When life gives you lemons, make lemonade

2025 was not our year. Returns were materially below our objectives as global equity markets advanced. The extraordinary aspect of 2025 is that for the most part the Strategy’s companies maintained their excellent operating momentum, but this was not reflected in their share prices. This discrepancy sets the Strategy up well for the future, and accounts for our growing optimism.

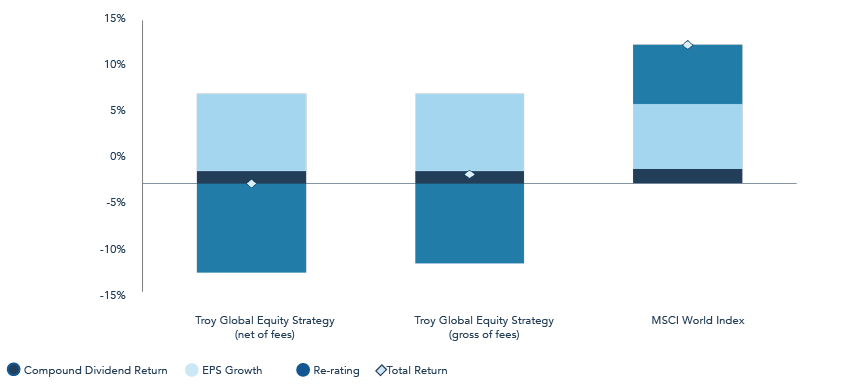

Figure 1: The Strategy has de-rated, despite superior earnings growth

Source: FactSet and Troy Asset Management Limited – net and gross of fees GBP, 31 December 2025. Past performance is not a guide to future performance and forecasts are not a reliable indicator of future performance. All references to benchmarks are for comparative purposes only. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Global Equity Strategy. Please refer to Troy’s Glossary of Investment Terms.

Nonetheless, we recognise that this year’s outcome requires unpicking. We see three reasons for the Strategy’s poor performance – animal spirits, AI, and our own mistakes. We’ll review each in turn.

Over a typical investment cycle, the Strategy tends to lag slightly in more buoyant markets and add most value when markets are more difficult. 2025 is unusual because we sampled both conditions. The Strategy added value when markets sold off sharply in March and April. Performance then lagged materially during the subsequent rally.

Figure 2: 2025 monthly returns

Source: FactSet, 31 December 2025. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Global Equity Strategy.

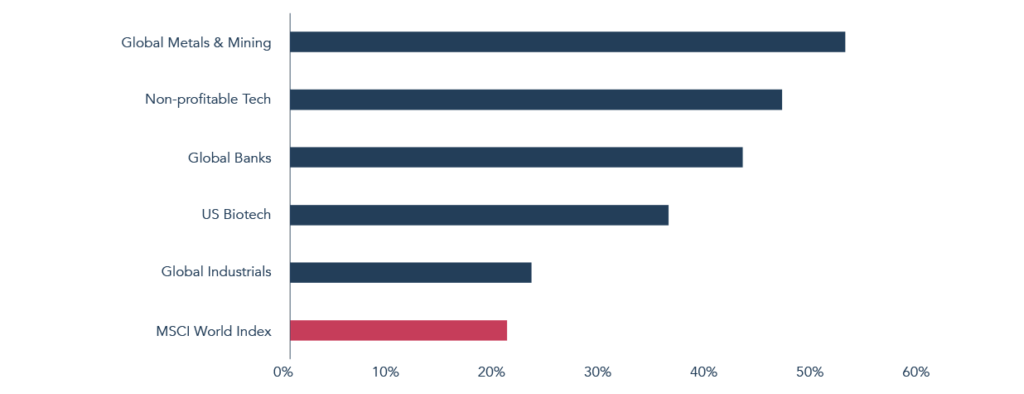

Periods of underperformance in rising markets are not uncommon over the history of the Strategy. These episodes usually coincide with markets that are led by those areas most sensitive to sudden upturns in investor sentiment – cyclical companies and ‘value’ stocks. This year banks, miners and industrials are among the best performing sectors. They do not form a part of the portfolio.[1] More speculative companies – those with weak finances and/or new technology – have also generated exceptional returns. For instance, unprofitable tech and biotech – inherently risky companies that we tend to avoid – have each recorded spectacular gains.

