Read why Blake Hutchins, manager of the Trojan Income Fund, thinks the outlook for UK equities is attractive.

An improved backdrop for UK equities

In my recent meetings with investors, and even when talking to friends, it is clear that the current mood towards the UK is miserable. With high interest rates, stubborn inflation, declining house prices, and alarmist media headlines, it is no wonder that negative sentiment hangs over the UK equity market. In the year to date, there is also a sense of having missed out. The S&P 500 is up c.20% YTD versus a flattish UK market. The ‘AI frenzy’ has driven extraordinary gains in some of the USA’s biggest companies; NVIDIA, up >200%, Microsoft, up c.50%, Alphabet, up c.40% and Meta up >160%. UK investors can be forgiven for feeling a little sorry for themselves.

This week has felt a little different. UK shares have rallied strongly on the back of a softer than expected inflation print – the first we have seen in this rate cycle. With sentiment so low and rate expectations already very high, it strikes me that further downside is limited and that the outlook for UK equities is attractive.

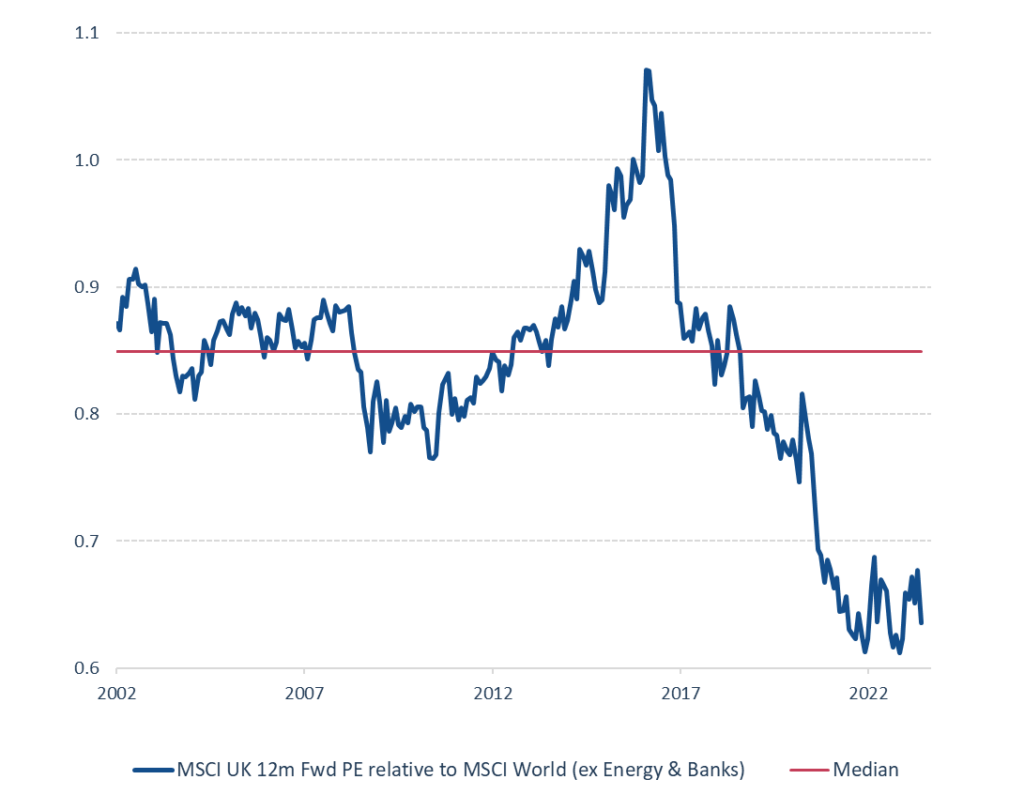

Firstly, valuations in the UK are incredibly depressed compared to other markets. This is reflected in Figure 1, where the overall PE ratio for the UK market, relative to the MSCI World is at a 20-year low. Such valuations are bound to attract buyers. Anecdotally, it is encouraging for me to see my global equity colleagues taking notice of UK valuations. Troy’s Global Income strategy has a meaningful allocation to the UK market, whilst our Global Equity Fund colleagues have started two new holdings this year in world-class UK businesses trading at notable discounts to their US peers.

Figure 1: MSCI UK 12M FWD P/E relative to MSCI World (ex energy & banks)

Past performance is not a guide to future performance

Source: Factset and Troy Asset Management Limited, 30 June 2023. All references to benchmarks are for comparative purposes only. P/E is price to earnings.

Secondly, if we are moving past the peak in inflation, it could mean that sterling’s strong rally, from close to parity with the dollar in September last year, to a recent high of $1.31, takes a pause for breath. This would be good for the many international earners in the UK market, including your Fund’s largest holdings – Unilever, RELX and Diageo.

Finally, UK domestic stocks should benefit from moderating base rate expectations. Once peak rates have been priced in by the bond market, we can reasonably expect that investors will start to look through current earnings weakness from those companies focussed on the UK economy. The past few days have proved a case in point, benefiting the select domestically focused names in your portfolio. These include property-related stocks Howden Joinery and Big Yellow Group, consumer discretionary names Next and Domino’s and the investment platforms St. James’s Place, AJ Bell and IntegraFin.

Time will tell whether this week’s positive inflation news is a one-off or the start of a welcome disinflationary trend. But we are feeling upbeat – past experience tells us that times of widespread pessimism and historically low UK valuations bode well for future returns.

I would like to end by wishing readers a wonderful Summer.

Please refer to Troy’s Glossary of Investment terms here. Performance data is net of fees with income reinvested unless stated otherwise. All performance and income data is in relation to the stated share class, performance of other share classes may vary. Past performance is not a guide to future performance. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the Fund’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. Tax legislation and the levels of relief from taxation can change at any time. The yield is not guaranteed and will fluctuate. There is no guarantee that the objective of the investments will be met. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. For further information on Troy’s use of benchmarks, you should consult the Fund prospectus. Investments denominated in currencies other than the base currency of the Fund may be affected by movements in currency exchange rates. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. The investment policy and process may not be suitable for all investors. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Ratings from independent rating agencies should not be taken as a recommendation. The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The sub-funds are registered for distribution to professional investors only in Ireland. The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information document(s) or, as the case may be, the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland. The offer or invitation to subscribe for or purchase shares in Singapore is an exempt offer made only: (i) to “institutional investors” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “SFA”); (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305 (1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA. Issued by Troy Asset Management Limited (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP . Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training.

© Troy Asset Management Limited 2023