Currency – Last But Not Least

“The US dollar remains as important as when Bretton Woods collapsed”

Mark Carney at Jackson Hole, 2019

Currency markets can change quickly, but Carney highlights that the US dollar’s dominance is one element that has endured for decades.

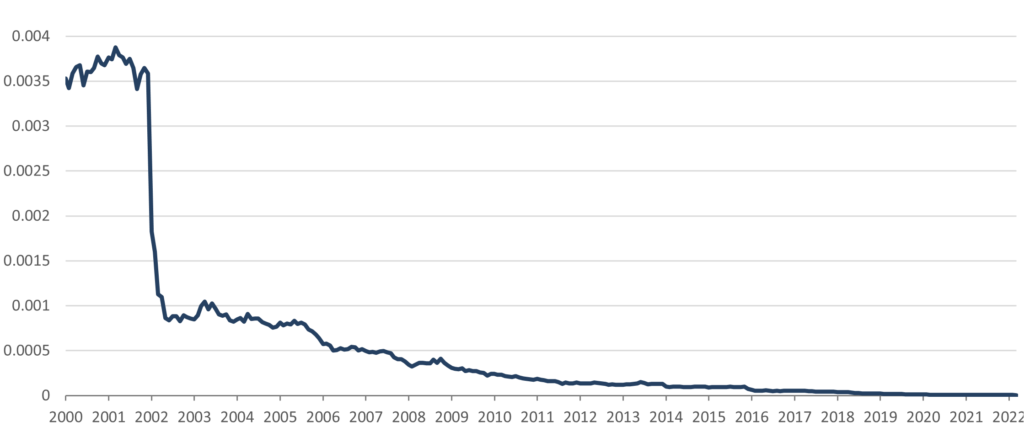

Currency analysis is often left out of discussions, perhaps as there is no consensus on the complex drivers of currency movements, but it can be immensely important when attempting to preserve capital in real terms – just ask the savers in Argentina, who have experienced first-hand the vicious erosion of their currency against recognised stores of value such as gold (Figure 1).

Figure 1: Value of the Argentinian peso against one ounce of gold

In our multi-asset mandates at Troy, investments are selected through ‘bottom-up’ analysis of the attractiveness of individual equities and fixed securities. The approach is different to a ‘top-down’ attitude, where securities are owned to gain exposure to a particular currency or macro driver. Currency risk is managed carefully and hedged when we feel it is appropriate. We are happy to be unhedged or fully hedged depending on market dynamics at the time. Currency exposure has made a significant positive contribution to the multi-asset mandates since the strategy’s inception and is responsible for 10% of historic returns[1], whilst also helping to protect capital during downturns.

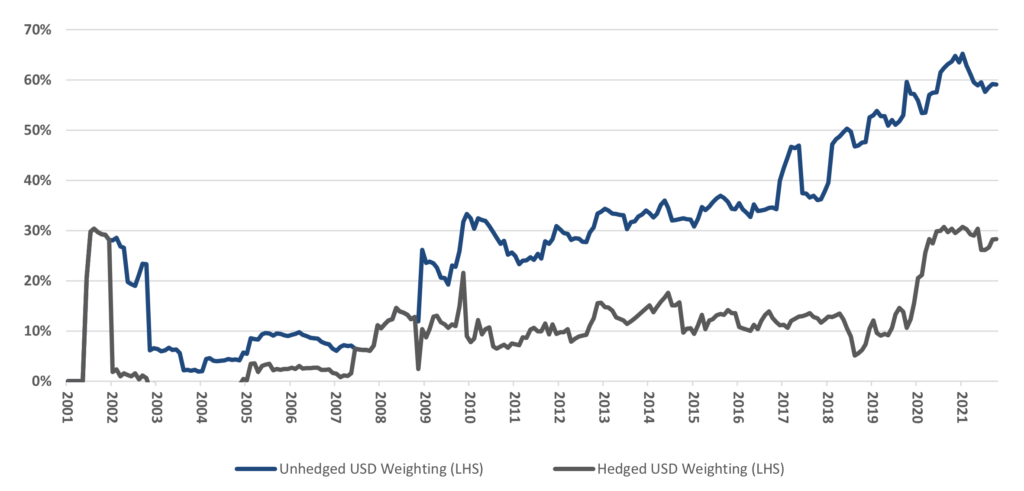

Over the last two decades the multi-asset funds have owned fewer sterling-denominated assets and more dollar assets. The transition has been driven by us continuing to find exceptional companies listed in the US and discovering better relative value in the large US inflation-linked bond market. The result has been that the strategy’s unhedged US dollar exposure has risen from 2% in mid-2004 to 59% at the end of March 2022 (with unhedged sterling exposure of 26%, gold being 12% and no other currency above 3%).