Figure 3: Big gains, over there: 2025 returns by sub-sector

Source: Bloomberg, 31 December 2025. Performance is in USD. Past performance is not a guide to future performance. All references to benchmarks are for comparative

purposes only.

At one level, therefore, the Strategy’s performance this year is consistent with historic patterns. What stands out in the data is the magnitude of the underperformance. The prominence of AI has contributed to this and hurt the Strategy’s performance in two ways – first, by benefitting the shares of semiconductor and data centre infrastructure companies, such as NVIDIA, in which the Strategy is not invested; and second, by calling into question the durability of several of the Strategy’s data and software companies.

The disruption from AI is more imagined than real at this point – earnings for the companies caught in the crosshairs are sound, and ahead of the market’s growth, but their valuations are lower. This is all the more pertinent when the year contains a +55% gain (in GBP) for Alphabet, the Strategy’s single biggest investment.[2] Alphabet’s transformation from ‘AI loser’ to ‘AI winner’ in the past six months is indicative of the equity market’s mood. We think that several other portfolio companies are also temporarily misjudged in the interminable debates about AI’s potential impact. This creates a significant opportunity, in our view, and underpins our optimism about the Strategy’s future returns.

Mea culpa: Fiserv and Diageo

The year was not without its errors. There are two in particular that stand out for being costly and imparting important lessons.

The greatest mistake is clearly Fiserv. Over more than a decade of ownership, our research suggested Fiserv’s 39-year record for annual double-digit compounded earnings growth was sustainable. This assumption was challenged abruptly by the company’s third quarter results. These revealed the company had underinvested and pursued sales tactics that were too aggressive, leading to a sudden reset in earnings and a change in management. This came as a shock and we immediately exited the investment. Fiserv was long known to be run harder than most in the portfolio, but our research found ongoing evidence for innovation and market share gains. We undertook significant additional work in the year to understand the trajectory of the business’s results, including a deep review of the company’s accounting standards. In retrospect we mistook red flags for orange ones, believing Fiserv’s shares to be unduly punished and deeply discounted because of a modest loss of operating momentum. We should have been more wary when signs of slipping execution coincided with the sudden departure of Fiserv’s charismatic CEO to serve in the US administration. The hard lesson from Fiserv is to make no exception in the avoidance of companies that are highly financially engineered.

In Diageo’s case we were wrong to expect revenues and earnings to be more resilient than they have proven to be. The consumption trends suggest that changing drinking habits are exerting more pressure on the company’s results than we originally thought. Diageo is a highly profitable business with a lot of embedded value; not only a unique collection of iconic brands, but an asset base heavily invested for a higher level of growth. Our continued ownership reflects a refreshed investment case centred on Diageo’s opportunity to simplify operations, focus investment, and improve returns on capital. The company’s valuation is depressed as we await the imminent arrival of Diageo’s new CEO, who comes with a track record for unlocking value.

AI Booming and Bubbling

We step into the AI debate with some trepidation because it is complex, polarising and fluid. It has absorbed a significant amount of our time and research effort this year. We find ourselves occupying the middle ground because we recognise the merits of both sides of the controversy. We will keep our comments here relatively brief since many of the views we shared 18 months ago continue to hold up.[3] We think we are still in the early stages of AI’s adoption, particularly for large enterprises, which are inherently slower moving. This buys some time for the incumbent companies that the Strategy favours to reinvest and adapt their offerings to incorporate generative AI (‘Gen AI’). This time cannot be wasted because AI-native new entrants are proliferating and the stakes are higher.

