The investment objective of the Trojan Global Equity Fund (the “Fund”) is to achieve capital growth over the long term (at least 5 years). Our strategy seeks to exploit a persistent market inefficiency that misprices those rare businesses that can grow at sustainably high returns on their capital. We invest for the long term in companies that have the resilience to withstand unexpected shocks and the adaptability to thrive in a dynamic global economy.

Back on the horse

Gabrielle spends her Saturdays at this time of year blowing away the cobwebs by jumping rails and hedges with the local charity ride. There are plenty of thrills and spills along the way. This year we seem to return to the office on a Monday to face the biggest hedges of them all – in financial markets. Investors have collectively fallen from their horses and the picture is not a pretty one. Nearly all asset classes have suffered and, outside of the dollar and energy stocks, there have been few places to hide.

There is a lot that can and has been said about the macroeconomics backdrop and we are not going to add to it with this Newsletter.[1] In a grim year for investors, we do, however, want to remind you why we invest as we do in the Trojan Global Equity Fund. We believe that the compounding power of great companies, with sustainably high returns on capital, can reliably build wealth for their owners. We aim to invest in them at a reasonable price, in a concentrated portfolio, and hold onto them for a very long time. We know from experience that we need to be discerning, do our research, and take the rough with the smooth. These special companies will ultimately do the hard work of capital accumulation for us. The difficult part is to stay the distance and not be swayed off course.

The Fund’s investments, strategy and methods are broadly unchanged since the start of the year. We are undeterred by deteriorating macroeconomic conditions, not because we underestimate the potential for disruption, but because we continue to see plenty of opportunity in our investments over the long haul. The health of the Fund’s holdings is the most important consideration and we remain focussed on the quality of their earnings and cash flows today, as well as the prospects for growth well into the future.

Life’s staples

Our optimism in the Fund’s strategy and its investments derives, in part, from the essential nature of our businesses. They sell products and services that are bought out of loyalty, necessity or habit – sometimes all three. For example, in an increasingly cashless world, Visa and Mastercard are the rails that keep commerce running whilst providing vital data and cyber-security services for merchants and card issuers. Elsewhere, Agilent’s instruments and consumables become an operating system upon which research labs of all sorts depend for data collection and analysis – across biopharma, food, forensics and chemicals. Lastly, a typical ophthalmic surgeon can complete a cataracts procedure in about eight minutes by accessing Alcon’s full suite of replacement lenses, surgical equipment and disposable supplies. The Fund’s broad investments in the technology sector share this same essential and recurring quality. The services of Alphabet, Microsoft, Intuit and Meta Platforms are woven deep into the fabric of modern life, used by hundreds of millions of businesses and billions of consumers each day for a wide variety of online tasks. They are ‘tech staples’.

The portfolio’s companies collectively meet demand that is both highly resilient and highly likely to grow over the next five, ten, and twenty years. There will, of course, be some sensitivity to the ups and downs of the business cycle. This is to be expected if consumer and corporate spending declines. Sticking with the examples cited above, banks will spend less money acquiring new cardholders and the growth of card network payment volumes will slow. New equipment sales for Agilent and Alcon (a minority of their revenues) could decline, and the sale of their premium-priced consumable products and services (a faster growing and more profitable part of their business mix) will become harder. We are confident, though, that any momentum lost to macroeconomic forces will be manageable and temporary. To expect otherwise is to bet against their entrenched positions in industries and economies that benefit from long-term structural growth. Since 2007, (i.e. including the impacts of the Global Financial Crisis and the pandemic) Visa’s revenues are up eight-fold (+15.1% CAGR[2]). Agilent’s have more than tripled (+8.5% CAGR) and Alcon’s are up over two and a half times (+6.7% CAGR).[3] In each case, these businesses have become more diverse, more embedded with their customers, and therefore more resilient in adversity. The next few (potentially recessionary) years will not determine the long-term value of the Fund’s investments any more than the last few (pandemic-stricken ones) have.

