“Over the short term, prices move in an almost unpredictable way but over the long term, since they rotate around fair value, their returns are far from random but are quite predictable, being determined by a combination of the stable long-term return on corporate net worth modified by the extent to which they are at any time away from fair value, as the pull back to that value over time will add to or subtract from that long-term return.”

Andrew Smithers, Wall Street Revalued

The End of the Beginning

After a poor year for returns from capital markets, virtually across the board, we offer some thoughts on how investors might proceed from here. While the above quote is hardly pithy it contains an important truth: that over long periods, expected returns are a function of starting value. Given where we are today in terms of valuation in equity markets, we believe returns are likely to be more constrained in the coming years than over the last few years. Income is likely to be a valuable and reliable part of that return for investors.

The capital markets landscape has changed radically in the last few months and means that the future is likely to be different to the recent, and not so recent, past.

2022 was highly unusual in one key respect, both equity and bond markets suffered substantial losses at the same time. This was worsened by a change in leadership within equities after the glorious run of the technology winners of the last decade came to an end. Both these facts are notable and give us a glimpse of what the coming decade may hold.

As ever during times of stress, it helps to put things in perspective. We have had an extraordinary period in markets and the economy whereby structurally low inflation, and the aftermath of the global financial crisis of 2008, allowed for incredibly supportive economic policy. This was initially focussed on monetary policy, as governments sought to support weak economies via low interest rates and quantitative easing and at the same time repair some of the damage to balance sheets done by the crisis. This constrained fiscal policy. It was followed by both radical monetary and fiscal policy during COVID as governments had to provide help more directly to the economy rather than via the financial system.

So, as Mervyn King so neatly summarised, COVID gave us too much money and lockdown too few goods1 ; the result was inflation but also a highly speculative period in markets which were driven to generationally high valuations.

These rich valuations collided with a less supportive policy backdrop and the horrors of Ukraine. As the focus of the authorities shifted from supporting economic growth to quelling inflation risk, assets suffered. So far, so obvious.

What we are left with is a darkening outlook but with equity markets still priced towards the upper end of their historic valuation range. This suggests that while asset prices have declined in response to rising interest rates, they have yet to fully reflect the declining earnings outlook which would normally be associated with a recessionary environment.

Expectations vs Reality

Of course, valuation alone tells you very little about what markets might do in the short term, but we believe they offer a pretty reliable framework for what longer term expected returns are likely to be. High valuations imply low returns. The fact that investors tend to be most optimistic when prospective returns are at their lowest (and vice versa), is an unfortunate aspect of human psychology and was demonstrated perfectly during the speculative fervour of early 2021.

Perhaps this exuberance should be no great surprise given the extremely favourable conditions under which investors have operated for some 14 years. Not least, for an extended period money has been essentially free. Even over short periods low interest rates encourage rash behaviour. When this condition holds for years, speculative creativity really takes flight. This culminated in a world of SPACS2 , meme stocks3 , crypto and “have fun staying poor4”. What is unusual about this occasion was the madness was such that it could be identified in real time, even if the timing of its conclusion was unknowable5.

Within boring old mainstream equity markets this manic updraft drove a material rerating which, when combined with strong earnings growth, in part driven by a strong economy (which itself also was benefitting from cheap money), created the lollapalooza of the recent past.

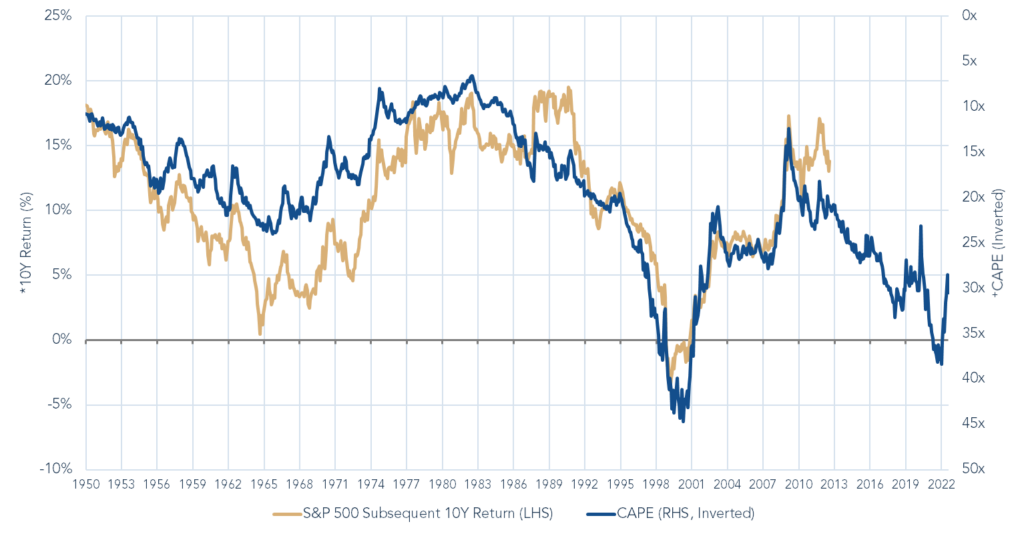

The following chart demonstrates the tight correlation of the starting long-term valuations and subsequent 10-year returns.