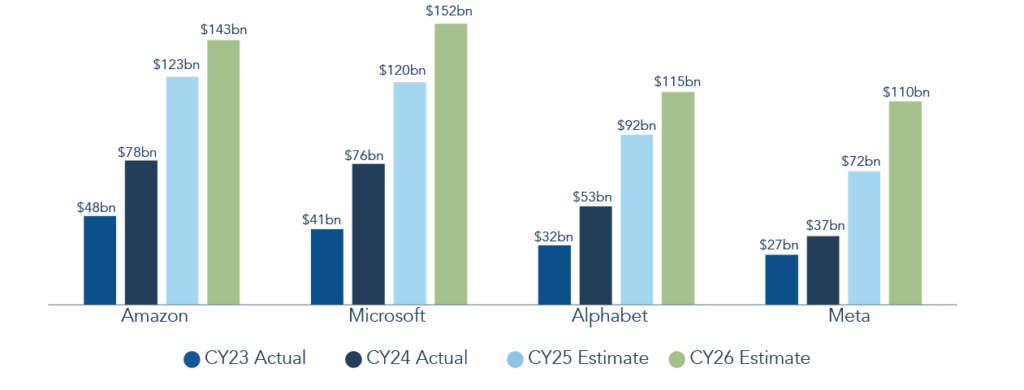

Figure 4: Growing Capex ($bn)

Source: Jefferies, 31 December 2025 . Past performance is not a guide to future performance. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

Capital expenditure (‘capex’) estimates for Alphabet, Meta Platforms and Microsoft for 2025 are over +50% above where they were 18 months ago. Capex is set to rise by substantial amounts again in 2026. This trend makes us nervous about prospective ROICs, yet it does not take place in isolation. So-called scaling laws underpinning the improvement of large language models (‘LLMs’) continue to hold. In simple terms, the models grow more capable with bigger training runs, requiring greater capex and unlocking higher economic potential. NVIDIA’s latest chips should propel further advancement at the frontier of model development. Moreover, AI demand is scaling rapidly and currently outstrips supply. This is visible in the contracted backlogs for Alphabet, Microsoft and Amazon that are growing substantially faster than their cloud service revenues. Despite their enormous scale, revenue growth has accelerated as capacity has come online. This is an important signal.

Figure 5: Accelerating growth across the board (revenue growth, YoY)

Source: Bloomberg, 31 December 2025. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

Accelerating revenue growth provides cover to invest aggressively. And whilst capital intensity is up a lot, AI is generating internal productivity savings that means they are scaling revenues without adding many more employees. This is a tailwind for profitability when ROIC is under pressure. It is also consistent with the lesson from investing in Microsoft over the past decade; rising capital intensity is not incompatible with attractive ROICs.

Figure 6: Revenue per employee

Figure 7: Microsoft’s ROIC and capital intensity

Source: Bloomberg, 31 December 2025. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

There are important differences to draw out between the companies that put them on different trajectories. To summarise:

- Microsoft is a trusted partner for corporate executives anxious to explore AI’s potential. Its relationship with OpenAI brings with it valuable IP (without the direct costs of model development), the opportunity to take market share, and risk management headaches.

- Now that its Gemini model is cutting edge, Alphabet’s unique vertical integration is coming to the fore across its various services.

- Amazon Web Services (‘AWS’) is behind in developing its own models and chips but it is quickly catching up thanks to its close relationship with Anthropic. Amazon has much to gain in applying Gen AI to its own retail operations.

- Meta faces elevated risks and rewards. Revenue acceleration is the steepest due to the power of AI to super-charge user engagement and ad targeting. Meta is also in a more precarious position without a cloud service business, leading custom chips, or (for now) a leading frontier model.

Outside of the cash-rich companies owned in the Strategy, we see growing fragility and excess. Sky-high private market valuations for deeply loss-making AI labs set unrealistic growth expectations. The market for model makers looks ripe for consolidation and indebted ‘Neoclouds’ (CoreWeave, Crusoe etc.) are vulnerable marginal providers of capacity.[4] Public and private markets are increasingly intertwined through equity ownership and contractual relationships. It is hard to imagine how the boom will continue without wrong turns and misallocated capital.

