Avoiding banks, sticking with quality

It has been a positive start to the year for markets – almost every major equity index is up year to date. Nevertheless, we are mindful of the consequences of the fastest interest rate hiking cycle in over forty years. The past two months have brought an appropriate reminder, with the abrupt failure of four mid-sized US banks along with Credit Suisse, the latter finalising the demise a 167-year-old mainstay of the Swiss economy. The events had echoes of the global financial crisis and sparked widespread falls in the share prices of banks and other financial companies. We were pleased to see your Fund respond as defensively as we would expect during the sharp market sell-off1 in March, delivering a modestly positive total return2 in falling markets. Investors should expect the lagged impact of higher rates to continue to throw up challenges.

Regular readers will know we like defensive dividend growth from businesses that can sustain high returns on capital throughout the economic cycle. As such, we tend to avoid highly levered3 business models such as those of banks. March’s short episode reminds us of the risk and volatility possible for shareholders when a company’s equity is dwarfed by its liabilities. That is not to say that banks cannot be good investments, but the inherent volatility of profits, dividends and share prices do not easily fit our approach at Troy. Thankfully, we find ample high-quality dividend growth opportunities elsewhere across the UK market.

A good time for income

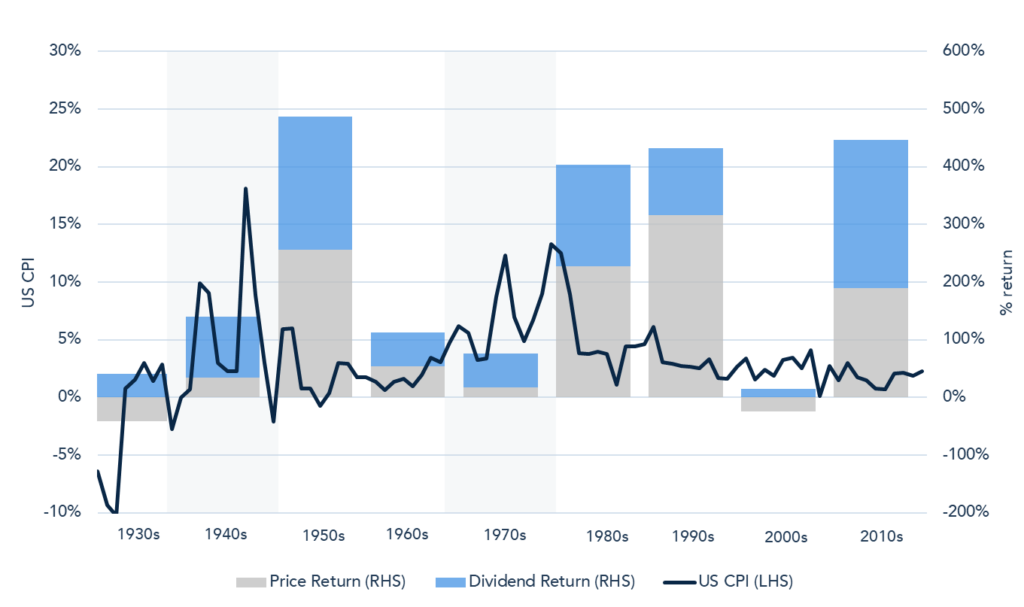

We see great virtue in the reliable dividend compounder for today’s investor. Higher and more volatile inflation and interest rates create a complex investing environment. Dividends provide the certainty of hard cash today, over the promise of share price returns tomorrow – a feature that becomes more valuable in uncertain times. Indeed, in periods of sustained high inflation, history tells us that dividends become a significantly larger proportion of investors’ total returns2 relative to share prices, as Chart 1 highlights through the 1940s and 1970s. (We would also note that dividends become your only source of positive return when share price returns are negative, such as through the 1930s and 2000s). Even more important is dividend income that can continually grow year-on-year – this is a potent weapon against inflation, and the key advantage of equity investing over fixed income/cash. Income from bonds is, by design, fixed, whereas the beauty of dividend income from quality companies is the reliable, steady growth.

Chart 1: Share price and dividend returns from the S&P 500 index by decade, with US CPI overlayed. A larger proportion of total returns came from dividends during the high inflation of the 1940s and 1970s

Source: S&P and Factset, 31 December 2022. Income generated may fall as well as rise and past performance is not a guide to future performance.

