What is the role of fixed income in the portfolio?

Our approach to multi-asset investing is grounded in an ‘equities first’ approach. Over time, equities have been and will likely continue to be, the most important driver of risk and return for the portfolio. The strength of this mandate is our ability to dynamically shift our allocation to stocks in response to valuations and the wider opportunity set. We believe that the portfolio’s fixed income¹ exposure performs a critical role in enabling this flexibility. It also offers invaluable diversification and protection for our investors’ capital. Finally, fixed income continues to be an important driver of portfolio returns in its own right and has contributed c.20% of the annualised return for the strategy since launch in 2001. The importance of this latter role grows when prospective returns from equities are lower, as we believe is the case today.

Since the strategy’s inception, four pillars have made up its asset allocation: equities, fixed income, gold and liquidity. In determining the split between the four, we weigh up the relative merits of each and their expected returns. Equities play an essential role in the portfolio, but it is not appropriate for them to be the predominant asset class at all times. This mandate’s objective is to ‘protect investors’ capital and grow its value in real terms over the long term’. Over the mandate’s 23-year history, fixed income has played a vital role during times of equity market excess, as well as the ensuing periods of volatility and weakness for share prices.

This note sets out our approach to fixed income, the types of investments we favour and those we seek to avoid, and the role that fixed income has played during three important market drawdowns in the strategy’s history. Finally, this note will examine today’s opportunity set and why we believe that index-linked bonds in particular offer attractive, risk-adjusted returns.

Defining the universe: what we seek to avoid

As with equities, Troy’s investable universe for fixed income is not static. Rather, it will evolve over time, whilst continuing to be defined by a clear framework. The overriding features of this framework, for both equities and bonds, are a high threshold for quality and a common-sense approach to risk. When it comes to fixed income, this means debt issued by sovereigns or corporates with strong governance and with the ability and the willingness to repay their debts. At times when returns from such bonds look meagre, we will opt to sit on the side lines rather than compromising on quality. This can be achieved either by assuming shorter duration debt or by holding more in the ‘liquidity’ portion of the portfolio, which tends to be invested in conventional UK gilts or US treasuries with less than two years to maturity.

When Troy’s Multi-Asset Strategy was established in 2001, it was expressly designed to be managed independently of benchmarks. As a result, no relative-return mindset propels us to move further out the risk curve for the sake of short-term gains, only to risk permanent capital loss further down the line. This focus on absolute levels of risk and return was perhaps most in evidence during the 2010s, when an abundance of liquidity, combined with zero interest rates, compressed risk premia around the world. This significantly impacted bond markets, where the stock of debt globally trading on negative nominal yields rose from around zero in 2014 to $18trn in 2020. The temptation for many was to reach for return and, in fixed income, this meant investing in the bonds of riskier, less credit-worthy issuers or extend duration. During this time, we held a combination of UK and US index-linked government bonds, reducing our risk via the reduction of duration and increasing liquidity as the decade progressed. The approach no doubt appeared boring to many and was counter to much of the received wisdom at the time.