In this dynamic and uncertain situation, we are careful to manage our exposures. For instance, Alphabet remains a top holding, but whereas we were buyers of the shares in April, in recent months we have made material cuts to the investment. Opportunity costs have also motivated this shift. As these risks and valuations have evolved, other opportunities have emerged. Investments in Alphabet, Meta and Microsoft have been a source of funds for other ideas.

Data! Data! Data! I cannot make bricks without clay.

Sherlock Holmes

Experian’s shares were -1% in 2025 and LSEG’s were -20%.[5] They are therefore illustrative of companies that have held back the Strategy’s returns this year. Consistent with much of the rest of the portfolio, operating results remain solid. Both companies will almost certainly report double-digit growth in earnings for 2025, and the companies have met or exceeded investors’ expectations for the year. The challenges have not so much been financial but hypothetical – focussed on AI’s potential to change competitive dynamics in their industry. Company valuations have de-rated lower in this context. This trend is part of a broader theme engulfing the shares of data and information service providers. The great fear overhanging these stocks is that AI will make replicating software and datasets easier, thereby enabling a new breed of competitors.

Figure 8: Steady growth meets de-rating (NTM P/E ratios)

Source: Bloomberg. Note Experian has a March year end. LSEG has a December year end.

LSEG

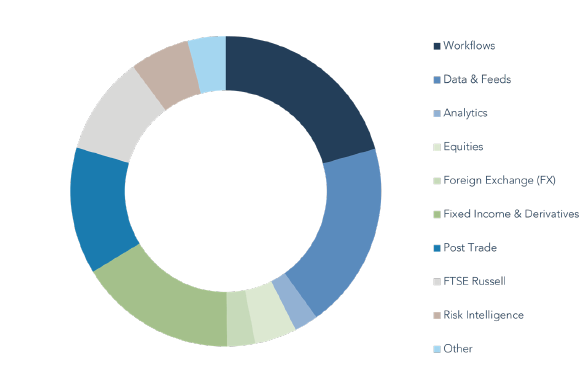

In LSEG’s world of financial data sold to bankers, new entrants are quickly emerging. Anthropic has released Claude for Financial Services, allowing its users to analyse investments using natural language prompts. At Troy, we use AlphaSense, a single chatbot capable of querying Troy’s own internal research, the third-party research to which Troy subscribes, and information freely available on the web. The emergence of these and other players raises the risk of disintermediation and displacement for LSEG’s own Workflows desktop products. It also supposedly endangers the Data & Feeds business it has supplying data to banks and other financial institutions. Together, the Data & Analytics division – largely comprising of Workflows and Data & Feeds – accounts for ~45% of LSEG’s group revenues.

Figure 9: LSEG’s revenue mix

Source: Bloomberg, 31 December 2025. 2025 Estimates.

The competitive risk posed by AI appears plausible on the surface but for LSEG we find it struggles to stand up to scrutiny. Data & Feeds faces minimal risk, in our view. ~45% of its revenues derive from real-time pricing. This data is gathered through LSEG’s own infrastructure from 575 exchanges and trading venues, processed and distributed in milliseconds to financial institutions and governments. The probabilistic qualities of Gen AI have little to offer here in a market defined by deterministic data, economies of scale and network effects. Another ~25% of Data & Feeds data is proprietary and exclusive to LSEG, inaccessible to an LLM without LSEG’s permission. This includes, for instance, M&A transaction data from thousands of public and private sources, further enhanced by LSEG’s data standards, curation and analytics. LSEG has ~33 petabytes of data in total, far more than the ~10 petabytes of web data over which LLMs are typically trained. LSEG usually sell this as part of a bundled set of services and the breadth of LSEG’s offering makes it a convenient and cost-effective one-stop-shop for financial data.

Figure 10: ~90% of Data & Feeds revenues is protected by proprietary data, technology or infrastructure

Source: LSEG

The Workflows business operates in a more competitive environment than Data & Feeds, but we believe it to be well insulated from Gen AI’s threat. Unlike peers such as Factset that primarily serve asset managers, 85% of Workflows revenues comes from traders and investment bankers. Their needs centre less on qualitative research for which LLMs can add value, and more on the exclusive data, tools and connectivity that LSEG provides to power users’ trading and commercial activity.

