. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the fund’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. Any reference to benchmarks are for comparative purposes only. Tax legislation and the levels of relief from taxation can change at any time. Any change in the tax status of a Fund or in tax legislation could affect the value of the investments held by the Fund or its ability to provide returns to its investors. The tax treatment of an investment, and any dividends received, will depend on the individual circumstances of the investor and may be subject to change in the future. The yield is not guaranteed and will fluctuate. Any objective will be treated as a target only and should not be considered as an assurance or guarantee of performance of the Fund or any part of it. The fund may use currency forward derivatives for the purpose of efficient portfolio management.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The sub-funds are registered for distribution to professional investors only in Ireland.

The distribution of certain share classes of the sub-funds of Trojan Investment Funds (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents or, as the case may be, the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

Certain sub-funds are registered in Singapore and the offer or invitation to subscribe for or purchase Shares in Singapore is an exempt offer made only: (i) to “”institutional investors”” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “”SFA””); (ii) to “”relevant persons”” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA. “

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2023. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence. Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2023.