A deeper understanding of value

In our previous Newsletter (see here) we observed that when using free cash flow (FCF) yield, our preferred measure of value, the Fund’s portfolio of companies is valued similarly to the global index. This remains the case today, with both the Fund and the MSCI World Index carrying a ~5% FCF yield (see Appendix). This is, of course, a relative measure of value. FCF yields for all companies, including the Fund’s, can go higher still as stock prices fall. Since we last wrote on the subject in early September yields have indeed risen.

Any valuation premium the portfolio once commanded on a FCF basis has been eradicated in 2022 amid rising interest rates and dire investor sentiment. We see this as an anomaly because the portfolio’s companies are far more financially productive (generating higher cashflow returns on their capital) and are faster growing than the Index’s average. The Fund’s underlying FCF is also less dependent on financial debt – indeed, several of the portfolio’s companies have net cash. But beyond this there is a deeper reality to the economics of many of the Fund’s businesses that renders this valuation comparison somewhat meaningless. For many of the Fund’s companies the incremental returns from their growth are obscured. They are, in fact, much higher than the reported financial statements might suggest. In some cases, they are extremely high. This is true for the Fund’s payments companies (Visa and Mastercard, as well as Amex, Fiserv and PayPal), its consumer internet franchises (Alphabet, Booking Holdings, Meta Platforms), those involved in providing credit data and analysis (Experian, Moody’s, and S&P Global), and business software providers (Adobe, Intuit and Microsoft). Together these companies account for ~60% of the Fund’s assets. The additional costs incurred for the sale of completing the next digital payment, serving the next digital ad, or delivering extra data services and software are very modest. They require little or no costs of production, sales and marketing expense or working capital. In the near term, this financial model is highly advantageous in managing through an inflationary environment like the one we are currently experiencing. In the longer term, high incremental profitability gives these special companies enormous flexibility to manage their costs.

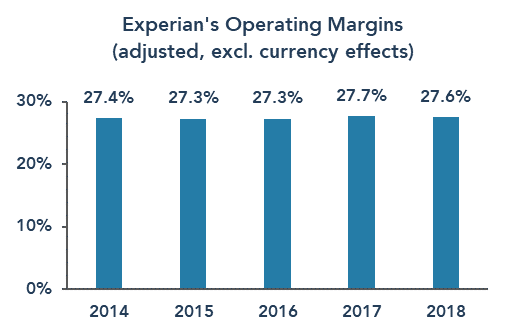

This point was brought home to us several years ago by Experian, a company owned at Troy since 2006. At the start of 2015, current CFO Lloyd Pitchford committed the company to holding group operating margins approximately flat for three years as Experian reinvested into a variety of initiatives to accelerate the group’s growth. Three years later, Lloyd grinned when we discussed this commitment with him at a meeting held in Troy’s offices. Margins were stabilised with remarkable precision.

Source: Experian, 17 May 2018.

This episode tells us something profound about Experian and businesses like it. Their profit margins are not only well above the average, they are also largely within their control. If margins are a choice, it therefore follows that profits and FCF in any given year are at management’s discretion. This is very different from more average companies, beholden to external forces, where costs and margins are a much tighter balancing act. All else equal, if our companies were run in a similar way to the average business, their FCF yields would be considerably higher and the value discrepancy we observe today would be all the more apparent.

Big tech’s luxury to invest (and cut costs)

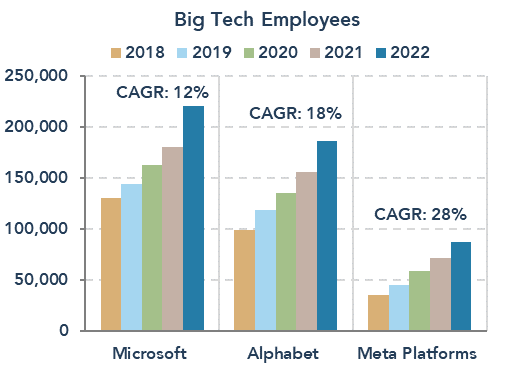

That the Fund’s businesses are far from ordinary has become a point of controversy in recent months. The Fund’s big tech companies (Alphabet, Meta and Microsoft) have each invested at a rapid pace in the last few years to capture growth partly unleashed by the effects of the pandemic. As revenue growth slows for a host of reasons, squeezing margins as employee headcount and expenses continue to rise, investors’ time horizons have naturally shortened to focus on the potential for recessionary impacts next year. We understand the concern as the numbers involved are simply gigantic. When added together, these companies are comfortably spending hundreds of billions of dollars every year on R&D, capex and venture capital-style investments. Cut these, as many investors now suggest, and they would be instantly more profitable and the value inherent in their shares would be compelling.

