Why we are sticking with quality as earnings come under pressure

In recent weeks, I am sure that investors have once again been reflecting on how best to navigate markets. In today’s challenging investment environment, we are prioritising companies with resilient cashflows trading at reasonable valuations more than ever.

The Trojan Income Fund seeks to deliver investors a defensive total return by striking a sensible balance between capital and income growth. We do this by investing for the long-term in what we see as high-quality companies capable of growing dividends consistently.

Readers will have seen the market falling this year, primarily because of falling valuations rather than as a result of earnings weakness. Inflation and interest rate expectations have moved staggeringly fast over the past 12 months. This time last year, interest rates were expected to stay low, but as inflation has spiked, interest rates have risen, and equity valuations have fallen.

Interest rate-driven market falls tend to happen fast; once central banks are expected to raise base rates, the rate at which future equity cash flows are discounted rapidly follows suit. Other things being equal, discounting back prospective cash flows at a higher rate results in a lower company value and thus share price. Whilst this first order impact of higher rates on valuations happens almost automatically, the effect on the economy and corporate earnings is more complex, and tends to hit consumers and company profits after a lag. We believe it is to this that share prices are now most vulnerable.

Are we there yet?

Company earnings have remained broadly resilient year to date, but it seems inevitable to us that there will be a wave of profit warnings over the next 12 months. Companies will be battling slowing growth, rising costs and significantly higher interest payments against a shaky geopolitical environment and myriad inflationary pressures, particularly if energy prices remain high and interest rates continue to climb.

At Troy, we try to invest in high-quality businesses, with low levels of cyclicality , that we intend to hold for many years – possibly even decades. Equally importantly, we strive to avoid companies whose profits and cash flows might be volatile. This enables us to have a long-term perspective and remain patient equity investors, as we know that if we stick to quality, earnings, dividends, and value will compound. We can recover from short-term market declines through the steady accumulation of earnings and dividends.

In times of inflation or other economic stress, conventional thinking is that very profitable businesses with high margins will be less affected by rising costs than those with low margins. This is a sensible rule of thumb, and one we observe ourselves; holdings within the Trojan Income Fund in aggregate generate operating profit margins of over 20%, nearly twice that of the wider UK market (i.e. the FTSE All Share Index). There is however, room for selective nuance; some low-margin companies are able to consistently generate stable returns as a result of their highly defensive business models and powerful market positions. A good example of this is Compass Group, the world-leading outsourced catering company and a top-ten holding across Troy’s UK Equity Income Strategy.

The benefits of diversification and scale – Compass Group

The chances are you will have eaten (and hopefully enjoyed) a Compass meal. The company can trace its origins back over 80 years, and as market leader, serves 5.5 billion meals a year for 55,000 clients – including Google and The Wimbledon Tennis Championships, in 45 countries. Although a British company, the US is its largest, fastest growing and most important market, accounting for over 62% of sales, and even more of profits. Indeed, Compass is one of several holdings in the Trojan Income Fund such as Diageo, RELX, Experian, Bunzl which enjoys a large and growing US franchise. The USA has been a rich land of opportunity for all these businesses – as a vast, single country with a strong economy, it has proven more amenable for growth than, for example, navigating the borders and cultural differences from growing across Europe.

Compass’ historical performance is compelling. Even during the Global Financial Crisis, the company managed to grow sales and margins in the face of a severe recession, demonstrating its resilience. However, the global pandemic proved a unique and unusual challenge. As people were forced to work and study from home, sporting and leisure events were cancelled, and hospital services disrupted, Compass’ revenues temporarily dried up. This meant that 2020/21 was arguably Compass’ most challenging year; the company suspended its dividend and raised fresh equity in order to protect the long-term health of the business.

