Our aim is to protect investors’ capital and to increase its value year on year.

The Greater Russian Agenda

Ση πατρίς εν γαρ τοις πόνοισιν αύξεται –

Your country becomes great when in trouble

Euripides – The Suppliants

In February 2020, the daily reality of face masks and lateral flow tests was unknown, as was the personal and economic toll to be wrought by Covid. Two years on, and not yet back on its feet, the world faces another major crisis.

Shock waves from the war in Ukraine are likely to be longstanding and far-reaching. At the epicentre of this conflict, we see humanity, cruelly pushed to its limits, capable of immense resolve and resourcefulness. From the effectiveness of Ukraine’s infantry against Russian tanks to the nation’s ability to maintain a working power grid, displays of defiance and ingenuity point to a country bent on independence. The irreconcilable gulf between the two countries’ positions makes the outlook uncertain and a swift resolution unlikely.

Meanwhile, the conflict is compounding inequalities around the world. Rising food and energy prices are hurting the poorest the most. In the US, the lowest 20% of earners spend nearly twice as much of their outgoings on energy as the top 20% do. The contrast is starker between countries. Across Sub-Saharan Africa, food makes up roughly 40% of the consumer price basket, compared with 14% in the US. Russia and Ukraine combined are crucial sources of both food and energy – Russia supplies around 10% of the world’s oil and 40% of Europe’s gas, whilst together with Ukraine the two countries produce 30% of the world’s wheat. Prices of agricultural commodities have sky-rocketed since the war began, with a raft of damaging consequences. These range from implications closer to home, as people in the UK are forced to choose between heating homes or feeding families, to food insecurity crises in emerging markets; Kenya has just declared a national disaster.

European countries are working to keep the lights on, most notably Germany which up until now relied on Russia for 65% of its imported gas. Longer-term, this will lead to more investment in alternative energy infrastructure, and will most likely accelerate the green transition. Western sanctions and Chinese ambivalence further suggest that Russia will be isolated on the global stage once the war is over. These implications from the war are surely not lost on Vladimir Putin and they run deeply counter to his agenda of a Greater Russia – an agenda he set out unequivocally in an essay to his armed forces last summer. With this context, it is unclear which, out of peace or escalation, he would now consider the lower risk.

Our approach at Troy is long-term, and it is rooted in the selection of companies well placed to determine their own fortunes. We seek to avoid businesses where too much of the risk is linked to external factors, such as those with excessive single-country exposures, or those whose profitability largely depends on commodity or energy prices that lie beyond their control. Within the Trojan Fund’s equities, we have never owned any stocks listed in Russia, and less than 2% of the companies’ underlying revenues were derived from Russia last year. This will be even lower today as companies have withdrawn from the country. In terms of our asset allocation, we never ‘position’ the portfolio for any single geopolitical or macroeconomic outcome, but when equity valuations become elevated we reduce our exposure to equity risk. Such was the shape of the portfolio entering into 2022. The modest exposure to resilient equities, combined with contributions from gold and the US dollar, helped in delivering a positive return across our multi-asset strategy during the first quarter.

My colleague Marc de Vos has written Special Paper No. 9, ‘Currency – Last but not Least’. In this he notes that currency, namely the US dollar, plays an important role in the way we manage risk in the portfolio. As wryly noted recently by a friend of Troy, the US is likely to emerge from this conflict as the ‘least hated superpower’. Marc explains why dollar hegemony is unlikely to be replaced any time soon.

The way things work: index-linked

Even if investors had predicted the war in Ukraine, such foresight would not necessarily have yielded the right investment decisions. Some assets, such as gold, have proven dependable during the crisis; others, such as conventional bonds, have strayed from their ‘safe haven’ status. Since December, the 30-year US Treasury bond has declined nearly -20%, and is c. 30% off its August 2020 high, its worst drawdown since 2009. This has been the story for bond investors the world over. The Bloomberg Barclays Global Aggregate Index, made up of global investment grade debt from 24 local currency markets, fell -6.2% in the three months to 31 March. Given the high valuation starting point, the downside risk for expensive corporate and government bonds has been a recurring theme of these Reports for some time. The portfolio’s bond exposure, by design, is entirely index-linked.