Figure 11: Workflows meets specific needs with specialist data and tools

Source: LSEG

LSEG’s products and services are trusted to complete high-value tasks, carrying small costs in relation to the activity they support – a financial transaction, analyses, or compliance etc. LSEG is deeply embedded into the policies, procedures and end-to-end workflows of large financial institutions. These are heavily regulated entities for which errors can carry substantial financial, legal and reputational costs. Customers have little incentive to experiment with incomplete substitutes, especially not those offered by new entrants with short track records for delivery and regulatory compliance. This makes LSEG’s Data & Analytics division sticky, recurring and defendable.

We believe misplaced fears about AI-related competition have led investors to overlook three important aspects of LSEG’s business. First, LSEG enjoys very broad diversification by product, asset class and geography. Data & Analytics is broad in its own right. The other 55% of LSEG’s business represents a unique collection of hard-to-replicate assets operating in consolidated markets with high barriers to entry. These businesses are structurally growing, highly profitable, and carry little to no risk from Gen AI.

Second, is the way that management has modernised the business. Workflows was a consistent market share donor when it was acquired as part of the 2021 merger with Refinitiv. Since then, its fortunes are revived through product innovation and sharper commercial execution. It was LSEG’s landmark partnership with Microsoft announced late in 2022 that renewed our interest in the company because it further signalled a commitment to reinvest.[6] LSEG has re-platformed its infrastructure in the cloud, making its data easier and faster for customers to access.[7] There are financial benefits to this too, as the heavier part of this reinvestment phase comes to an end, leading to improved profitability and cash flow.

Lastly, few investors are considering the upside for LSEG from AI as it drives deeper engagement, discoverability and new distribution arrangements. The growth of quantitative trading is leading to explosive demand for LSEG’s real-time data, and first-party LSEG LLMs and agents are coming to LSEG’s products to give users a more intuitive way to explore LSEG’s vast datasets. LSEG is expanding its reach to make its data available to more customers. As part of its Microsoft partnership, LSEG’s data and products are increasingly interoperable with the ubiquitous Microsoft 365 suite, including Excel, Teams and Copilot. LSEG has also struck new distribution agreements with third-party LLMs and cloud infrastructure providers. We see strong evidence for LSEG’s continued adaptation, setting the business up for durable growth.

Experian

These data sets are vast, complex, they’re constantly being refreshed, they are subject to expansive and stringent regulation, and they need to be accurate all of the time. The job of creating these data assets is a huge and complex operational exercise, which relies not just on process but also on proprietary intellectual property and significant industry expertise. They simply cannot be replicated and they cannot be accessed unless permissioned by us.

Brian Cassin, Experian CEO

Brian Cassin is a straight-talking Irishman with over a decade’s experience leading Experian. In recent months, he has responded robustly to worried questions about the replicability of the company’s datasets by AI. Experian’s data does not lie around on the open web. The data comes directly from thousands of financial institutions who appoint Experian (and only a small handful of other credit bureaux) to gather, process and aggregate individuals’ private credit information. This is a sensitive and regulated process that takes place at enormous scale. In North America alone, Experian ingests 1.1bn new data points on a monthly basis and combines them with historical data to understand credit trends and make precise predictions. This new information from thousands of sources does not all arrive in neat, standardised formats – a mammoth data cleansing and normalisation exercise is required to make sure the information is represented correctly and for the right individual. Every credit bureau’s dataset is unique and it evolves continually over time as new information is added. The data’s value rests in its depth, breadth and regulatory compliance, giving its users a complete and accurate picture of every consumer over their adult lives. Deep and proprietary understanding is then required to extract useful signals from it.