Many investors in Troy’s multi-asset funds have sterling-denominated liabilities, and performance in sterling terms is key. The primary non-sterling exposure in the Strategy is to cable (GBP/USD). To manage the currency risk, we hedge a significant portion of the dollar exposure back to sterling. At the end of March 2022, this reduced the unhedged dollar exposure of 59% to 28% net (Figure 2).

“The cemetery for seers has a huge section set aside for macro-forecasters”

Warren Buffett, 2004

Currencies are very different to equities and bonds, as there are no cash flows to value. There is no ‘price’ of a currency in isolation, so currencies are quoted relative to one another. Beauty is in the eye of the beholder, and unfortunately the holders tend to be fickle. The task of predicting currency returns, at least in the short term, is best left to others with much shorter time horizons. In the world of currency analysis, several analysts point to current account deficits as an indicator that a currency will weaken. However, the US has run a current account deficit since the early 1990s yet the dollar has held up well over the period, suggesting current accounts may be less predictive for the US.

Figure 2: Troy Multi-Asset Strategy unhedged and hedged US dollar exposure

Purchasing power parity (PPP), the idea that things should cost a similar amount in different countries, also appears to have little predictive power. For example, The Economist’s Big Mac Index is a light-hearted PPP tool that compares the cost of the McDonald’s classic in countries around the world. The Swiss franc is a currency that has consistently appeared ‘overvalued’ on PPP metrics for decades, yet it has strengthened against most other currencies, including sterling over the same time frame. The Economist’s tool also suggests that, as of early April 2022, the Russian rouble and Turkish lira are the most undervalued currencies relative to the dollar. (It is safe to assume that we will not be swapping our dollars for lira).

The safe haven

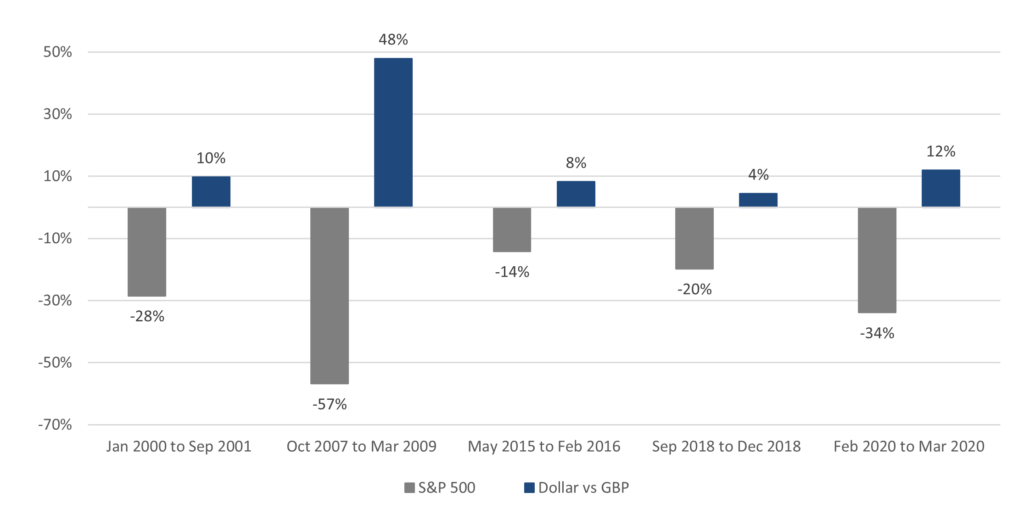

Much easier to predict is the dollar’s strength at times of market stress. During crises investors want to hold a low-risk currency they can trust. Many investors also follow carry-trade strategies, where money is borrowed in a low interest rate currency such as the US dollar and invested in a higher interest rate currency. These carry trades are typically unwound during market downturns, resulting in significant forced dollar purchases as cash ‘returns home’. In response to this combination of forced buying as well as ‘safe haven’ flows, the dollar typically appreciates against most other currencies, including sterling, offering a valuable offset (Figure 3).