What we do do: three important drawdowns

- May 2001 – March 2003

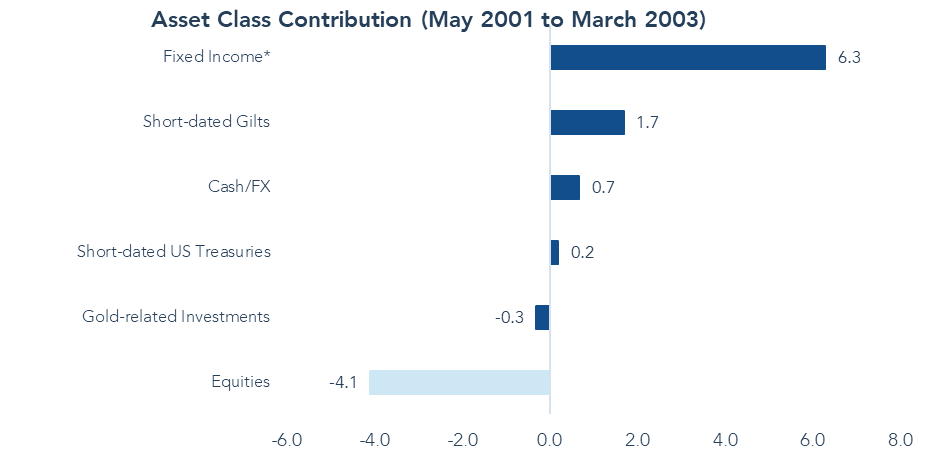

At the inception of the strategy in May 2001, the world’s equity markets were still contending with the unravelling of the dot-com bubble. This particular bear market, which began in late 2000 and continued into 2003, saw c. -50% drawdowns for both the S&P 500 and the FTSE All-Share Index. The Trojan Fund was in existence for most of this, witnessing a -45% fall in the FTSE All-Share Index during its first two years. During that time, the Fund delivered a positive return of c. +3% thanks to a prudent allocation to a combination of index-linked bonds, corporate debt and nominal bonds, and a modest allocation to equities. Each of the components of the fixed income exposure contributed positively to the Fund’s returns during the period, with US index-linked bonds (the largest allocation) the main driver. US index-linked constituted c. 30% of the portfolio by the end of 2001 and generated strongly positive returns for the strategy thanks to falling real yields which followed the equity market down into 2003.

*Within ‘Fixed Income’, US TIPS accounted for 4.3% of the overall contribution.

Source: Troy Asset Management Limited and FactSet, 31 May 2001 to 31 March 2003. Past performance is not a guide to future performance. Contribution to return is provided as gross absolute returns in local currency and does not include charges and fees. Currency exchange rates will impact the return of non-GBP securities. Asset allocation and holdings are subject to change.

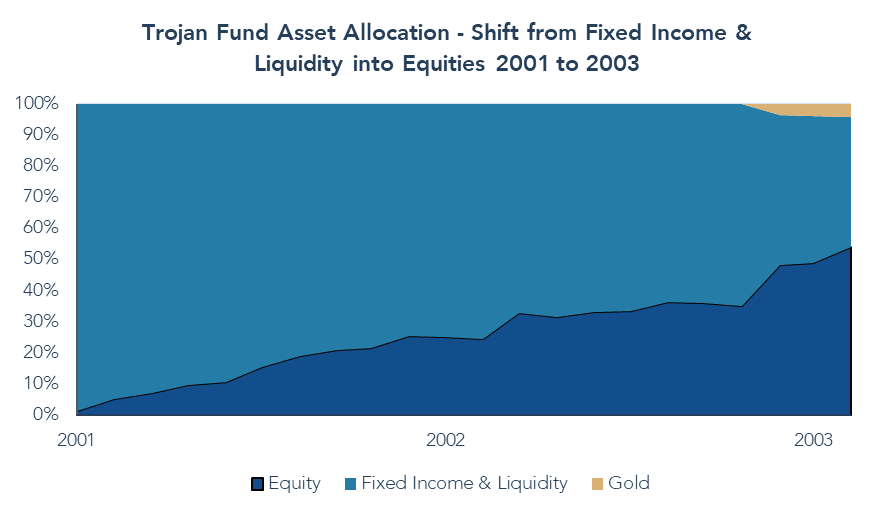

During this period, fixed income was able to perform two roles. Firstly, correlations were such that fixed income acted as an effective offset to equity market weakness. This inverse relationship between stocks and bonds does not always hold, as we shall come on to describe. Secondly the portfolio’s bond exposure, having performed well, put the strategy on the front foot to be able to lean into equity risk in 2003; it also provided an invaluable source of funds. This, along with the Fund’s liquidity, enabled the equity weighting to increase from a low single-digit exposure in the summer of 2001 to over 50% by the end of March 2003 (above).

