Recent performance

This is our first newsletter of 2024 and it follows the Trojan Income Fund’s fiscal year end on 31st January. The performance of the Fund for the 12 month period to 31st January 2024 can be summarised as:

- A total return of +5.1% compared to the FTSE All-Share index of +1.9%.

- Lower volatility1 of 8.0% compared to the index of 10.8%.

- Dividend growth of +4.4%.

- The Fund outperformed the market in each of the FTSE All-Share’s down months in the period (namely in March, May, August and October in 2023 and most recently January 2024).

In summary, the Fund had a good fiscal year and delivered the type of return profile that our investors look for; market-beating returns with lower-than-average volatility, healthy dividend growth and resilience in more difficult markets. We are working hard to sustain these results.

Consumer staples – emerging opportunities

The re-emergence of the Chinese economy onto the global stage has been one of the dominant themes for markets since I began my investment career in 2007. It is hard to believe that it was as recent as 2006 that China’s nominal GDP overtook the UK’s! Today, China’s economy is well over 5x the size of ours. Many international industries have sought to benefit from China’s growth. Consumer Staples businesses, a category with longstanding presence in your Fund, provide pertinent examples.

A sharp rise in demand for consumer goods is a long-established part of nations’ economic development. According to Unilever, as GDP per capita (PPP) reaches c.$8,000-9,000, a tipping point of accelerated demand is reached and spend on fast moving consumer goods (FMCGs) surges. Rising incomes enable the purchase of white goods such as refrigerators, dishwashers, and washing machines, fuelling demand for more varied foodstuffs as well as dishwashing tablets and washing powders/liquids/capsules. As economic development continues, consumers tend to start on the inexorable journey from ‘value’ to ‘premium’ products. It is therefore no surprise that the global Consumer Staples giants have worked hard to establish a competitive presence in China in the 21st century.

More recently however, a slowdown in economic growth and increased geopolitical risks have started to tilt the narrative on China. And there is an additional challenge looming that is of particular relevance to Consumer Staples – the country’s demography. China’s population has grown by almost 300m people since 1990 to c.1.4bn. This is a huge number, and the middle class continues to grow at pace. However, the overall population is now shrinking and, concerningly, ageing fast. China currently has 20% of the population over the age of 60 and this number is forecast to reach nearly 40% by 2050. Since 2017, China’s birth rate has fallen almost 40%. Whilst a rising wealth effect should persist for some time, it will be hard to overcome these demographic challenges on a long-term view.

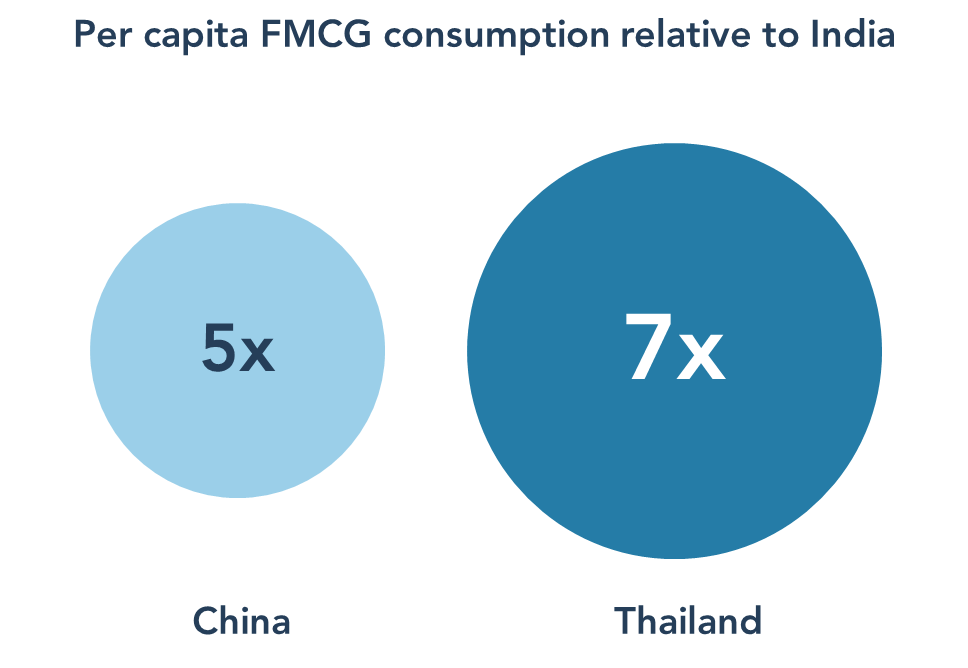

Against this backdrop, a new hope for economic development on a massive scale has emerged – India. Whilst not without political risk itself, India is seemingly more aligned to the West than China. The Indian economy is firing on all cylinders and is expected to become the world’s third largest by 2027 (from fifth place today). GDP per capita (PPP) of $8,400 is already firmly within the band at which consumption patterns tend to upwardly inflect. This growth has been built on a bedrock of investment in public infrastructure and digital services. Crucially, despite having a very similar population size, India has a dramatically different demographic profile to China. More than 50% of India’s population is below the age of 30 and urbanisation is expected to lead to more than 10m people per year moving to cities. Consumption of fast-moving consumer goods in urban areas can be 3x as high as rural populations. Today, India’s consumption is at only 20% of China’s, but a young, urban and increasingly wealthy population is music to the ears of consumer-facing companies.