Figure 3: S&P 500 performance vs USD/GBP during

The dollar is therefore both a risk to be managed, and a tool for managing risk. The ‘safe haven’ status of the dollar is increasingly useful today, given rising correlations between equities and bonds. The multi-asset funds’ dollar exposure, although reduced through currency hedging, has helped during periods of drawdown. As an example, during the market sell-off at the start of the Covid pandemic, the Strategy’s return would have been -1.8% lower had the dollar exposure been fully hedged[1]. Similar benefits are visible during the recent Ukraine crisis where the Strategy’s return would have been -0.9% lower with no dollar exposure, or Brexit[2] where returns would have been -1.1% lower.

Some level of dollar exposure is therefore useful. However, the approach to selecting the level of dollar risk to be hedged has evolved over time. Our focus is on having enough exposure to allow for the positive offsetting effects to be felt by the Strategy’s, without taking excessive risk.

Dollar dominance to persist?

In 1900, sterling dominated global finance and made up 64% of global foreign currency reserves, with most of the rest being French francs and German marks. Keynes described in 1930 how the Bank of England serves as “conductor of the international orchestra”. The dollar steadily grew in importance under the Bretton Woods System, where the dollar was pegged to gold and other currencies to the dollar. Growth in dollar use attracted the ire of many, with French Minister of Finance, Giscard d’Estaing, referring to its “privilège exorbitant” in the 1960s. The US Treasury Secretary’s 1971 comments to G10 ministers that “The dollar is our currency, but it is your problem” is unlikely to have helped sentiment in Paris. Today’s world is very different to 1900, with sterling only representing 5% of foreign currency reserves and the dollar occupying a similar level of dominance today as sterling did over 120 years ago.

A frequently cited argument against the dollar’s continued supremacy is the risk that it loses its status as the world’s reserve currency. The argument is receiving particular attention lately because the dollar has become a weapon in sanctioning Russia. The West’s ability to remove Russia’s access to the majority of Russia’s own $469bn of foreign currency reserves has surprised many experts. The scale of dollar hegemony today should not be understated. Although foreign currency reserves only represent one element of the dollar’s dominance, the dollar also reigns in commercial trade contracts. In Asian emerging markets roughly ¾ of exports are denominated in dollars and in South America the number is closer to 100%. Similarly, four out of every five cross-border interbank SWIFT transactions have a dollar leg. The greenback is even dominant in pricing commodities, with everything from oil to copper quoted in dollars. The world is reliant on the dollar and that incumbency is difficult to change.