Source: Troy Asset Management Limited and FactSet 31 May 2001 to 31 March 2003. Asset allocation and holdings are subject to change.

2. 2008

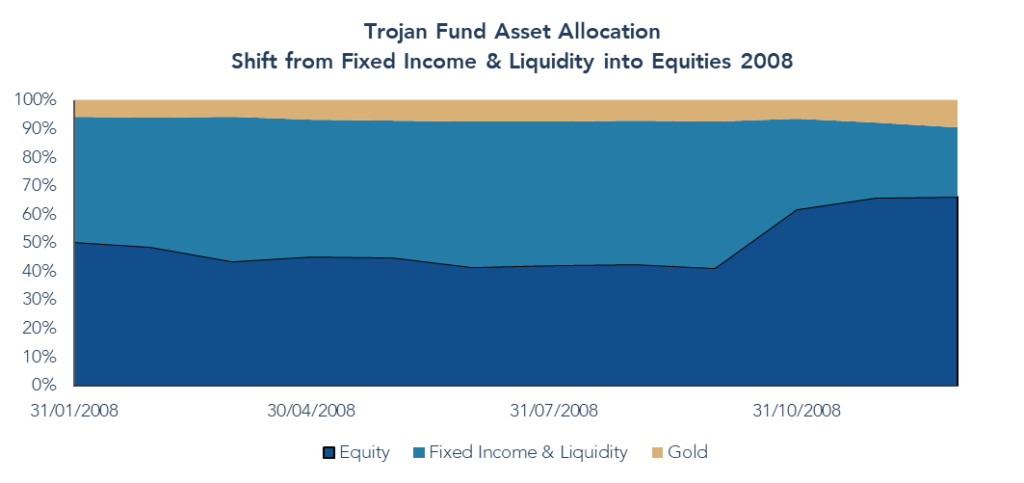

In 2008, a combination of foreign currency, conventional sovereign bonds, and a modest exposure to equities, enabled the strategy to generate a positive return for the calendar year. This was a year in which the US market fell -37%² and the UK market -30%. Intra-year drawdowns for these indices were more extreme. As with the bear market of the early noughties, fixed income provided a helpful offset to the portfolio’s equities. This came in the form of developed markets sovereign debt, namely Singaporean, UK and Austrian bonds, which also formed an important part of the liquidity that was deployed into both equities and index-linked bonds when markets declined. The strategy’s weighting to equities moved from 44% to 66% over the course of 2008. (below).

Source: Troy Asset Management Limited and FactSet 31 December 2007 to 31 October 2009. Asset allocation and holdings are subject to change.