As inflation has risen, so too have expectations for interest rates, threatening to reverse a multi-decade long appreciation in nominal bonds. Inflation or index-linked bonds are, somewhat counterintuitively, not insulated from this risk. When index-linked bonds are held to maturity, the one variable component of their return is inflation, as both coupon and principal payments move in line with changes in the Consumer Price Index. Up until maturity however, as is the case with all bonds, prices fluctuate and more so the longer the bonds’ duration (i.e. the time to maturity). A combination of nominal rates and inflation expectations – the former minus the latter produces the ‘real yield’ – determine the price of the index-linked bond. Whether index-linked bonds actually make money depends on the degree to which one component moves relative to the other. If market expectations for inflation increase more than nominal bond yields, real yields will fall and index-linked bonds will generate positive returns. However, if markets start to price in an increase in nominal yields without a commensurate increase in inflation expectations, real yields will rise and index linked bond values decline.

The degree to which this occurs in either direction depends on multiple factors, not least the starting point for yields. The nominal yield on the 10-year US Treasury has been on a downwards trajectory for four decades, moving from a peak of 16% in 1981 to 1.5% at the start of 2022. Meanwhile, US inflation in February reached 7.9%, a level not seen since 1982 when rates were around 15 percentage points higher. Is it any wonder that the Federal Reserve is now responding, somewhat belatedly, by acknowledging that yes, inflation might be a problem and that they should probably try and do something about it? The bond market is now pricing in ten interest rate hikes of 0.25% (or five of 0.5%) for the next twelve months. In terms of what this has meant for our index-linked bond holdings, market-implied expectations for inflation have risen but less so than this move in nominal rates. The result has been a rise in real yields, causing index-linked bond prices to fall – albeit this has been a flesh wound in comparison to the casualties in non-inflation-linked debt.

Losing the plot?

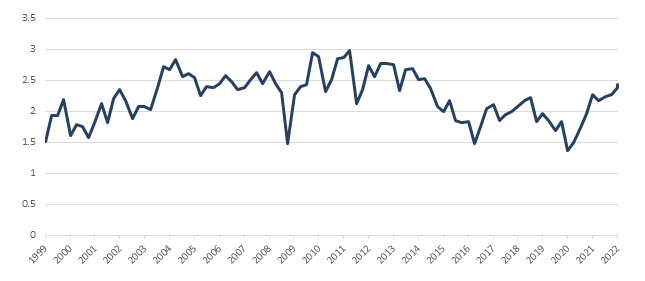

Figure 1: 5-year, 5-year US breakeven rate: Inflation expectations for 2027-2031 are within the recent range %

For all the short-term market movements, it is worth setting out our longer-term expectations for both inflation and nominal rates. Although shorter-term inflation expectations have risen, this is not the case for inflation expectations further out. For the five years between 2027 and 2032, market prices imply that US inflation will average 2.4% (Figure 1). That represents a minor overshoot of the Federal Reserve’s target of 2%. In other words, investors are asked to pay a very modest premium to protect their savings should consumer prices overshoot. Perhaps this is unsurprising given how low and stable consumer prices have been for so long. Even in the midst of the highest inflation for 40 years, it is remarkable the extent to which investors remain anchored to what has gone before.

However, we are of the view that the longer inflation persists, the more likely it is to become ingrained. The shock to supply chains from the pandemic has been prolonged by events in Russia and Ukraine, as well as China’s ongoing zero-Covid policy. Inflation in the US has also started to spread more broadly into areas such as rents and services. This is occurring at the same time that an increasingly strident labour force is calling for wages to reflect their higher cost of living. That call is currently being met. We will watch to see how the bargaining power of labour develops, since higher wages remain key to supporting demand beyond the dissipating effects of supply shocks. With these seeds planted however, it seems likely that we will see a coming decade that is more inflationary than the last.