Source: BLS, S&P’s Shiller, NBER; Minack Advisors. July 2022. *Average nominal total return. +Cycle-adjusted Price to Earnings, inverted & leading by 10 years

Sorry to be the bearer of bad news but the next 10 years, in the absence of a material repricing of risk (in addition to that which we have already seen) returns are likely to be low. As such it may be wise, even now, for investors to take a different approach to equity investment.

As an income investor we have experienced, over many years, how our approach becomes more or less favoured at different points in the market cycle. Essentially, the better the recent historic returns the less in favour is our strategy. If investors are enjoying high year-on-year returns, the relative certainty of an income yield and its incremental contribution to return is swamped by the riches delivered by the market.

However, since over extended periods the underlying return delivered by the market tends to be fairly constant, a very strong period in markets must, by definition, be a function of not only returns on equity (or corporate net worth as Andrew Smithers says) but also the price investors are willing to pay for those returns. Strong returns are likely to have been driven in part by a re-rating of equity prices.

A Random Walk?

Equities, over very long periods, are not a random walk but demonstrate what should properly be called “negative serial correlation”7. What is expensive is likely to become cheaper and vice versa.

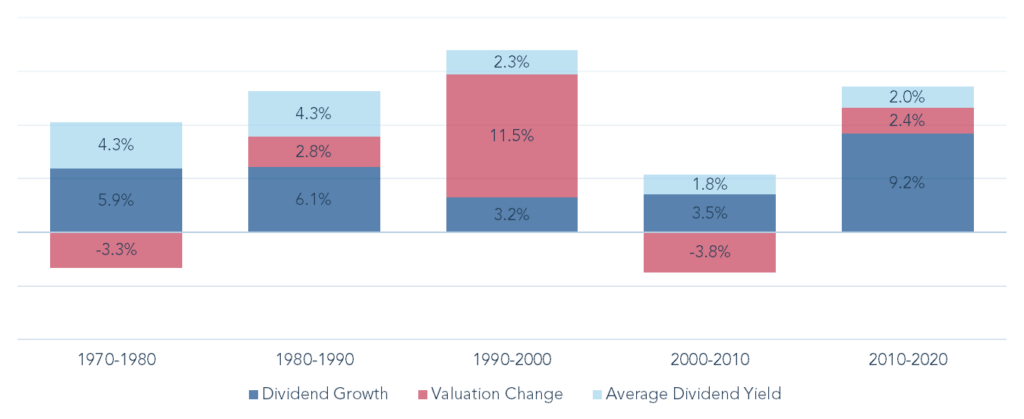

We demonstrate this phenomenon in the below chart showing returns over discrete decades in US equities (as an example).

It can clearly be seen that in times of plenty, returns are augmented by the re-rating of equities in addition to the strong underlying corporate performance. Further, in more lean times, the contribution from dividends and dividend growth becomes dominant. This effect can also be seen from the above data to have delivered in both times of inflation (1970-80) as well as following a speculative peak (2000-10). If, as we fear, investors suffer in the next 10 years, from both the aftermath of a similar speculative peak (this time driven by the COVID policy response rather than by the Y2K8 fears of 2000) and greater inflation, income may become more valuable still.

| US Equities | 1970-1980 | 1980-1990 | 1990-2000 | 2000-2010 | 1990-2000 |

| Dividend Growth | 5.9% | 6.1% | 3.2% | 3.5% | 9.2% |

| Valuation Change (Price/Dividend) | -3.3% | 2.8% | 11.5% | -3.8% | 2.4% |

| Average Dividend Yield | 4.3% | 4.3% | 2.3% | 1.8% | 2.0% |

| Total Return | 6.9% | 13.2% | 17.0% | 1.6% | 13.6% |

| Returns from Dividends and Dividend growth | 100% | 78% | 32% | 100% | 82% |

Source: Troy Asset Management Limited, Bloomberg/MSCI US Index, 31 December 2022. Income generated may fall as well as rise. All information above is calculated as annualised returns.

All Change

In our experience this change in return profile from decade to decade is echoed in markets. It is very unusual for the leaders of one decade to persist to the next. Not only do investors have a tendency to crowd into winners, driving up valuations and therefore diminishing future returns, but more fundamentally, over valuation attracts yet more capital which leads to over investment and ultimate lower underlying returns on capital.