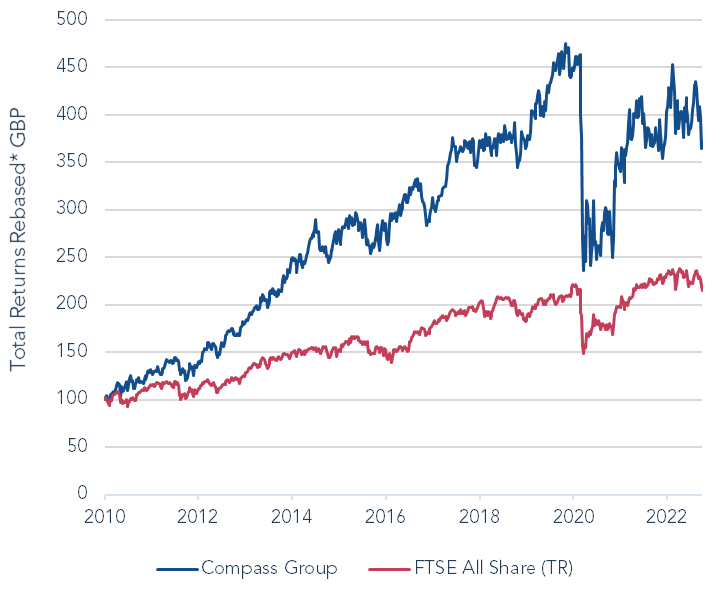

We consider a global pandemic an unusual case, and still view Compass’ defensive qualities favourably. Indeed, the company has since bounced back strongly, winning significant market share, and restoring revenues to above pre-Covid-19 pandemic, even though several countries are still grappling with its effects. 2020 was a difficult time for the company and investors, but as you can see in figure 1, the share price has largely recovered. For savvy investors, the turbulent period of the past 2 years offered the chance to buy what we believe to be a truly high-quality business at a compelling discount. As we look ahead to the looming risk of recession, Compass should be able to defend profits and further enhance its competitive position.

Figure 1: Total Return vs. the Index

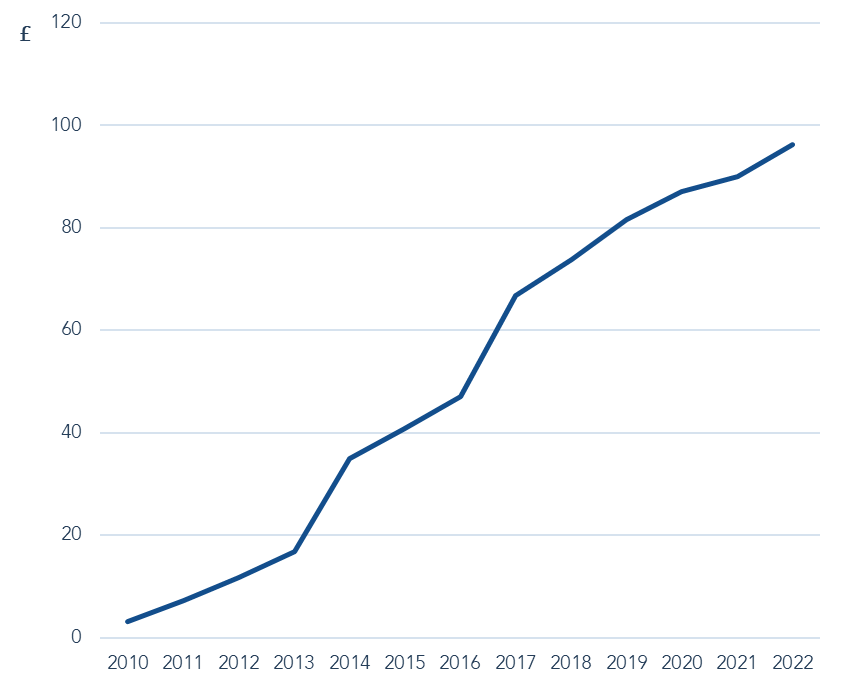

Like some other businesses we own, Compass has rarely traded on a particularly high dividend yield, and yet it has been a wonderful income stock when the total value of dividends to a long-term shareholder are considered. Figure 2 highlights aggregate dividends received from Compass since 2010 (the year in which the Trojan Income Fund first purchased shares in the business). For £100 invested in January of that year, an investor has received £96 back in income alone. Today’s dividend represents a 9% yield on our initial purchase price.

Figure 2: Aggregate Dividends on cost of £100

With share price volatility likely to remain a feature of the coming months, we think Compass’ regular, stable, growing stream of dividends is all the more valuable to investors reliant on investment income to cover their expenses. From a total return perspective, buy and hold investors have received a 14.3% compound annual return from the company since January 2010, comfortably surpassing the FTSE All-Share Index’s return.

At first glance, it may seem surprising that a company in the unglamorous world of catering is capable of such a strong performance. What is so special about this business? I would highlight three things.

Significant scale – Scale is a frequently cited source of competitive advantage for large companies. However, its importance should not be underestimated; in today’s challenging environment, there is enhanced value in global scale and geographic diversification. Compass enjoys both.

The scale at which food is purchased is crucial in the catering industry, where relative buying power is critical in a price-competitive, low-margin industry. Compass has a real advantage in supply chain management, particularly in the all-important US market, with its Foodbuy brand, through which it procures raw food for its own operations as well as for third parties. While the economics it earns from supplying to third parties are not significant, the unrivalled buying power this creates means the company is able to provide the most cost-effective catering solutions to its customers. This business model also means Compass can operate with significant negative working capital (i.e. its current liabilities exceed its current assets), allowing it to earn very attractive returns on its invested capital (>20%) despite having modest operating margins (7-8%). The result is that Compass’ superior scale becomes self-reinforcing – generating more profit than peers, and more firepower to win market share and further consolidate the industry. We love businesses that are fundamentally difficult to compete against, and Compass is undoubtedly one of them.