3. COVID-19

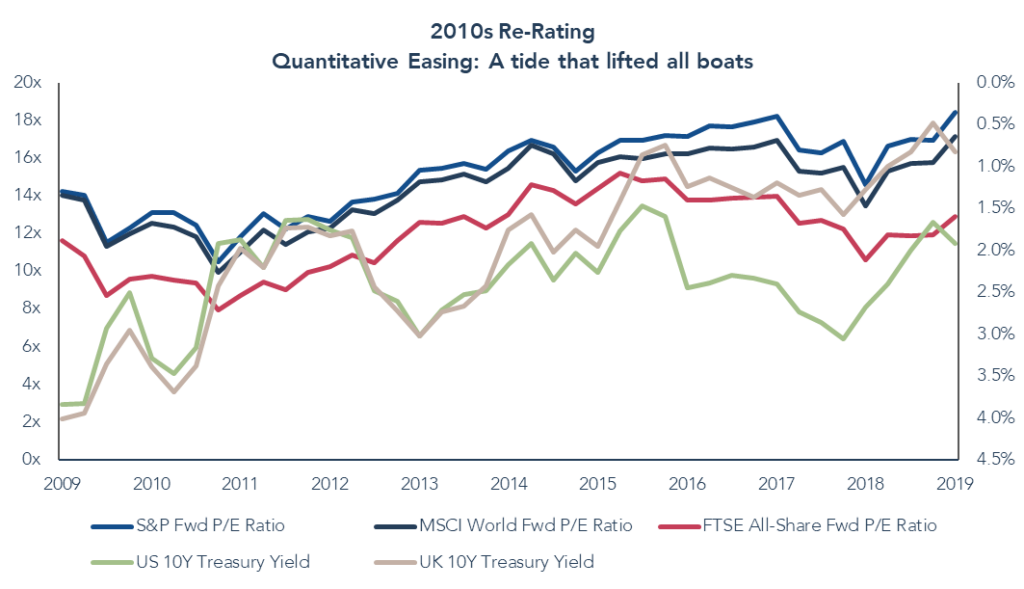

Quantitative Easing was the tide that lifted all boats in the years that followed the Global Financial Crisis. An increase in the valuations of all asset classes increased the vulnerability of prices across the board, reducing the likelihood that the inverse relationship between stocks and bonds, which had protected capital in the drawdowns of 2001-03 and in 2008, would hold during the next crisis.

Source: Bloomberg, December 2019. Past performance in not a guide to future performance. Yield is to maturity is inverted and is shown in the RHS. Please refer to Troy’s Glossary of Investment Terms. P/E refers to price/earnings.