It is no mean feat for a company to regularly hand back a portion of their cash profits to shareholders as dividends. The challenge is laid bare when noting that, by our reckoning, only 15 of the 350 largest companies in the UK market4 have managed to grow their dividends every year without interruption for 20+ years (see Table 1). More than half of these names are in our UK Income portfolios, and we are very interested in the others!

Table 1:

| Company |

|---|

| British American Tobacco* |

| Bunzl* |

| Clarkson |

| Cranswick |

| Croda* |

| DCC |

| Diageo* |

| Diploma* |

| Halma |

| National Grid* |

| Primary Health Properties |

| Rotork* |

| Sage* |

| Spectris |

| Spirax-Sarco |

| *Held in the Troy’s UK Income portfolios. |

Robust dividend growth from core holdings

Dividends have also long been viewed as important signals of corporate health and management’s view on a company’s prospects. No signals are full-proof, but we believe dividend actions are insightful, especially for those companies with the credibility of long track records. With that in mind, we are encouraged by the strong recent dividend announcements from your portfolio companies.

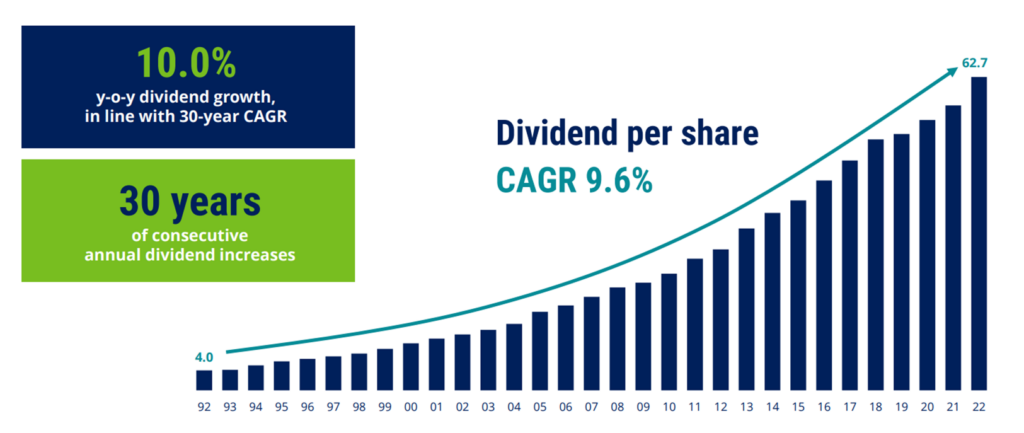

A standout for us was Bunzl (c.3.5% holding), which raised its full-year dividend by +10% on the back of even stronger growth in profits. Bunzl has proven its defensive qualities amidst the current record inflation, continuing a remarkable track record of resilience through many and varied challenging environments. CEO Frank van Zanten took on the top job in 2016, but first joined the company in 1994 when his family-owned business was acquired by the group. Frank has been with the company for almost the entirety of Bunzl’s now 30-year unbroken dividend growth track record (1992-2022, see Chart 2). The company has had extraordinary success in this time, becoming the clear global leader in its distribution niche and building a reputation for reliability and continuous improvement. It stands to reason that Frank has seen what makes a truly successful business, and the first seven years of his tenure suggest he knows how to keep it going. We greatly value these combinations of strong management teams in proven, quality businesses.

Chart 2: Bunzl – Three decades of consecutive dividend growth

Source: Bunzl, 28 February 2023. CAGR is the compound annual growth rate.

A similarly fruitful partnership is found in core portfolio holding RELX (c.7% holding). CEO Erik Engstrom has led the company since 2009, and through steady year-on-year progress has evolved the business into one of UK’s best technology businesses. Despite today’s challenges of inflation, higher costs, and concerns of a recession, RELX reports that their efforts over the past decade are translating into structurally higher growth rates. 10% growth in their latest full-year dividend, on top of buybacks and a healthy outlook are reassuring signals in uncertain times.

There are also some clear positive drivers benefitting some holdings today. The resurgence in global mobility post-pandemic is playing into the hands of IHG (c.2% holding), one of largest branded hotel companies in the world. A further latent boost can be expected from the more recent ‘reopening’ of China where IHG has a large presence. Strong recent results supported 10% growth in its recent dividend.