LLMs aggregating slices of publicly available information cannot offer much additional value. They are therefore likely to follow other purported threats to the credit bureaux that have popped up over the past decade; lending clubs, social media giants, BNPL providers and Open Banking. Despite various claims to the contrary, none have posed actual danger to the bureaux’s competitive standing. Language models with stochastic outputs are also at odds with determining identity and credit worthiness based on hard facts and complicated maths.

Beyond the regulated data there are behavioural and institutional realities. Experian’s clients use Experian’s data to form credit models upon which essential decisions are made – e.g. the extension of a loan, identity verification, a marketing offer. Experian increasingly delivers its data though cloud native analytics and decision-making software that further embeds its services into the fabric of its customers’ daily activities. Market shares do not easily move even among the large players, who co-exist according to historical strengths developed as the credit bureaux industry was established. The stickiness of customer relationships is underscored by the massive 2017 data breach in the US experienced by Equifax, Experian’s close rival. Despite the huge damage done to customer trust, Equifax lost no customers – a remarkable outcome and a reassuring stress test of the durability of this business model. We see repeated examples of the difficulty in unseating the incumbent bureaux – for example, over the past decade, deep-pocketed newer entrants in the UK and Brazil, Experian’s other two major markets, have failed to gain any meaningful traction.

Experian’s clients are less interested in finding new data providers and more interested in using the data from incumbents in new and creative ways. Far from being a risk to Experian’s business, we see AI as a tailwind. Experian is introducing language models to make its products easier to use. For instance, Experian’s AI Assistant enables credit analysts to use simple language queries to understand how their complex models might be amended or improved. Experian has also trained a small language model to automatically generate the required documentation detailing a credit model’s compliance with internal risk policies and regulatory requirements. This delivers big efficiency savings and provides a good example of how Gen AI is slowly but surely creeping into enterprises to provide real ROI.

Other AI benefits sit inside Experian. The company has ~7,000 product developers and software engineers who are 20-40% more productive because of Gen AI coding tools. Experian’s tech estate is in good shape because for the past eight years the company has migrated its data to the cloud. This process is now drawing to a close, reducing data processing time by ~60%, accelerating the launch of new products from months to weeks, and enabling clients to move to real-time analytics. The financial benefits of this effort are also coming through with lower capital intensity and the reduction of dual running costs as legacy mainframe datacentres are decommissioned. This development combines with the scaling of Experian’s major product initiatives and historically low financial leverage to give the company tremendous flexibility in the coming years.[8] Despite an uncertain macro-economic backdrop, these dynamics give us a high degree of confidence in Experian’s earnings over the medium term.

A pessimist sees the difficulty in every opportunity; an optimist sees the opportunity in every difficulty.

Winston Churchill[9]

Experian and LSEG are not isolated cases. In our view, the same disconnect exists to varying degrees across information service companies, software and e-commerce. These sectors are collateral damage in the excitement for the AI trade. We are in no doubt that AI is a transformative technology across nearly all industrial sectors. But whilst we remain optimistic about AI’s long-term potential, we are realistic about the pace of change and the technology’s limitations. The pressure on the shares of these companies has felt relentless in the past six months, but Alphabet’s progress this year shows how quickly and dramatically popular narratives can flip. Consistent with Alphabet (owned in the Strategy since 2013), our research into Experian and LSEG stretches back many years; from 2017 in the case of LSEG, since 2006 for Experian. Over that time, we have developed an understanding of them that leads us to independent conclusions. We believe the debate surrounding these companies can fail to account for their enduring competitive advantages. It often trivialises the depth and complexity of mutually dependent commercial relationships, the trust these represent, and the value they bring. It can further underestimate how management are reinvesting assertively to enhance the value their companies deliver to customers.

Experian’s and LSEG’s share price performance in 2025 is creating an opportunity, in our view. Experian is valued on a prospective 4.5% equity FCF yield. LSEG is at 6.1%. Both companies are capable of growing FCF per share in the low double digits. Both companies have growing financial flexibility to reinvest into their businesses or return excess capital to shareholders. We have added to the Strategy’s investments this year.

Experian and LSEG are representative of a portfolio that is valued at a significantly higher FCF yield to the wider market, despite far superior levels of financial productivity, reinvestment and growth.