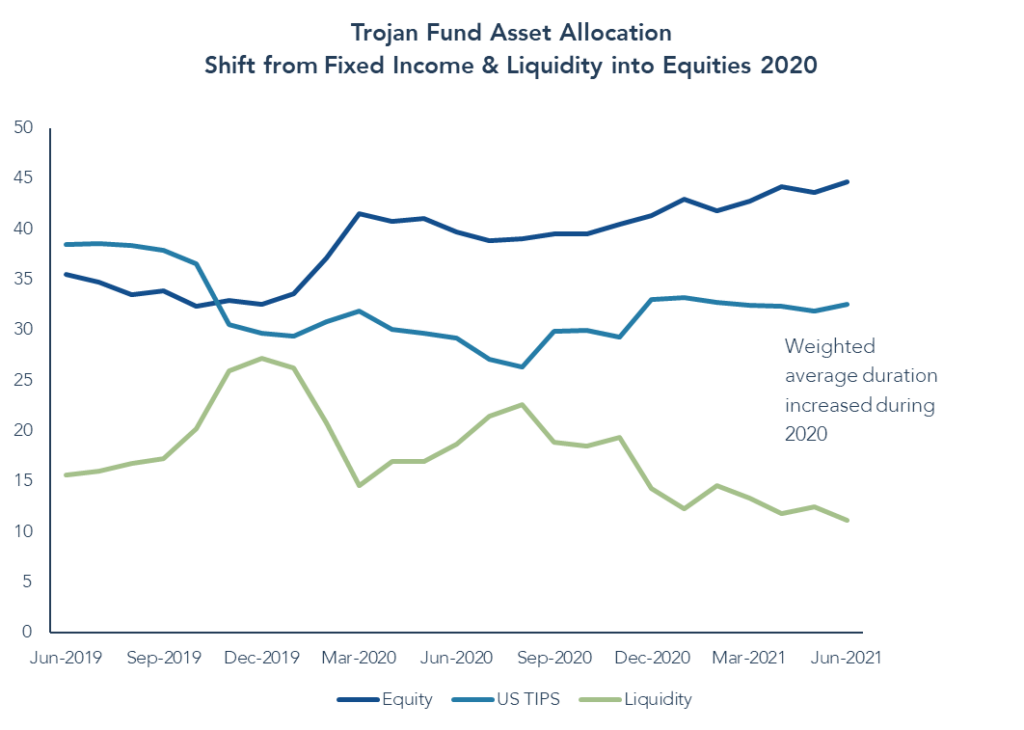

As valuations reached multi-year highs for both stocks and bonds towards the end of the 2010s, we reduced our equity allocation and took on selective fixed income exposure. This entailed selling the strategy’s holdings in UK index-linked bonds in 2019, where valuations had reached extreme levels, and holding modest duration in the portfolio’s US TIPS, where real yields remained positive. We were prepared to hold a substantial portion of the strategy in liquidity despite the negligible rates of interest available on cash and Treasury bills at the time. This not only preserved its nominal value but also provided invaluable dry powder to deploy during the COVID-19 downturn when we increased the portfolio’s exposure to both equities and index-linked bonds, as both asset classes fell simultaneously in March 2020. During the first quarter of that calendar year, the strategy was roughly flat whilst UK equities fell by -25%.

Source: Troy Asset Management Limited and FactSet. Asset allocation and holdings are subject to change.

2024: the opportunity today

Fast forward to 2024 and we have witnessed much change in bond markets over the past two years. We, as investors, have also learnt lessons as regards duration, inflation expectations and the evolving role of fixed income within this strategy. In summary, fixed income as an asset class remains more relevant than ever today, pricing in as it has done a shift in discount rates which equity markets, on the whole, have yet to incorporate.

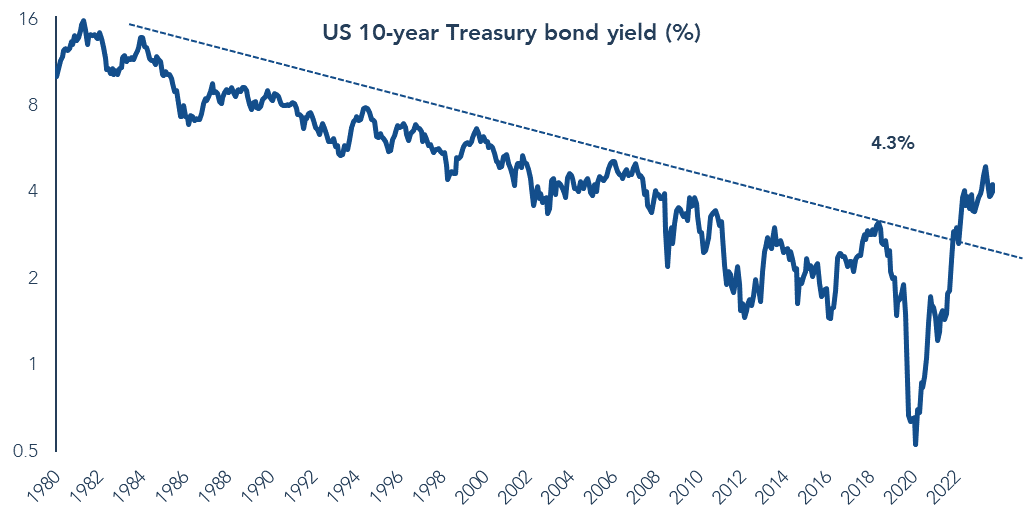

The rate hiking cycles which have occurred around the globe, and specifically in the US from March 2022 to July 2023, mark the fastest and most significant increase in interest rates since the early 1980s. This change in the risk-free rate follows the prolonged period of monetary excess that prevailed in the 2010s and extended into 2021. Whilst we do not think that the ramifications of this change in the cost of capital have been fully digested by all markets, there has been a pronounced reversal in the multi-decade bull market witnessed in most developed market sovereign bonds, as illustrated below by the US 10-year Treasury yield.

Source: Bloomberg, logarithmic scale, 29 February 2024. Past performance is not a guide to future performance.

Whilst corporate debt markets have also seen yields rise to reflect a higher risk-free rate, the spread between yields available on high-quality corporate bonds and those on government bonds remain below historical averages. The US BBB/Baa corporate spread against the US 10-year Treasury is currently 1.3%, versus a 20-year average of 1.8% and a peak of c. 6% during the Global Financial Crisis. In our opinion, this represents scant premium for the greater illiquidity of the corporate credit asset class, alongside its greater likelihood of exhibiting a positive correlation with equity markets when risk assets turn south. That is not to say that we do not continue to consider corporate credit as an investable asset class, but the valuations on offer today do not excite us.