The large consumer staples companies held in your Fund already have long histories in India and have invested heavily over the past decade. Diageo for instance has accumulated a 55% controlling stake in United Spirits, the country’s largest spirits company. Reckitt has strong presence, particularly through market-leading hygiene brand Dettol. But perhaps the most valuable presence of all is Unilever’s holding in Hindustan Unilever.

A jewel in the crown

Unilever PLC’s 62% holding in India-listed Hindustan Unilever Limited (HUL) is regarded as the crown jewel in the global Unilever portfolio, and for good reason. It is the largest consumer goods company in India and has been growing materially faster than the parent company and at a higher level of profitability.

Like any good FMCG business, HUL’s competitive advantage lies in the strength of its brands and distribution. Having traded in India in some form since 1888, Unilever’s brands have number one positions across 85% of their Indian business, in categories ranging from ice cream to personal care products. Hindustan Unilever also has one of the widest distribution networks of any business in the country. Nine in ten Indian households use HUL brands and the company reaches c.9m out of the country’s c.11m retail outlets. The unique structure of the Indian market creates significant barriers to entry for newer less established brands and makes HUL’s distribution virtually impossible to fully replicate. Whereas modern supermarkets dominate in countries like the UK, 80% of HUL’s revenue is from local ‘mom and pop’ shops (called kirana stores) to which HUL has unmatched access. The company has also invested in a powerful digital offering to service these general trade stores. Today, more than 1.3m of these customers use HUL’s bespoke electronic B2B ordering app.

Source: Google Images

Despite Unilever’s majority ownership, HUL is a quintessentially Indian business with an independent management team, local listing, and brands that are deeply integrated into the local culture. HUL’s operational autonomy allows it to leverage the benefits of the group’s global R&D investment but apply it in a way that delivers success at a local level. This has been one of the reasons why HUL has been able to outperform other international FMCG peers in the region. HUL’s people are an important competitive advantage. The company has been able to attract the best talent in the country for many years and has cultivated a high-performance culture. This has long been recognised at the parent company and is evident through the disproportionate representation of HUL in the parent company’s senior leadership team. It has also been highlighted by Unilever PLC’s new CEO and Chairman in our most recent interactions.

Source: Hindustan Unilever

HUL’s strong brands and distribution, coupled with still immature consumption habits, drive the prospect of fast and long sustaining growth. This growth is becoming all the more valuable to Unilever PLC itself, particularly as its Indian business is more profitable and significantly more highly valued than the rest of the group. Hindustan Unilever has accounted for 25% of Unilever’s total revenue growth since 2010 despite being only 12% of current sales. Assuming HUL continues to grow in line with the 8-10% rate achieved over the past decade, it is quite possible that HUL could represent c.30% of group profits by 2035. The bigger this business gets, the faster Unilever as a group should grow and the more valuable we believe it should be.

We have spent a significant amount of time with Unilever management and have deepened our research over the past year, with a specific focus on HUL. We are also positive about Unilever’s new CEO and CFO. They see significant potential to apply learnings from HUL to other parts of the business – where this degree of cross-pollination has historically been lacking. We are left feeling enthusiastic about the future for the group, and in particular the exciting Indian exposure accessed through Hindustan Unilever and its growing influence on the prospects for the PLC.

1As measured by the standard deviation of monthly returns.

Please refer to Troy’s Glossary of Investment terms here. Fund performance data provided is calculated net of fees with income reinvested unless stated otherwise. All performance and income data is in relation to the stated share class, performance of other share classes may differ. Past performance is not a guide to future performance. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the fund’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. Any reference to benchmarks are for comparative purposes only. Tax legislation and the levels of relief from taxation can change at any time. Any change in the tax status of a Fund or in tax legislation could affect the value of the investments held by the Fund or its ability to provide returns to its investors. The tax treatment of an investment, and any dividends received, will depend on the individual circumstances of the investor and may be subject to change in the future. The yield is not guaranteed and will fluctuate. Any objective will be treated as a target only and should not be considered as an assurance or guarantee of performance of the Fund or any part of it. The fund may use currency forward derivatives for the purpose of efficient portfolio management.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained in the prospectus, the relevant key investor information document and the latest report and accounts. The investment policy and process of the fund(s) may not be suitable for all investors. If you are in any doubt about whether the fund(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party.

The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The sub-funds are registered for distribution to professional investors only in Ireland. The distribution of certain share classes of the sub-funds of Trojan Investment Funds (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain a copy of the prospectus and the key information documents for Switzerland, the memorandum and articles of association, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Reyl & Cie Ltd, Rue du Rhône 4, CH-1204 Geneva, Switzerland, web: www.reyl.com. The Swiss paying agent is: Reyl & Cie Ltd, Rue du Rhône 4, CH-1204 Geneva, Switzerland. Certain sub-funds are registered in Singapore and the offer or invitation to subscribe for or purchase Shares in Singapore is an exempt offer made only: (i) to “institutional investors” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “SFA”); (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

All references to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2024. ‘FTSE ®’ is a trade mark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Limited 2024.