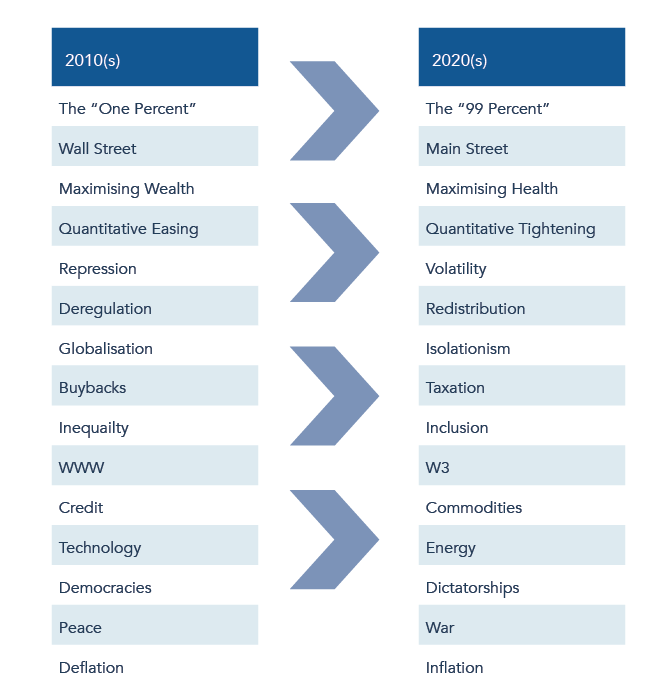

Once again, perhaps, this should not be too surprising. We have seen a period of returns accruing to a small number of companies which became extremely popular leading to an exhaustion of incremental buyers. Further we’ve seen a sea-change in the investment backdrop; in inflation, interest rates, geopolitics, regulation, industrial policy, energy security and many other areas. To us, a change in market leadership seems very likely. An example of this “all change” idea is laid out below by Michael Hartnett of Bank of America, but there are many such examples.

Source: Bank of America, 31 December 2022

To this we would add two comments. First, although much has changed, valuations remain rich thus we cannot add that assets yet offer attractive prospective returns. Second, we would add a further line which suggests that returns from 2010s were driven by capital growth, whereas from the 2020s they may be driven far more by income.

Where to from here?

Having made the case for the importance of income as a crucial part of returns in the coming years, the question now is how should one go about investing for income in this new world?

It is tempting to think that the profound change in the investment environment should lead to an equally radical change in investment approach. We do not think that such a change invalidates our focus on high-quality businesses that lack both capital intensity and cyclicality. It is certainly true that there are plenty of capital-heavy, often commodity related businesses that are cheap. They may very well perform over the coming months, but we do not think that investing in businesses that have low and volatile returns on capital is likely to be a winning proposition over the next 10 plus years which is the timescale over which Troy typically invests.

We will address this point in more detail in Income Matters No.5.

1https://www.cityam.com/central-banks-covid-qe-splurge-was-a-mistake-ex-boe-governor-king-says/

2Special purpose acquisition company.

3Meme stocks describe the shares of companies that have gained a cult-like following on social media, which can influence share prices.

4The rallying cry of Bitcoin enthusiasts. For context Bitcoin is now down c.75% from the peak.

5https://www.gmo.com/globalassets/articles/viewpoints/2022/gmo_let-the-wild-rumpus-begin_1-22.pdf

6Re-rating in the stock markets means that investors are willing to pay a higher price for shares, usually in anticipation of higher earnings in the future.

7For a more detailed discussion see Wall Street Revalued, Andrew Smithers, 2009

8Year 2000 problem

Disclaimer

Please refer to Troy’s Glossary of Investment terms here. Fund performance data is net of fees with income reinvested unless stated otherwise. All performance and income data is in relation to the stated share class, performance of other share classes may vary. Past performance is not a guide to future performance. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic dividend yield reflects distributions declared over the past twelve months as a percentage of the fund’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. The yield is not guaranteed and will fluctuate. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. For further information on Troy’s use of benchmarks, you should consult the Fund prospectus. Investments denominated in currencies other than the base currency of the Fund may be affected by movements in currency exchange rates.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the Fund may not be suitable for all investors. If you are in any doubt about whether the Fund is suitable for you, please contact a professional adviser.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Ratings from independent rating agencies should not be taken as a recommendation.

The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The Fund is available to professional investors only in Ireland. The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information document(s) (edition for Switzerland), the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

The offer or invitation to subscribe for or purchase shares in the Funds (the “Shares”) is an exempt offer made only: (i) to “institutional investors” (as defined in the SFA) pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “SFA”); (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. The fund described in this document is neither available nor offered in the USA or to U.S. Persons.

Copyright © Troy Asset Management Ltd 2023.