Based on a bottom-up appraisal of valuations and our outlook for both inflation and interest rates, the strategy’s fixed income allocation today is comprised predominantly of US index-linked government bonds. This is an area of fixed income which we believe should generate attractive risk-adjusted returns on an absolute basis, whilst also protecting investors’ capital ahead of inflation. Index-linked government bonds, in both the US and the UK, are currently pricing in a level of inflation roughly commensurate with the average rate experienced over the past three decades. This may be accurate, but we suspect that the market has failed to adjust for many of the changes which have occurred over the past few years. Many of the forces which kept inflation low and stable from the early ‘90s to 2021 are shifting, namely globalisation and the suppression of real wage growth. Growing nationalism, labour’s increased bargaining power and a greater propensity on the part of governments to provide fiscal support, whether to lower-earners or via the reshoring of manufacturing and decarbonisation initiatives, are all likely to set us on a path of higher inflation for some time to come. Higher inflation risks eroding the real wealth of investors, posing a direct risk to our mandate of capital preservation.

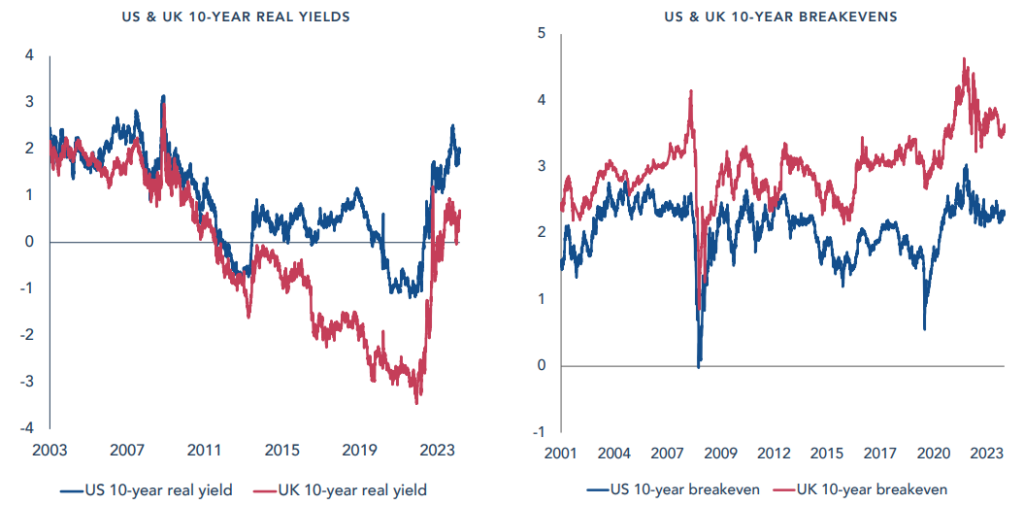

At the same time that inflation risks have grown, government-backed inflation-protection is more attractively valued than it has been for 15 years. Real yields, which determine the prices of index-linked bonds, are driven by a combination of both inflation expectations (also known as ‘break-evens’, or the rate of inflation required over a bonds life to give the same return from an index-linked bond as from an equivalent conventional bond of the same maturity) and nominal yields³. Whilst market expectations for inflation have moved very little, in spite of the uptick in actual inflation over the past three years, nominal bond yields have moved substantially. This has driven a marked increase in real yields, as seen below, for both US and UK index-linked bonds4. The higher yield on US securities makes them slightly more attractive than their British counterparts, but the valuation divergence has narrowed. Based on a 2% real yield, investors holding an index-linked bond to maturity will receive an average annualised return of 2%, in addition to the realised rate of inflation over that period. If actual inflation turns out to be higher than the break-even, which for the US 10-year is currently 2.3%, returns from index-linked bonds will surpass those of their conventional equivalents.