We must also mention Consumer Staples – a sector that typifies many of the characteristics we value most. We note a ‘return to form’ for Reckitt (c.7% holding), which recently announced +9% growth in its final dividend. This marks a resumption of growth in its distribution, and a signal of confidence after several years of working to reinvigorate the business. Consumer Staples have faced a punishing environment in the past two years, with spiralling raw material costs impacting margins and necessitating hefty price increases for end consumers. Pleasingly, the impact on demand has been limited and there are signs we are through the worst. In its latest results, Procter & Gamble (c.2.5% holding) points to an improving outlook for volumes and underlying improvements in margins after months of navigating high inflation. We have often extolled the virtues of consumer brands and the pricing power they hold, and we have been very reassured by the capabilities demonstrated by the portfolio’s global consumer staples through this time.

A marathon not a sprint

Not all companies are reporting high-single-digit or double-digit growth in dividends, but across the Fund almost every announcement so far this year has brought growth. We are very happy with even modest growth when it stems from repeatable, reliable business. In aggregate, we look to deliver at least mid-single digit growth in the Fund’s dividend year-in, year-out from a collection of resilient, high-quality companies. There is great value in steady progress, and steady income. We agree wholeheartedly with the recent writings of Simon Wolfson, CEO of Next plc for 22 years and regular source of invaluable insight on successful business:

“It is all too easy for companies to lose sight of the fact that assets that deliver modest growth and healthy cash flow are very valuable assets. Too many ‘mature’ companies have been sacrificed at the altar of ‘growth’: it is a well-trodden path that has littered corporate history with the carcasses of ruined companies – from GEC/Marconi to Northern Rock. Growth can always be bought, and ambitious sales targets achieved, through taking on higher and higher risks for lower and lower returns.

We are very clear: if we cannot find good quality investments, then there is no shame (and much wisdom) in handing surplus cash back to our shareholders.”

We think this is highly sensible advice for today’s investment climate and we remain wholly focused on seeking out the reliable dividend compounders of tomorrow. There are exciting valuations on offer for such companies in the UK market and we look forward to sharing further insights in future newsletters.

1A sell-off occurs when a large volume of securities are sold in a short period of time, causing the price of a security to fall in rapid succession.

2Return on an investment including capital appreciation and dividend or interest.

3A company which has a large amount of debt relative to its equity.

4Excluding investment trusts

Please refer to Troy’s Glossary of Investment terms here. Performance data is net of fees with income reinvested unless stated otherwise. All performance and income data is in relation to the stated share class, performance of other share classes may vary. Past performance is not a guide to future performance. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the Fund’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. Tax legislation and the levels of relief from taxation can change at any time. The yield is not guaranteed and will fluctuate. There is no guarantee that the objective of the investments will be met. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. For further information on Troy’s use of benchmarks, you should consult the Fund prospectus. Investments denominated in currencies other than the base currency of the Fund may be affected by movements in currency exchange rates.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. The investment policy and process may not be suitable for all investors.

Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Ratings from independent rating agencies should not be taken as a recommendation.

The Fund is registered for distribution to the public in the UK but not in any other jurisdiction. The sub-funds are registered for distribution to professional investors only in Ireland. The distribution of shares of sub-funds of Trojan Investment Fund (“Shares”) in Switzerland is made exclusively to, and directed at, qualified investors (“Qualified Investors”), as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended, and its implementing ordinance. Qualified Investors can obtain the prospectus, the key investor information document(s) (edition for Switzerland), the instrument of incorporation, the latest annual and semi-annual report, and further information free of charge from the representative in Switzerland: Carnegie Fund Services S.A., 11, rue du Général-Dufour, CH-1204 Geneva, Switzerland, web: www.carnegie-fund-services.ch. The Swiss paying agent is: Banque Cantonale de Genève, 17, quai de l’Ile, CH-1204 Geneva, Switzerland.

The offer or invitation to subscribe for or purchase shares in Singapore is an exempt offer made only: (i) to “institutional investors” (as defined in the Securities and Futures Act, pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore, as amended or modified (the “SFA”); (ii) to “relevant persons” (as defined in Section 305(5) of the SFA) pursuant to Section 305(1) of the SFA, and where applicable, the conditions specified in Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018; (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the SFA; or (iv) pursuant to, and in accordance with the conditions of, any other applicable exemption provisions of the SFA.

All reference to FTSE indices or data used in this presentation is © FTSE International Limited (“FTSE”) 2023. ‘FTSE ®’ is a trademark of the London Stock Exchange Group companies and is used by FTSE under licence.

Issued by Troy Asset Management Limited (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP . Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training.

© Troy Asset Management Limited 2023