At the same time, owing to high debt levels, there is likely to be a ceiling on how far rates can rise. Nobody, including central bankers, knows precisely the level of interest at which the economy will buckle. But bond yields today are close to where they were at the start of 2019, when the Fed last pivoted away from its tightening agenda. Levels of debt to GDP are much higher today in the wake of all the financial strain required to get through the pandemic. Another pivot is unlikely to be imminent, given the current disconnect between raging inflation and lowly interest rates. To maintain its credibility, the Fed needs to be seen to be doing something, particularly as this is now a political agenda. Polls show that Americans are currently more concerned about inflation than they have been in forty years. That said, it’s worth remembering just how quickly these things can change. As recently as September last year, the Federal Open Market Committee was forecasting, as per the committee’s ‘dot plot’, one rate rise for this year. Now it is predicting six. A volte face if ever there was one.

The fact that longer-term inflation expectations remain slightly above 2%, suggests an ongoing belief in the power of the U.S. Central Bank. It is clear though, from the reactive nature of their actions, that their roadmap is no more accurate than any of ours. It is uncertain as to where exactly inflation will end up, but we do not expect the Fed to sacrifice the economy to fight it. For that reason, it seems probable that we experience another U-turn in the not-so-distant future. Meanwhile, a tolerance for more variable and higher rates of inflation is likely to remain politically preferable to upending the economy with penal interest rates. That is particularly likely given that a large part of inflation is supply-driven; no amount of rate hikes is going to solve the problems of supply chain bottlenecks around the world.

A limited ability to control inflation or raise rates points to a future where real yields are more negative – i.e. inflation exceeds the rate of interest, known as financial repression. This is ultimately the only outcome that indebted economies can afford. It is also one in which index-linked bonds should offer valuable protection.

Short-term resilience without compromising the future

“We’re not really ever positioning ourselves. We’re simply trying to do the smartest thing we can every day when we come to the office. And if there’s nothing smart to do, cash is the default option.”

Warren Buffett (2003)

We are nonetheless mindful that the market may continue to anticipate higher rates as central bankers grasp the inflationary nettle, while longer-term inflation expectations take longer to budge. There is every likelihood, as occurred in the first few weeks of this year, that this unfavourable environment for index-linked bonds coincides with equity markets falling too. For this reason, and with an eye on minimising drawdowns, we maintain a relatively modest duration in our index-linked exposure. At the time of writing it stands around five years.

It is also the case that, with our equities, we incorporate an awareness of discount rate sensitivity into the prices we are prepared to pay. That does not mean buying the shortest-duration stocks around – i.e. those with the lowest price-to-earnings multiples (“PEs”). If those types of multiples existed for fantastic businesses, decision-making would be easy. Today’s market however is a far cry from that in which Benjamin Graham honed his craft. It is more efficient, and the lowest PEs tend not to accompany businesses with excellent prospects. One might do well from sectors such as energy or mining for as long as rates move from ‘x’ to ‘x+y’. But, ultimately, sustained outperformance by any stock needs to be accompanied by ongoing earnings growth.

A lasting rotation into so-called ‘value’ sectors, including those with commodity exposures, did occur during the Noughties. This was underpinned by raw material demand from China; the country had entered the WTO and growth in goods manufacturing and construction was booming. Such a dynamic does not exist today so when today’s supply chain crisis in grains and energy abates, which at some point it will, from where will that lasting demand for raw materials derive? We continue to favour companies where we are confident that revenue and earnings growth will be long-lived, but also where the valuations do not overstate the company’s potential. Sky-high multiples are off the menu, and a low equity exposure gives scope to add when valuations return to earth.

Finally, cash is the ultimate short-duration asset. It can be invaluable in the early stages of a market starting to price in inflation. If all asset classes fall together, the one that is able to retain its nominal value offers tremendous optionality. The ability to reinvest cash, at higher prospective rates of return, is an effective way of benefitting from rising yields. This, combined with our equity allocation and shorter-duration index-linked bonds, is in-keeping with the portfolio’s long-only approach. It also does not require a compromise on the quality of the assets that we own.

The wisdom of crowds

The bond market is often seen as the Buddha of the financial system, bestowed with predictive powers beyond those afforded elsewhere. It is therefore interesting to observe that in the month of March, equities were on a tear while bond markets continued to sell off sharply. This subverted the narrative at the start of the year, when fears of higher yields, and of higher discount rates, were knocking the prices of many more expensive equities on the head.