Figure 12: Superior metrics at a cheaper FCF yield

Source: FactSet and Troy Asset Management Limited, 31 December 2025 . Neither past performance or forecasted performance are guides to future performance. Characteristics are shown excluding banks. FCF measures are based on trailing figures over the last 12 months. Asset allocation subject to change. All references to benchmarks are for comparative purposes only. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Global Equity Strategy.

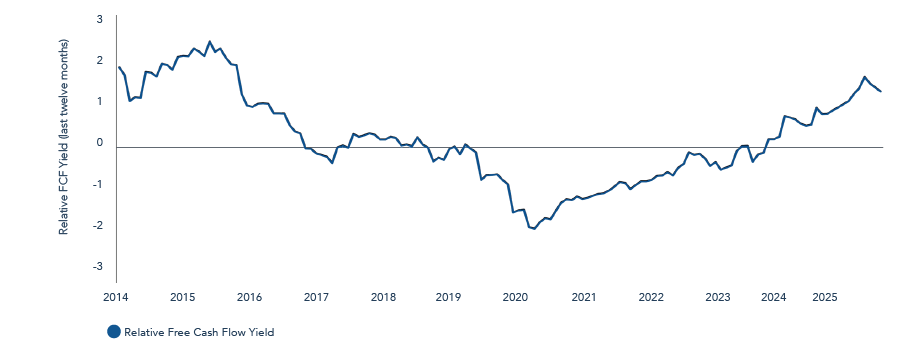

It is ten years since the Strategy last traded at such a high FCF yield compared to the market. In this time the quality and growth potential of its companies has improved, and we are confident in its prospects.

Figure 13: FCF yield at a historic discount

Source: FactSet, since inception, 31 December 2013 to 31 December 2025, GBP. Past performance is not a guide to future performance. Relative data of Troy Global Equity Strategy vs MSCI World Index. All references to benchmarks are for comparative purposes only.

In conclusion, as valuations of other parts of the market look stretched, indebted or are predicated on benign economic conditions, the Strategy is particularly well placed – reasonably valued, lowly levered, and economically resilient. In a dynamic environment defined by technological change, we believe our differentiated focus on adaptive reinvestment to sustain long-term growth is a powerful and durable foundation. Our actions will continue to be guided by a disciplined focus and our objective of achieving double-digit returns that compound over the long term. Our own capital is invested alongside our clients, and we have added to our personal investments in the Strategy during the year.

Thank you for your continued support. We wish you all a happy and prosperous 2026.

[1] To be clear, we are not averse to businesses with cyclical revenues – Alphabet and Meta Platforms, for instance, have cyclical advertising revenues. But we are averse to undifferentiated, low margin, low growth, capital intensive businesses, or those reliant on debt financing. Many will be inherently cyclical.

[2] The investment case for Alphabet was explored in the Strategy’s Half Year letter. See here

[4] The neoclouds are typically formally crypto-currency miners that have repurposed their GPU chip capacity to capitalise on the shortage of dedicated AI training capacity for AI labs. They are usually monoline businesses with concentrated customer bases and high financial leverage.

[5] On a total return basis, in GBP. Source: Bloomberg.

[6] The Strategy first acquired shares in the company in 2023. It has owned shares in Microsoft since the Strategy’s inception in 2013.

[7] Also a representative example for Azure’s ongoing momentum.

[8] We have written in the past about the strength of Experian’s financial model and the unusual level of control management exercise over the company’s earnings. See here.

[9] It is Churchill’s quote according to the internet, although the Churchill scholars find no record of him saying it. Beware of using chatbots to find pithy quotes!

The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Global Equity Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund.

Performance data provided is either calculated as net or gross of fees as specified in the relevant slide. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. This presentation may also contain forward-looking statements that are based on current expectations, estimates, forecasts, and projections. These statements are not guarantees of future performance and involve certain risks and uncertainties which are difficult to predict. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Information on the risks of the investment in the fund can be found in the Prospectus.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any product described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2026.