Source: Bloomberg, March 2024. Past performance is not a guide to future performance.

The chart above left shows the downward march in real yields that occurred up until 2021, followed by a sharp repricing. We reduced our TIPS duration at the end of 2021 to around 4 years across a number of US index-linked bonds. This modest duration, as well as the selection of index-linked over conventional bonds, helped to mitigate the negative impact from this part of the portfolio during the worst year for US government bonds since the signing of the US constitution. It did not however prevent inflation-linked bonds detracting from performance; the strategy fell low single-digits in 2022 but would have been in positive territory had index-linked bond prices not declined. These negative returns from so-called inflation protection, in a year when US CPI reached its highest since 1982, were in many ways counterintuitive. They (re)-taught us that market expectations can remain anchored to the recent past for a long time.

We expect that inflation expectations are likely to remain subdued until the market can see clear evidence to the contrary. This may require for inflation to fall further in the short term, before it becomes clear that the steady state is settling at a higher level. In the meantime, we have increased our duration to c. 5 years on the back of lower valuations. We continue to hold the bulk of our exposure in shorter-dated index-linked bonds that will continue to grind out a return of the real yield, plus experienced inflation, to maturity.

Conclusion

“In Olympic diving, you know, they have a degree of difficulty factor. And if you can do some very difficult dive, the payoff is greater if you do it well than if you do some very simple dive. That’s not true in investments.”

Warren Buffett

Our ongoing investments in fixed income should be viewed in the context of our mandate for capital preservation and our overall investment approach. Whilst capital markets attract a huge amount of collective brainpower thanks to the potential returns available, a competitive tendency towards excessive complexity can lead to adverse outcomes for the end investor. A preference for intellectual cartwheels over more pedestrian activities will often lead to the favouring of more convoluted but not necessarily higher-returning investment strategies. Meanwhile, impatient dispositions can lead to overtrading at the expense of the benefits of compounding that come from holding investments over a longer time frame. This hyperactivity seems to be especially common in fixed income investing where the accrual of gains, particularly in less risky parts of the market, may at times feel like the equivalent of watching paint dry.

When it comes to our approach to fixed income, as with equities, we are long-only and long-term. We consider the big picture risks facing investors, whilst scrutinising every investment from a bottom-up perspective. A comprehensive understanding of risk and return, grounded in the nature of the bond’s issuer, the economic outlook and the valuation investors are being asked to pay, gives us the confidence to invest on a strategic basis. It also gives us the confidence to eschew investments where prospective returns are likely to be low or where there is a higher risk of permanent capital loss. Fixed income will continue to play an essential role for the strategy, both in terms of contributing to returns and in terms of managing risk. As with eras past, we believe that today’s holdings are well placed to deliver on both.

¹ The terms ‘fixed income’, ‘debt’ and ‘bonds’ will be used interchangeably throughout this note. Whilst index-linked bonds produce an income that adjusts with inflation, such bonds are generally considered to fall under the ‘fixed income’ umbrella. The term shall be used in this way throughout the note.

² S&P 500 fell -14.3% in sterling terms during the calendar year of 2008.

³ The real yield is calculated as the nominal yield minus the break-even rate of inflation. The nominal yield is the yield from a conventional bond.

4 It is worth noting at this juncture that we do consider other sovereign debt markets, as we have for this strategy historically, but that the US and the UK offer not only superior liquidity (versus for example the much less liquid Japanese government bond market), but also the backing of sovereigns in each case with fiscal and monetary autonomy. This latter point is important in terms of the ability of governments to repay their debts. It is also important in terms of the ability, and likelihood, of higher fiscal spending which is likely to bring about a more sustained level of inflation.

Disclaimer

Please refer to Troy’s Glossary of investment terms here. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-asset Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund.

Performance data provided is either calculated as net or gross of fees as specified . Fees will have the effect of reducing performance. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2024. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Ltd 2024.