Rather than read too much into this, it pays to realise that markets will dance to their own tune and can often behave irrationally. Trading volumes, in equities and bonds alike, have been thin over the past few weeks, with retail investors in particular leading price discovery for stocks. Commentators rationalising the moves have suggested that perhaps stocks, after all, are now a great hedge for inflation.

In bond markets too, conclusions are being drawn – perhaps too early. The prevailing narrative is that a yield curve inversion, which recently occurred and measures the spread between a long and short-dated Treasury, presages a recession. Historically, yield curve inversions have been followed by recessions, but often with a lag of up to three years.

How helpful is this information and on what logic is it based? The reasoning behind it, beyond a set of historical observations, is that, for banks, higher short-term rates make deposits more expensive than long-term loans are profitable. This disincentivises lending which hurts the economy. There is also the fact that the market, pricing in lower rates in the longer-term, believes that rates will need to fall due to anticipated economic weakness. But what proportion of deposits are 2-years in duration? If one considers that most are shorter, the 10-year, 3-month spread is probably a more useful guide to future lending patterns. Using the 3-month also excludes a flurry of rate rises which markets are pricing in but which are yet to happen. Because the 3-month yield remains considerably below the 10-year, this barometer is not currently inverted and, on that basis, not forecasting a recession.

The winds of change

This year began with equity and bond markets focused on central bank tightening. Whilst events in Ukraine continue to unfold, the market’s preoccupation with interest rates appears, for now, to be back in the driving seat. This whip-sawing of markets has been painful for many investors, and over a relatively short time frame. In an era where live prices blink constantly from a screen, it can be tempting to follow the mood music. Fear of missing out lures many into chasing the latest thing. With the defence and energy sectors having performed particularly well this year, many are not only reconsidering the investability of these stocks, but are also drawing conclusions about what the recent outperformance means for issues of an ESG (environmental, social or governance) nature.

There is certainly change afoot but we would refute any simple conclusion that ESG no longer matters. Prior to 2022, the world had already been moving away from an approach of straight sector-based divestment, towards a more considered integration of ESG matters. A company’s direction of travel and its pace of change on significant issues matter just as much as where it stands today. Across our mandates, we consider an understanding of a company’s social and environmental footprints to be fundamental in determining the competitive advantage and future financial returns of that business. Rather than diminish this importance, events in Ukraine seem to be building on the way that Covid helped awaken the public conscience across a range of social issues. Meanwhile, by underlining our current dependence on fossil fuels, the energy crisis also highlights the need for investment and for change.

We expect that this year will continue to be difficult for investors to navigate. We do not consider our role to be that of making precise macroeconomic or geopolitical forecasts. Rather, we must ensure that the portfolio is resilient for a variety of short-term scenarios without compromising on its ability to generate long-term returns. The importance of modest duration in index-linked bonds and of resilient business models in equities cannot be overstated in this context.

Charlotte Yonge

Sebastian Lyon

April 2022

Disclaimer

All information in this document is correct as at 31 March 2022 unless stated otherwise. Please refer to Troy’s Glossary of Investment terms here . Past performance is not a guide to future performance. The document has been provided for information purposes only. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. The document does not have regard to the investment objectives, financial situation or particular needs of any particular person. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The views expressed reflect the views of Troy Asset Management Limited at the date of this document; however, the views are not guarantees, should not be relied upon and may be subject to change without notice. No warranty is given as to the accuracy or completeness of the information included or provided by a third party in this document. Third party data may belong to a third party. Benchmarks are used for comparative purposes only.

Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Asset allocation and holdings within the fund may be subject to change. Investments in emerging markets are higher risk and potentially more volatile than those in developed markets.

The fund(s) of Trojan Investment Funds are registered for distribution to the public in the UK but not in any other jurisdiction.

The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents, or as the case may be the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

In Singapore, the offer or invitation to subscribe for or purchase Shares is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act. This document may not be provided to any other person in Singapore.

All references to indices are for comparative purposes only. All reference to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2022. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764).

Copyright: Troy Asset Management Limited 2022