Decentralised business – Compass has several local and sector-specific business to business brands, enabling it to target more than 30 subsectors, ranging from high-end catering at sporting events to remote, off-shore catering for oil companies. Its emphasis on local, customer-centric, decentralised leadership is core to the success of the business. This model is all the more powerful when these local, customer-facing businesses are plugged into the wider group’s global supply chain management.

High retention – Compass retains about 95% of existing customers – and in the first quarter of the year, it was even higher. By serving customers what they need and offering the best value for money, Compass suffers very low customer churn and stable revenue growth so it can focus on winning new business. For clients, catering is not usually a core activity. Given Compass’ expertise, it can run clients’ catering operations more efficiently than the client can in-house, or by going to a competitor.

Looking ahead

The current inflationary backdrop is certainly not an easy operating environment. Compass’s two largest costs are food and labour, the prices of which are rising significantly. However, as many contracts have an element of inflation protection built in, profits have something of a buffer, and Compass’s advantages of scale mean the perilous operating environment gives the company a relative advantage over its peers – historically, periods of industry stress have led to Compass gaining market share.

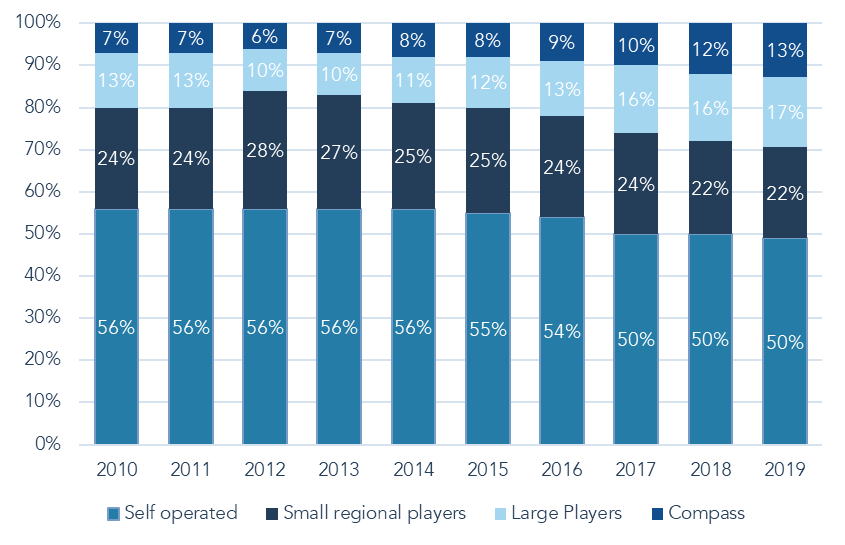

Taking a longer-term view, Compass has an attractive, significant market opportunity. As the chart below shows, the factors highlighted above have enabled the company to consistently increase its share of the market during the past 10-years.

Figure 3: Global Food Service Market 2010-2019

There remains abundant opportunity for further growth. The global catering market is very fragmented, with 70% of the market still either self-operated (as opposed to being outsourced to the likes of Compass) or in the hands of small regional players. Given that customers cite cost-saving as one of the key reasons for choosing to outsource their catering, we imagine there are material new opportunities for Compass in the coming inflationary years. We estimate Compass can provide clients with cost savings of around 20% compared with small regional peers – the choice seems clear!

High-quality dividend growth

Compass Group is typical of many of the high-quality, diversified, resilient businesses held by the Trojan Income Fund. Having topped up our shareholding at lower valuations on the back of disruption from the COVID-19 pandemic, the share price has recently risen to a more typical valuation level for a company of Compass’ quality; 21x earnings and a ~2.2% prospective dividend yield.

As Compass navigates challenging conditions, we believe it will fare far better than most. Should inflation expectations or turbulent markets create renewed share price volatility, this is a stock that should be near the top of any quality-orientated, dividend growth investor’s buy list.

As we live and invest through these uncertain and extraordinary financial times, we will keep you up to date with the opportunities and risks we discover. We wish our investors well for the remainder of 2022 and beyond.

Important Information

Please refer to Troy’s Glossary of Investment terms here. Fund performance data provided is calculated net of fees unless stated otherwise. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. Investments in mid and smaller cap companies are higher risk than investments in larger companies. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the fund’s price, as at the date shown. The yield is not guaranteed and will fluctuate. It does not include any preliminary charge and investors may be subject to tax on their distributions.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Derivatives (whose value is linked to that of another investment, e.g company shares, currencies) may be used to manage the risk profile of the fund.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. The fund(s) is/are registered for distribution to the public in the UK only. The fund(s) is/are available to professional investors only in Ireland.

The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents or, as the case may be, the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

The offer or invitation to subscribe for or purchase shares in Singapore is an exempt offer made only: (i) to “institutional investors” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “SFA”); (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

All reference to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2022. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence. Morningstar logo (© 2022 Morningstar, Inc. All rights reserved.) contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. The fund described in this document is neither available nor offered in the USA or to U.S. Persons.

Copyright Troy Asset Management Ltd 2022.