Source: Bloomberg, 31 October 2022.

The companies themselves are getting the message. Microsoft has announced layoffs and Alphabet has promised to slow the rate of employee growth. Meta’s share price slumped in October when the company said it would continue to grow its operating expenses in 2023, only to subsequently announce a -13% reduction to its work force, providing some relief for the shares. Could this group go further? Undoubtedly. Should they? Yes – probably, but this is where it gets more debatable. We agree that costs have grown too fast based on investment plans that have not generated the expected revenues. There is an opportunity to go on a stricter diet, realign costs, prioritise investments and come out of this tougher period leaner and faster. Stories of underemployment at these firms have become a running joke on social media. That needs to stop. There are, however, limits to our enthusiasm for cutting costs, and investors should be careful what they wish for. These companies’ great progress over the past decade owes a lot to their willingness to reinvest their tremendous profitability back into newer ventures. It was far-sighted, patient and aggressive reinvestment that led to Microsoft’s Azure, Alphabet’s YouTube and Meta’s Instagram all becoming the global juggernauts that they are today. Their investments today are, for the most part, strategically sound and not reckless vanity projects as some suggest. The quantum of spend can and should be reduced and we like the Fund’s investments in these companies all the better because they have the opportunity to cut fat as we enter more wintery economic conditions. But consistent with our longer-term perspective, we also want them to remain heavily invested for durable growth over the next decade.

Happier new years

We approach the end of 2022 with a sense of relief. It’s been a rough ride and there are many daunting obstacles ahead. We continue to draw confidence from the steady quality of the Fund’s companies. They sell everyday essential products and services from which they generate enormous and dependable cashflows. This positions the Fund well as the global economy faces various pressures. We continue to view the Fund as reasonably valued when compared to the global corporate average, especially since in the majority of cases the earnings power of the portfolio’s companies is even better than it appears on the surface. They have the flexibility to adapt to a harsher operating environment and emerge from it stronger.

Thank you for your continued interest in the Fund. We wish you and your families a happy Christmas and a prosperous New Year.

[1] We highly recommend our multi-asset colleagues’ latest Investment Report instead.

[2] Compound Annual Growth Rate (CAGR)

[3] Interestingly, Visa was demutualised from the banks in 2008, Agilent split off its electronics instrumentation division into a separately-listed entity in 2013 and Alcon was acquired by Novartis in 2011 only to regain its independence in 2019. We believe that these developments have materially improved the management of these companies and enhanced the rate, durability and profitability of their growth. It is evidence for how corporate change and focus can create lasting value. Please note that for comparison purposes, the figures quoted above exclude Agilent’s electronics business and Alcon’s pharmaceuticals sales.

Disclaimer

Please refer to Troy’s Glossary of investment terms here. All information in this document is correct as at 31 October 2022, unless stated otherwise. The document has been provided for information purposes only. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. The document does not have regard to the investment objectives, financial situation or particular needs of any particular person. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The views expressed reflect the views of Troy Asset Management Limited at the date of this document; however, the views are not guarantees, should not be relied upon and may be subject to change without notice. No warranty is given as to the accuracy or completeness of the information included or provided by a third party in this document. Third party data may belong to a third party.

Fund performance data provided is calculated net of fees unless stated otherwise. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities.

The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The distribution of shares of the sub-funds of Trojan Investment Funds (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information documents or, as the case may be, the key information documents for Switzerland, the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

In Singapore, the offer or invitation to subscribe for or purchase Shares is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act. This document may not be provided to any other person in Singapore.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: Hill House, 1 Little New Street, London EC4A 3TR. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. The fund described in this document is neither available nor offered in the USA or to U.S. Persons.

Copyright © Troy Asset Management Ltd 2022