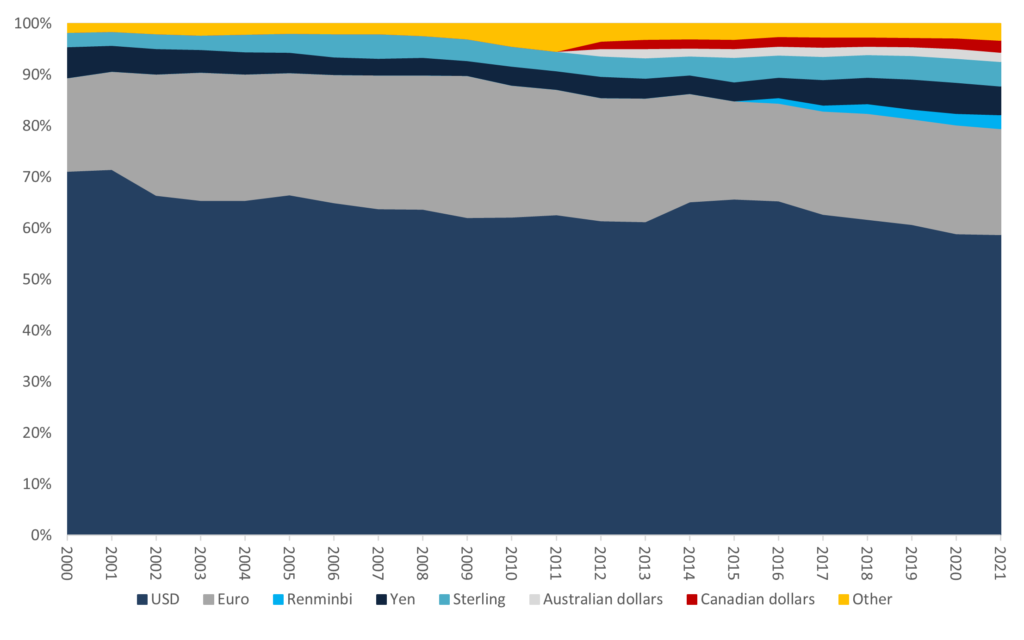

Figure 4: Global foreign exchange reserves by currency

Several commentators point to China’s renminbi as a threat to dollar dominance, due to the ever-increasing size of China’s economy and influence. This argument fails to recognise the characteristics that make the dollar attractive. The size of the US economy is only one element; reserve currencies are typically freely floating, issued by countries with open economies, broadly accepted political systems and predictable legal frameworks[1]. The renminbi offers none of these.

Where some central banks have sought to diversify their foreign currency reserves away from the dollar, the renminbi has not found favour. Instead, some have moved small amounts to the Australian and Canadian dollar. In 2021 the renminbi made up no more than 3% of global foreign currency reserves, compared to 59% for the US dollar (Figure 4). The renminbi therefore appears unlikely to gain significant traction as a reserve currency without large changes to the political, legal and financial system in China.

Our view

Currency exposure can be a significant driver of volatility in returns, particularly in a world of increasingly unorthodox monetary and fiscal policies. Some currencies have also posed a headwind over sustained periods.

The dollar is likely to remain the dominant global currency for the foreseeable future, with few realistic alternatives. Its ‘safe haven’ status also offers valuable diversification to investors at times when few other assets offer positive returns. The notable exception is gold, which is also held in Troy’s multi-asset funds.

Our multi-asset strategy at Troy has dollar exposure which is driven by a bottom-up view on individual assets. The resulting currency risks are then carefully managed as appropriate. Other currencies, such as the euro and Swiss franc, represent a very small part of the portfolio today. It is likely that we will maintain a positive net dollar weighting, giving exposure to its useful diversifying properties during times of market stress. The dollar has proven itself within the portfolio over the last two decades and continues to aid in our endeavour to protect the precious capital of our investors.

Marc de Vos

April 2022

Disclaimer

All information in this document is correct as at 31 March 2022 unless stated otherwise. Please refer to Troy’s Glossary of Investment terms here. Fund performance data provided is calculated net of fees unless stated otherwise. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

Investors in Austria, Germany and Spain may obtain a copy of the prospectus of Trojan Funds (Ireland) (the “Fund”), relevant key investor information document(s), memorandum and articles of association and financial statements in English (with the exception of the KIIDs which are also available in German and Spanish) free of charge from www.fundinfo.com and/or the respective information agent. The Funds’ information agent In Germany is Zeidler Legal Services, Bettinastraße 48, 60325, Frankfurt, Germany. The Funds’ information agent in in Austria is Erste Bank, Graben 21, 1010 Wien, Österreich. This document may be made available only to professional investors in Germany, Austria or Spain and should not be passed to anyone in these countries other than a professional investor.

Investors in Switzerland can obtain a copy of the prospectus, the key investor information documents or, as the case may be, the key information documents for Switzerland, the memorandum and articles of association, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland. The latest share prices can be found on www.fundinfo.com.

The offering of Shares has not been and will not be notified to the Belgian Financial Services and Markets Authority (Autoriteit voor Financiële Diensten en Markten/Autorité des Services et Marchés Financiers). The Shares may be offered in Belgium only to a maximum of 149 investors or to investors investing a minimum of €250,000 or to professional or institutional investors, in reliance on Article 5 of the Belgian Law of 3 August 2012. This document may be distributed in Belgium only to such investors for their personal use and exclusively for the purposes of information. Accordingly, this document may neither be used for any other purpose nor passed on to any other person in Belgium.

The Fund is registered for distribution in Italy for professional investors only.

The offer or invitation to subscribe for or purchase shares in the Funds (the “Shares”) is an exempt offer made only: (i) to “institutional investors” (as defined in the SFA) pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified [(the “SFA”)]; (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764).

Copyright © Troy Asset Management Ltd 2022